Hello friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I am now approaching my 3rd anniversary of my "Buy and Hold" model on Covestor which had its inception on April 15, 2009. Similarly I am approaching my 9th anniversary of my first entry on this blog on May 12, 2003. I would like to thank all of my readers and everyone at Covestor and Seeking Alpha who have supported me and encouraged my blogging.

This past month I picked up shares of W.W. Grainger (GWW) for my Covestor Buy and Hold Model on March 12, 2012, at a cost of $212.98/share. GWW closed at $214.81 on March 30, 2012, down $(2.74) or (1.26)% on the day, slighly ahead of my own purchase price. Let's take a closer look at the business, the fundamentals of performance, some of the valuation figures and finally the technicals of the price chart.

This past month I picked up shares of W.W. Grainger (GWW) for my Covestor Buy and Hold Model on March 12, 2012, at a cost of $212.98/share. GWW closed at $214.81 on March 30, 2012, down $(2.74) or (1.26)% on the day, slighly ahead of my own purchase price. Let's take a closer look at the business, the fundamentals of performance, some of the valuation figures and finally the technicals of the price chart.

According to the Yahoo "Profile" on W.W. Grainger (GWW), the company

"... provides material handling equipment, safety and

security supplies, lighting and electrical products, power and hand tools, pumps and plumbing supplies, cleaning and maintenance supplies, forestry and agriculture equipment, building and home inspection supplies, vehicle and fleet components, fasteners, instruments, welding and shop equipment, and various other items for facilities maintenance market; and services comprising inventory management and energy efficiency solutions. Its customers include small and medium-sized businesses to large corporations, government entities, and other institutions."

How is the business doing? On March 12, 2012, GWW reported strong February, 2012 sales, with an 18% increase aided by an additional selling day (21), higher prices, and higher volumes.

Examining their latest quarterly report, Grainger (GWW) reported 4th quarter results on January 25, 2012. Revenue came in at $2.08 billion, ahead of the $2.07 billion analysts were expecting according to FactSet Research, and earnings came in at $148.5 million or $2.04/share, or an adjusted $2.13/share ahead of last year's $132.2 million or $1.83/share while also exceeding expectations of $2.11/share. The company maintained guidance of $9.90 to $10.6/share for the 2012 fiscal year.

Longer-term, Grainger, according to the Morningstar.com 'Financials' has increased its revenue from $6.4 billion in 2007 to $8.07 billion in the trailing twelve months (TTM). During the same period earnings have increased from $4.94/share in 2007 to $9.07/share in the TTM. Outstanding shares have decreased from 85 million in 2007 to 71 million shares outstanding in the TTM as the company bought back shares steadily during this period.

As of December, 2011, GWW had $2.7 billion in total current assets $.87 billion in total current liabilities for a healthy current ratio of 3.1. Free cash flow has grown from $271 million in 2007 to $549 million in 2011.

In terms of valuation, using the Yahoo 'Key Statistics' on W.W. Grainger (GWW), we can see that this is a large cap stock with a market capitalization of $15.06 Billion. The trailing P/E is a bit rich at 23.68 but with continued growth, the forward P/E is estimated (fye Dec 31, 2013) at 17.84 with a PEG Ratio (5 yr expected) working out more reasonable at 1.55.

The company has 70.1 million shares outstanding with 60.32 million that float. As of 3/15/12, there were 1.49 million shares out short ahead of my own arbitrary '3 day rule' at 5.60 days or short interest. The company pays a dividend estimated going forward at $2.64 yielding 1.20%. The company has a payout ratio of 28% and last had a stock split in 1988 when it split its shares 2:1.

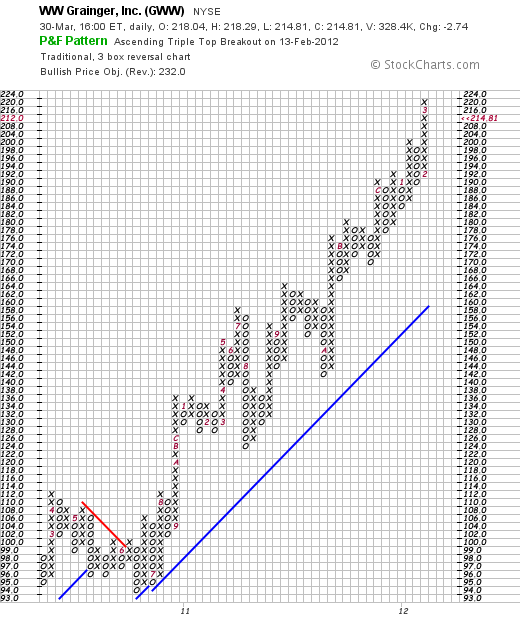

There is little to explain about the technicals on GWW. Looking at the 'point & figure' chart on Grainger from StockCharts.com, we can see a chart of impressive strength. After a small correction in April, 2010, from $112/share to a level of $94/share in June, 2010, the stock has soared steadily to its current level of $214.81. If anything, the chart suggests the stock may well be a bit ahead of itself and ripe for a retesting of support levels at the $170 level.

Recently, the IBD reported how W.W. Grainger (GWW) and Fastenal (FAST) as well as Home Depot and Tractor Supply (TSCO) could well benefit from an economic rebound as they are all involved in the 'nuts and bolts' of business growth.

While the economic recovery in America is far from certain, there are signs that America is turning around from recession at least into slow growth. With things picking up, I would have to second the idea that Grainger (GWW) might be a good place to put one's investment dollars. That certainly was what I did in my own portfolio.

Grainger has a broad range of products serving multiple industries, reported strong February sales figures, came in with a very healthy quarterly report that exceeded expectations and has a track record of growth going back several years at least. They have a solid balance sheet and are generating increasing free cash flow while reducing their outstanding shares. These factors generally bode well for shareholders.

Valuation-wise, the company is priced a bit rich with a P/E north of 23, but if growth continues as expected (or perhaps exceeding expectations), this will work out to a PEG just over 1.5 for a relatively reasonable valuation. The company has a lot of shares out short possibly setting itself up for a squeeze if they continue to do well.

Technically, the shares have been extremely strong without even a suggestion of weakness for the past 2+ years. That enough should make you a little cautious. But I would rather invest in stocks showing persistence of price momentum than the alternative.

Thanks again for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them right here.

Yours in investing,

Bob

Updated: Sunday, 1 April 2012 10:47 PM CDT