Stock Picks Bob's Advice

Tuesday, 13 April 2010

Schlumerger LTD (SLB) and Sysco (SYY) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Sysco (SYY) is currently one of my holdings in my Trading Account. My 125 shares were acquired 7/27/09 with an effective cost basis of $23.25/share. As I have discussed elsewhere I manage all of my holdings by minimizing losses by selling stocks quickly and completely if they decline and lock-in stocks that appreciate in price by selling them slowly and partially at targeted appreciation levels determined by my purchase price. As is my strategy, I sell 1/7th of my holding as each appreciation price is reached.

Sysco (SYY) is currently one of my holdings in my Trading Account. My 125 shares were acquired 7/27/09 with an effective cost basis of $23.25/share. As I have discussed elsewhere I manage all of my holdings by minimizing losses by selling stocks quickly and completely if they decline and lock-in stocks that appreciate in price by selling them slowly and partially at targeted appreciation levels determined by my purchase price. As is my strategy, I sell 1/7th of my holding as each appreciation price is reached.

Sysco (SYY) hit my first appreciation level which is a 30% gain from the purchase price today and I sold 18 shares of my 125 shares (I now have 107 shares of SYY remaining in my account) at a price of $30.30. This represented a gain of $7.05 or 30.3% since purchase.

It is also my strategy to allocate my portfolio into equities or cash based upon the activity of my underlying holdings. In this case, owning far less than my maximum of 20 positions (only 8 currently) a partial sale on a stock appreciating (what I refer to as "good news") generates a signal to add a new holding. On the other hand should I sell a stock on a decline, I refer to this as a sale on 'good news' and instead of adding a new holding, I leave the proceeds in cash. Thus, assuming that my stocks generally reflect the overall tone of the market, I am literally forced to respond to market moves by either adding to stocks or moving into cash.

With the sale of shares of Sysco (SYY) on good news, I utilized this "good news" buy signal to make a purchase of shares of Schlumberger (SLB). I purchased 42 shares of Schlumberger (SLB) at

With the sale of shares of Sysco (SYY) on good news, I utilized this "good news" buy signal to make a purchase of shares of Schlumberger (SLB). I purchased 42 shares of Schlumberger (SLB) at $42.00$65.48/share for a cost of $2,756.85. It is my intention to continue to add new positions on 'good news' creating a new holding slightly bigger than the average size of my other positions.

The economy appears to be slowly recovering from the deep recession of 2008. Even though unemployment remains unacceptably high at 9.7%, last month 162,000 jobs were created, the best job creation performance since the recession began. The recession kept oil prices low, making oil service companies like Schlumberger (SLB) unattractive to investors. However, oil prices have once again moved sharply higher as the recovery has developed. Graphically, we can see the sharp rebound in oil prices in this chart from MoneyWeek:

As this article points out, as expected, as oil prices have rebounded so has the resurgence in oil exploriation as oil rigs recently hit a 14-month high.

Given all of this, I chose to buy shares of Schlumberger (SLB) a company which according to the Yahoo Profile,

"...supply technology, integrated project management, and information solutions to the oil and gas industry worldwide. The company operates in two segments, Oilfield Services and WesternGeco. The Oilfield Services segment provides a range of exploration and production services required during the life of an oil and gas reservoir."

and

"The WesternGeco segment provides reservoir imaging, monitoring, and development services, as well as operates data processing centers, and multiclient seismic library. Its services range from 3D and time-lapse (4D) seismic surveys to multi-component surveys for delineating prospects and reservoir management. The company has a joint venture agreement with National Oilwell Varco, Incorporated to provide high speed drill string telemetry systems."

Schlumberger (SLB) will be announcing the latest quarter's results in just a few days on April 23, 2010.

On January 22, 2010, Schlumberger (SLB) announced 4th quarter 2009 results. Revenue came in at $5.74 billion, down from the $6.87 billion in revenue the prior year. Income from continuing operations decreased 34% to $.67/share vs. the $1.03/share the prior year. Sequentially both results improved but year-over-year results showed the effects of the slowdown in the oil exploration business in the midst of the recession.

This stock does not really fit into my usual strategy of buying the consistent growing company independent of cyclical economic events. However, as this economy rebounds it seems wise to participate in those sectors that are emerging from downturns---oil service appears to fit the bill.

In fact, Schlumberger has used the economic recession as an opportunity to expand its business through acquisition. Most recently it announced an acquision of IGEOSS, a "France-based provider of 'geomechanical solutions', acquired Nexus Geosciences, another seismic software and services company, and Geoservices for $1.07 billion from Astorg Partners, another French firm. Schlumberger, meanwhile, is still working on its acquisiton of Smith International, another oil service company which faces ongoing Justice Department review.

In terms of longer-term financial results, reviewing the Morningstar.com "5-Yr Restated" financials on SLB, we can see that revenue which grew rapidly from $14.3 billion in 2005, peaked at $27.2 billion in 2008, then dipped to $22.7 billion in 2009. Earnings grew rapidly from $1.82/share in 2005 to $4.45/share in 2008 only to also dip to $2.59/share in 2009. Dividends are paid regularly and grew from $.42/share in 2005 to $.84/share in 2008 where it was kept in 2009. Outstanding shares, which increased from 1.23 billion in 2005 to 1.24 billion in 2006, have been decreased with share buy-backs to 1.239 billion in 2007, 1.22 billion in 2008 and 1.21 billion in 2009.

Free cash flow has remained positive with $3.07 billion reported in 2007 and $2.92 billion in 2009. Morningstar shows that the balance sheet is solid with $243 billion in cash and $13.4 billion in other current assets. This is almost a 2:1 current ratio, and in fact current assets are nearly enough to cover both the $7.2 billion in current liabilities and the $7.1 billion in long-term liabilities combined.

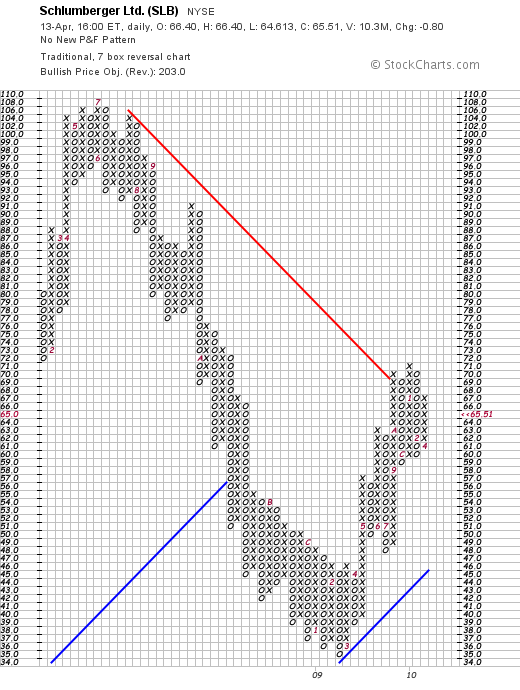

Reviewing the 'point & figure' chart on Schlumberger (SLB) from StockCharts.com, we can see that this stock peaked at approximately $108/share in July, 2008, before sharply selling off and hitting a recent low of $35/share in February, 2009. The stock has rebounded along with the rebound in oil prices, recently broke through resistance at its current level of $65.51. The stock clearly has reversed its downward slide and imho appears poised for further appreciation on the upside.

In terms of valuation, reviewing the "Key Statistics" on Schlumberger (SLB) from Yahoo, we can see that this is a large cap stock with a market capitalization of $78.39 billion. The trailing p/e is a moderate 25.31, but the forward p/e (fye 31-Dec-11) is estimated at 17.06. With the reasonably rapid growth in earnings, the p/e is more or less reasonable as measured by the PEG ratio at 1.56.

Yahoo reports 1.2 billion shares outstanding with 1.19 billion of them that float. As of 3/15/10 there were 44.28 million shares out short, but since the daily volume is a substantial 12.6 million shares (over the past 3 months), the short interest ratio works out to a moderate 2.6, under my own 3 day rule for significance.

The company, as noted above, does pay a dividend with a forward annual dividend rate of $.84/share yielding 1.3%. Schlumberger last split its stock April, 10, 2006, with a 2:1 stock split.

To summarize, my idiosyncratic trading system dictated that I add a new position to my trading account due to the "good news" generated by the partial sale of my holding of Sysco (SYY). Lacking any holding that reflected the new-found strength in the oil market along with the renewed economic recover, I chose a very large player in the oil service industry, Schlumberger (SLB) which appeared to be a relatively good value with good potential going forward.

Thank you for visiting my blog! If you have any comments or questions, please feel free to leave them right here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 10:02 PM CDT

|

Post Comment |

Permalink

Updated: Saturday, 17 April 2010 10:09 PM CDT

Sunday, 11 April 2010

Kohl's (KSS) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I always enjoy writing about a Wisconsin firm that has become a big success in the national market. The first time I wrote up Kohl's (KSS) on this blog was back on August 12, 2006, when the stock was trading at $60.76. Kohl's stock has just now approached that level after the 2008 bear market that savaged so many stocks especially retail stocks that declined sharply in price when the consumer stopped buying.

I always enjoy writing about a Wisconsin firm that has become a big success in the national market. The first time I wrote up Kohl's (KSS) on this blog was back on August 12, 2006, when the stock was trading at $60.76. Kohl's stock has just now approached that level after the 2008 bear market that savaged so many stocks especially retail stocks that declined sharply in price when the consumer stopped buying.

Kohl's (KSS) closed at $56.84 on April 9, 2010, up $.21 or .37% on the day. I believe this stock belongs in my blog and may eventually find a place in my portfolio. I currently do not own any shares.

Kohl's Department Stores has a fascinating history that in some fashion parallels the story of Walmart. In 1962, the same year that Sam Walton was opening up his first discount store in Rogers, Arkansas, 563 miles North-East of that location Max Kohl was opening up his first deparment store, Kohl's Department Store in Brookfield, Wisconsin.

Kohl's Department Stores has a fascinating history that in some fashion parallels the story of Walmart. In 1962, the same year that Sam Walton was opening up his first discount store in Rogers, Arkansas, 563 miles North-East of that location Max Kohl was opening up his first deparment store, Kohl's Department Store in Brookfield, Wisconsin.

Kohl's Department stores has grown significantly since that first store. On March 3, 2010, Kohl's (KSS) announced plans to open nine stores in five states and 'plans to open a total of approximately 30 new stores in 2010.' As of the end of last month, Kohl's (KSS) had a total of 1,067 stores in 49 states. In comparison, Walmart has had an even more meteoric rise with currently more than 8,416 retail outlets 'operating under 53 different banners in 15 countries.'

The other interesting fact about Kohl's (KSS) is the fact that Wisconsin's senior U.S. Senator is Herb Kohl, son of Max Kohl. Herb and his brother inherited Kohl's Department Stores. He later became President of Kohl's and was involved in its sale to BATUS Inc. in 1972. In 1985 Kohl purchased the Milwaukee Bucks and was first elected to the United States Senate in 1988.

The other interesting fact about Kohl's (KSS) is the fact that Wisconsin's senior U.S. Senator is Herb Kohl, son of Max Kohl. Herb and his brother inherited Kohl's Department Stores. He later became President of Kohl's and was involved in its sale to BATUS Inc. in 1972. In 1985 Kohl purchased the Milwaukee Bucks and was first elected to the United States Senate in 1988.

In 1986 BATUS sold Kohl's Department Stores to a 'management-led group of investors.' At that time Kohl's had only 40 stores with sales of $300 million. In 1992, Kohl's (KSS) had their IPO with 11.1 million shares issued and Kohl's Department Store became a publicly traded corporation.

But more than an interesting story of a company that started off as a grocery store opened by a Polish immigrant, is the fact that Kohl's (KSS) remains a compelling investment today.

Kohl's (KSS) is participating in the powerful rebound in retail sales that we are currently experiencing as this nation recovers from recession. Most recently, on April 8, 2010, Kohl's reported that their March same-store sales increased 22.5%, beating expectations of a 12.4% same-store increase according to analysts polled by Thomson Reuters. In addition, the company in the same announcement raised guidance for the first quarter to $.55 to $.57/share up from previous estimate of $.48 to $.52/share in the quarter. This increased guidance exceeded estimates of $.54/share in the quarter that analysts are currently expecting.

Examining the latest quarterly result, the fourth quarter was reported on February 26, 2010. For the quarter ended January 30, 2010, earnings increased 28% to $431 million or $1.40/share from $336 milllion or $1.10/share the prior year. This beat expectations of $1.37/share according to analysts polled by Thomson Reuters. The company was quite cautious in that announcement and guided $.48 to $.52/share for the quarter under analysts expectations of $.54/share.

It is clear that with the increased sales activity at Kohl's stores the past two months, management has moved from a relatively gloomy outlook in February to a more positive outlook this month as noted from its recent raising of guidance on the back of strong same-store sales growth.

Longer-term, reviewing the Morningstar.com "5-Yr Restated" financials, we can see that revenue has grown steadily, except for a pause between 2008 to 2009, from $13.4 billion in 2006 to $17.2 billion in 2010. During this period earnings grew from $2.43/share in 2006 to $3.39/share in 2008 before dipping to $2.89/share in 2009 and then increasing to $3.23/share in 2010 fiscal year. No dividends are paid. Outstanding shares have decreased from 346 million in 2006 to 306 million in 2010.

Free cash flow which was a negative $(307) million in 2008, turned positive at $684 million in 2009 and grew to $1.5 billion positive in 2010.

Looking at the latest balance sheet, as reported by Morningstar.com, Kohl's (KSS) has $2.3 billion in cash, $3.2 billion in other current assets for a total of $5.4 billion in current assets when compared with the $2.4 billion in current liabilities has a healthy current ratio of 2.25. In fact, Kohl's could pay off ALL of its debt both current at $2.4 billion AND the $2.9 billion in long-term debt combined with its total of $5.4 billion in current assets!

In terms of valuation, Yahoo "Key Statistics" reports that Kohl's (KSS) has a market capitalization of $17.45 billion. The trailing p/e is a moderate 17.55 but the forward p/e (fye 30-Jan-2012) is more reasonable at 13.47, and looking forward, the PEG ratio at 1.18 suggests reasonable valuation as well. There are 306.97 million shares outstanding with 272.87 million that float. As of 3/15/10 there were 7.56 million shares out short representing 2.1 days of trading well below my own arbitrary 3 day rule for short interest significance. No dividends are paid and the last stock split was a 2:1 split back on April 25, 2000.

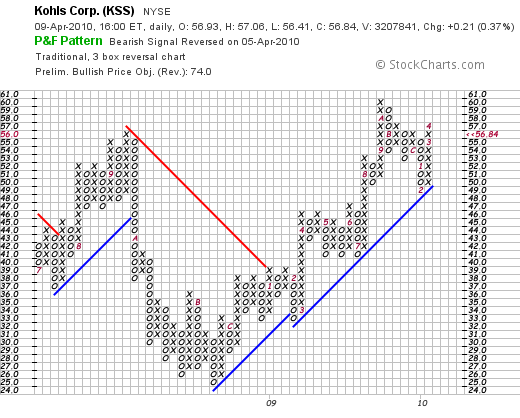

Reviewing the 'point & figure' chart on Kohl's (KSS) from StockCharts.com, we can see that the stock, which peaked at $57 in September, 2008, dipped as low as $25 in August, 2008. Since then the stock has been climbing steadily, hit $60 in October, 2009, dipped to $45 in February, 2010, only to climb once again above support lines to its current level just above $56/share.

To summarize, Kohl's is a uniquely American success story (as well as a Wisconsin success story) of a Polish immigrant starting with a single grocery store in the Milwaukee area, starting a department store in 1962 the same year Sam Walton was opening his own retail store, and growing it to a level where it was acquired, sold back to management, and then taken public where it grew to become a major retail player in the market today. Interestingly, the American success story also includes a currently sitting United States Senator, Herb Kohl, son of the founder of Kohl's and former president of the Department Store chain. Only in America!

Kohl's is experiencing a strong resurgence in sales as it successfully sells the 'middle level' of merchandise between a Macy's and a Target, offering value to a more cost-conscious consumer looking for both quality and value. They reported terrific same-store sales numbers last month which exceeded expectations, and raised guidance on the upcoming quarter. The last quarter exceeded expectations but was accompanied by a more reserved guidance from management. Things appear to be changing quickly for the better for this company.

I do not own any shares, but it is the kind of stock I like, may own in the future, and I believe represents an early recovery for retail and for the U.S. economy as a whole which appears to be slowly rebounding from its deep recession.

If you have any comments or questions, please feel free to leave them on the blog or you can email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Saturday, 3 April 2010

My Experience on Covestor Investment Management (CVIM)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on this website.

I cannot tell you how many times I have written and re-written that phrase about being an amateur investor here on this blog and elsewhere. I am. I love investing and writing about stocks and how I try to think about selecting stocks, deciding when and which stocks to buy and when and how much to be buying and selling when I do implement a transaction.

It is a blast and I thank you for each and every visit and all of your emails and comments that you have left on the blog both positive and critical of my thoughts and actions. I am certainly not always right.

Back in 2007 I was approached about participating with an innovative organization called Covestor about sharing my actual trading portfolio with them and they would publish and track my results and transactions. Starting on June 12, 2007, almost 3 years ago, I have been tracked and followed by Covestor and you can see my Covestor page here. With this service, my trading portfolio became public, my activity and performance verified--both brilliant and quite less than brilliant trades were shared publicly.

Back in 2007 I was approached about participating with an innovative organization called Covestor about sharing my actual trading portfolio with them and they would publish and track my results and transactions. Starting on June 12, 2007, almost 3 years ago, I have been tracked and followed by Covestor and you can see my Covestor page here. With this service, my trading portfolio became public, my activity and performance verified--both brilliant and quite less than brilliant trades were shared publicly.

I continued to refine my investment strategy aware that I was doing my investing publicly. It was a terrific relationship and continues to be useful for me as I refine my own approach to the tumultuous world of stock market investing.

I am particularly grateful to Perry Blacher, the co-Founder of Covestor and the President of Covestor Investment Management, the asset-management side of Covestor. He, along with Rikki Tahta and Simon Veingard are the people who have been among those responsible for getting Covestor from just an idea into an important player in the new "social investing" websites. Perry and Covestor recruited me to participate and have stayed with me as this blog has grown and my investing and writing experience has evolved.

I am particularly grateful to Perry Blacher, the co-Founder of Covestor and the President of Covestor Investment Management, the asset-management side of Covestor. He, along with Rikki Tahta and Simon Veingard are the people who have been among those responsible for getting Covestor from just an idea into an important player in the new "social investing" websites. Perry and Covestor recruited me to participate and have stayed with me as this blog has grown and my investing and writing experience has evolved.

Covestor's business model has always been to actually manage money. On April 14, 2009, a year ago, I was invited to be one of the first ten model accounts that Covestor uses to create shadow accounts utilizing the trading and asset allocation information to allow them to manage money for actual investors. Since I am an amateur, I do not manage any investments but rather am paid a subscription fee for the data feed. This new expanded Covestor service is called Covestor Investment Management (CVIM) and you can see my CVIM page here.

Participating in CVIM has made what I believe to be a responsible strategy of managing investments that much more serious for me. I like to say that I have started investing more like my father who while no longer alive has always been my largest source of inspiration to being involved in the stock market. I continue to look for stocks with revenue growth, earnings growth, solid balance sheets and reasonable valuation---but now find dividends more attractive than ever!

Participating in CVIM has made what I believe to be a responsible strategy of managing investments that much more serious for me. I like to say that I have started investing more like my father who while no longer alive has always been my largest source of inspiration to being involved in the stock market. I continue to look for stocks with revenue growth, earnings growth, solid balance sheets and reasonable valuation---but now find dividends more attractive than ever!

The last couple years, with my own portfolio declining along with all other investors as the market declined in our current 'bear market', I have been more interested in protecting against losses while still interested in capturing the gains of a climbing equities environment. I have added dividends to my list of attreactive features. Dividend stocks, as long as the dividends are secure, may offer an additional form of protection--in an environment of declining stocks, stocks that do not offer dividend merely offer the promise of greater value in the future. A dividend paying stock effectively becomes more attractive as the stock price declines reflecting the increasing dividend yield which is the result of the simple quotient of the stable dividend divided by the reduced stock price.

Furthermore, I have tried to think about stocks which are recession resistant. To that end, I have included stocks like Sysco (SYY), which while feeling a bit of the pinch of the recession, has managed to crank out continued revenue and earnings without interruption. TJ Maxx (TJX) where recession-pinched shoppers can find bargains in name brand products, McDonald's (TJX) where the price point remains a good value and which remains a place where even cash-strapped families can eat. Abbott (ABT) and Johnson & Johnson (JNJ) are two additional steady earners which pay steady and increasing dividends. Church & Dwight (CHD) has grown its results by selling a diverse set of consumer goods without being hurt too much by the economic downturn, AT&T (T) is the pre-eminent widows and orphans stock which has an interesting tie-in with Apple (AAPL) and pays a generous dividend, and 3M (MMM), the steady blue chip industrial finish out my holdings. I own the above stocks in my trading account.

I mention these stocks because my own participation in Covestor (CVIM) has created an increased sense of fiduciary responsibility for me. My own trading volume has decreased, my choice of investments is more sedate---in a word, I feel like I have finally 'grown up'! Things I suppose could be worse. Like falling from the Neverland world of quick trades for fractions of points into the world of grown ups concerned about dividends, tax consequenses, and recession-resistance of the holding, I believe that my participation with Covestor has been good for me and for the people that read my blog.

I do not in any way manage investments for people. But I am aware that what I write about and what I do invest in may result in others doing the same. I cannot promise that I shall do this without failure. I cannot even know that I shall be profitable. But I am glad of the relationship that has resulted in these changes.

Thank you Perry and all of my great friends over at Covestor!

Yours in investing,

Bob

Wednesday, 31 March 2010

The Hershey Company (HSY)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on this website.

Over the nearly seven years of blogging on this website, I have continued to focus on those stocks that I believed deserved inclusion on this blog and possibly inclusion in my portfolio. Until recently, I could depend on momentum investments, identifying companies that could generate greater and greater earnings on increasing revenue while hitting new highs in the market.

Over the nearly seven years of blogging on this website, I have continued to focus on those stocks that I believed deserved inclusion on this blog and possibly inclusion in my portfolio. Until recently, I could depend on momentum investments, identifying companies that could generate greater and greater earnings on increasing revenue while hitting new highs in the market.

Those kind of stocks are difficult to identify although I continue to look for this same pattern of financial results.

More recently I have shifted my holdings into more of a 'widows and orphans' investing approach, looking for value in investing, looking for stocks with growth potential yet showing reasonable valuation (GARP investing) and searching for stocks that might also pay a dividend. In short, as each year passes, I find that I am investing more and more like my father did, looking at dividends, stable and well-recognized names of stocks and their products and enjoying the relative lack of volatility that these 'quality' companies provided.

It is amazing what a good bear market can do to an investor's perspective!

I believe that The Hershey Company (HSY) fits my requirements and I wanted to share with you some of the things that make me believe it may well be a timely and attractive investment at this particular time. Hershey (HSC) closed today (3/31/10) at $42.81, down $(.24) or (.56)% on the day. I do not own any shares of this company at this time.

While Hershey (HSC) is well-known for its chocolate it has a wider range of products. As the Yahoo "Profile" on Hershey explains, the company

While Hershey (HSC) is well-known for its chocolate it has a wider range of products. As the Yahoo "Profile" on Hershey explains, the company

"...offers chocolate and confectionery products, including high-cacao dark chocolate products, such as chocolate bars, tasting squares, home baking products, and professional chocolate and cocoa items; and natural and organic chocolate products consisting of chocolate bars, drinking chocolate, and baking products. The company provides snack products comprising snack mix, granola bars, and macadamia snack nuts and cookies in various varieties; and a line of refreshment products, such as mints, chewing gum, and bubble gum, as well as pantry items consisting of baking ingredients, toppings, and beverages."

Recently Kraft (KFT) purchased Hershey competitor Cadbury for $19.5 billion, making Kraft the world's largest chocolate producer. While Hershey remains the dominant producer of chocolate in North America, this merger may be challenging as Hershey's continues to seek global sales growth.

On February 2, 2010, The Hershey Company (HSY) reported 4th quarter results. After removing one-time charges, the company reported that earnings for the period ended December 31, 2009, came in at $.63/share. This was ahead of expectations of $.60/share of analysts polled by Thomson Reuters. Sales for the quarter increased 2% to $1.41 billion, slightly under expectations of $1.42 billion in revenue by analysts.

For the full year, profits came in at $436 million or $1.90/share, nicely ahead of the prior year's $311.4 million or $1.36/share. Full-year sales also grew 3% to $5.3 billion from $5.13 billion.

They announced expectations the profit should grow 6 to 8% and that sales were anticipated to increase 3-5%. This worked out to an earnings range of $2.30 to $2.34/share ahead of analysts current expectations of $2.28/share. Revenue guidance was essentially in line with the analysts' expectations.

The company also went ahead and raised its quarterly dividend by 2.25 cents to 32 cents.

Looking at Morningstar.com for the "5-Yr Restated" financials on HSY, we can see that revenue has slowly grown from $4.8 billion in 2005 to $5.3 billionin 2009. Earnings have been erratic during this period, increasing from $1.97/share in 2005 to $.2.34/share in 2006. However, after dipping to $.93/share in 2007, they have steadily increased to $1.36/share in 2008 and $1.90/share in 2009.

Outstanding shares have decreased from 248 million in 2005 to 229 million in 2009 as the company retired shares with buy-backs.

Free cash flow after dipping from $589 million in 2007 to $257 million in 2008 has also rebounded strongly in 2009 to $939 million. The balance sheet appears adequately solid with $254 million in cash and $1,132 million in other current assets. This total of $1,386 million, when compared to the $910.6 million in current liabilities yields a healthy current ratio of 1.52.

Looking at valuation, using the Yahoo "Key Statistics" on HSY, we can see that this is a large cap stock with a market capitalization of $9.76 billion. The trailing p/e is a tad rich at 22.48 with a forward p/e (fye 31-Dec-11) estimated at 17.26. With the previously noted single-digit growth rate in earnings estimated by Hershey management, this results in a PEG ratio of 2.86, a bit rich by my standards as I prefer to invest in companies with PEG's between 1.0 and 1.5.

Yahoo reports that the company has 227.9 million shares outstanding with 227.6 million that float. The company trades an average volume of 1.9 million shares. With 5.93 million shares out short as of 3/15/09, this works out to a short interest ratio of 3.3 a bit higher than my arbitrary '3 day rule' for significance.

The company pays a nice dividend of $1.28 (going forward), with a forward annual dividend yield of 3.0%. The company does pay a good chunk of its earnings on its dividend with a payout ratio of 63%. The last stock split was a 2:1 split in June, 2004.

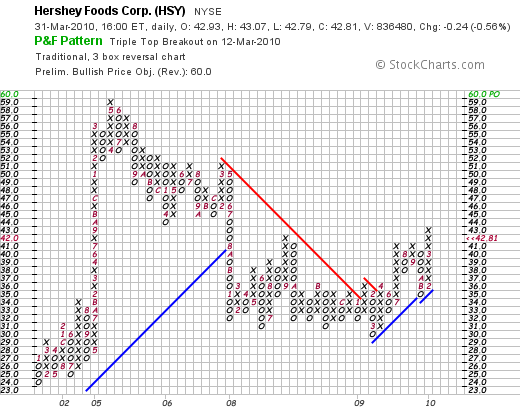

Examining the 'Point & Figure' chart on HSY from StockCharts.com, we can see that the company has really been trading sideways since dipping from $51 to a low of $31 in January, 2008. Recently, the stock appears to be technically breaking through resistance and slogging higher with higher lows and higher highs over the short-term.

In summary, They Hershey Company represents a company with core confectionary brands that are identifiable and well-respected in the United States and in a lesser fashion worldwide. The stock has found support at the $30-$31 level where it has traded for the past two years and only in the past six months has the price started to move higher. While not cheap in terms of absolute p/e or PEG analysis, the company does pay a solid dividend of 3% and has also managed to regularly raise that dividend over the past five years and longer. Recent earnings have been reasonably strong, the company has a growing free cash flow and a solid balance sheet.

This company may just be the sweet investment that I have been looking for! And that doesn't even count the many health benefits of chocolate!

In my own trading account I am still looking for solid companies with well-recognized products or services and appreciate receiving a dividend that has a track record of regularly being raised.

Thanks again for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Thursday, 11 March 2010

Walgreen (WAG) and Abbott Laboratories (ABT) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

As part of this blog, I try to share with you my actual trades in my 'Trading Account' and let you know why I made this trade and what I did with the proceeds. Earlier today I sold my position in Walgreen (WAG) and purchased shares in Abbott Laboratories (ABT) in an approximately equal amount. Specifically, I sold my 66 shares of Walgreen (WAG) at $33.71 and purchased 45 shares of Abbott Laboratories (ABT) at $55.37.Walgreen (WAG) closed at $33.94, down $.33 or (.96)% on the day.

As part of this blog, I try to share with you my actual trades in my 'Trading Account' and let you know why I made this trade and what I did with the proceeds. Earlier today I sold my position in Walgreen (WAG) and purchased shares in Abbott Laboratories (ABT) in an approximately equal amount. Specifically, I sold my 66 shares of Walgreen (WAG) at $33.71 and purchased 45 shares of Abbott Laboratories (ABT) at $55.37.Walgreen (WAG) closed at $33.94, down $.33 or (.96)% on the day.

My shares in Walgreen were purchased almost exactly a year ago on 3/27/09 at a cost basis of $26.73 so I actually had a gain of $6.98 or 26.1% since purchase. I had actually originally purchased 77 shares but had already sold 11 shares 9/23/09 when the stock hit a price of $34.75 and I had a realized gain of $8.02 or 30% since purchase. My sale today was not based on any appreciation or decline to any specified indicated sale level but rather on my own assessment that Walgreen is currently facing some challenges that may for the short-term hold back the performance of this stock while still believing in the long-term potential of Walgreen in general.

Perhaps my first concern with Walgreen's was in December when they reported that November, 2009 sales while up 8.7%, comparable store sales came in at 3.9% under expectations of 6.1%. On January 6th, 2010, WAG reported their retail numbers and again disappointed with same-store sales declining 0.5% missing expectations again. Proving that this wasn't an isolated set of reports, Walgreen on February 3, 2010, reported that January same-store sales dipped 1.1%. Last week on March 3, 2010, Walgreen did report positive same store sales growth but did report a relatively anemic 0.4% increase again under the 0.5% sales increase expected.

With Duane Reade reporting a loss yesterday, and the impending acquisition by WAG anticipated to close in the next few months and the stock acting weak when other shares were moving higher, my patience was tried to its limit, and I pulled the plug on my Walgreen shares looking for another stock to replace it with.

Quite frankly, if we examine the point and figure chart on WAG, the chart doesn't look like it has truly broken down although it is off from its recent high of $41, it is still trading well above support levels down at the $26 level. I chose to sell this stock due to the above-mentioned retail challenges although I am still a big fan of this company and look forward to a possibly repurchase of these shares in the future.

Let's take a closer look at Abbott Laboratories (ABT) and I shall try to explain why I felt more comfortable with this position in my portfolio as opposed to staying with my holding in Walgreen (WAG). ABT closed today (3/11/10) at $55.54, up $.51 or .93% on the day.

According to the Yahoo "Profile" on Abbott, the company

"...engages in the discovery, development, manufacture, and sale of health care products worldwide. It operates in four segments: Pharmaceutical Products, Diagnostic Products, Nutritional Products, and Vascular Products."

If we take a look at their latest quarterly result, Abbott (ABT) reported their fourth-quarter results on January 27, 2010. Their earnings were flat at $1.536 billion or $.98/share compared with $1.536 billion or $.98/share th eprior year. Excluding accounting items, Abbott came in with adjusted earnings of $1.18 vs. $1.06 last year and sales rose 10.6% to $8.79 billion. This was slightly ahead of estimates of $1.17/share on revenue of $8.59 billion.

Reviewing the Morningstar.com "5-Yr Restated" financials on Abbott, we can see that revenue has climbed steadily from $22.3 billion in 2005 to $30.8 billion in 2009. Earnings, after dipping from $2.16/share in 2005 to $1.12/share in 2006, have since climbed steadily to $2.31/share in 2007 and $3.69/share in 2009. Dividends have been increased annually to $1.56/share in 2009 up from $1.09/share in 2005. During this same period, ABT has kept outstanding shares rather stable with 1.56 billion shares in 2005 and 1.55 billion shares in 2009.

Free cash flow has been positive and growing from $3.5 billion in 2007 to $6.2 billion in 2009. The balance sheet also appears solid with $8.8 billion in cash, $14.5 billion in other current assets, and $13.1 billion in current liabilities. This yields a current ratio of 1.79. Abbott does have $16.5 billion in long-term liabilities.

In terms of valuation, looking at Yahoo "Key Statistics" on Abbott, we can see that this is a large cap stock with a market capitalization of $86.23 billion. The trailing p/e is a moderate 15.13 with a forward p/e (fye 31-Dec-11) of 11.64. Thus, the PEG ratio comes in at a very nice 1.12.

Abbott has 1.55 billion shares outstanding with 1.5 billion that float. As of 2/26/10 there were 8.97 million shares out short with a short ratio of only 1.2 (well under my own arbitrary 3 day rule for significance.) Abbott has a forward annual dividend rate of $1.76/share with a forward dividend yield of 3.2%. With a payout ratio of 42%, this dividend appears quite secure. In fact, Abbott is a regular dividend grower and increased its dividend 10% as reported on February 19th.

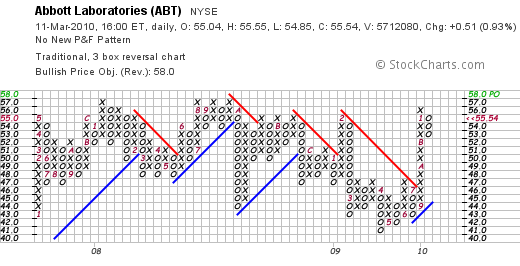

Examining the "point & figure" chart for Abbott on StockCharts.com, we can see that the stock has really been traveling sideways for the past two years between $41 and $57. Hopefully my purchase will not be at the upper range of a continued trading channel and we shall see Abbott move higher breaking through resistance at $57. In any case, the stock is certainly not over-extended. On the other hand, from my amateur perspective, the stock has not 'broken-out' yet to a higher level.

Looking at the Standard & Poor's Stock Report dated 3/10/10 on ABT, (available to me through my Fidelity account), there is a discussion of S&P's estimate of $33 billion of revenue in 2010 vs. $30.8 billion in 2009. The company is in the midst of a purchase of the Solvay Group. The company also just announced a purchase of Facet Biotech with a 67% premium over the market price. This acquisition extends its drug 'pipeline' with treatments for Multiple Sclerosis. This company is making waves on multiple fronts including announcing yesterday approval of the one-pice Tecnis multifocal intraocular lens implant for cataract patients.

In any case, in this market that is subject to the vagaries of an economy that is far from back to normal, I chose to switch from Walgreen to Abbott. With double the yield, a similar p/e, and what appears to be a more stable stock price, I hope that this decision will work out well for me and for my portfolio. Both companies are great growth stock stories and I could not fault anyone for staying tight with Walgreen. For the time being, I chose to make the switch. Wish me well.

If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Saturday, 6 February 2010

ResMed (RMD) "An Update on a Recent Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

In the midst of the recent market correction, there was a stand-out that defied the market decline, and moved strongly higher closing at $54.90, up $3.97 to close at $54.90 on the back of good news. That company was ResMed (RMD) an 'old favorite' that I recently reviewed on September 20, 2009. I do not own any shares of ResMed but it still is the kind of stock that belongs in my portfolio and certainly on this blog.

In the midst of the recent market correction, there was a stand-out that defied the market decline, and moved strongly higher closing at $54.90, up $3.97 to close at $54.90 on the back of good news. That company was ResMed (RMD) an 'old favorite' that I recently reviewed on September 20, 2009. I do not own any shares of ResMed but it still is the kind of stock that belongs in my portfolio and certainly on this blog.

On February 4, 2009, after the close of trading, ResMed (RMD) announced results for the quarter ended December 31, 2009. For the quarter, ResMed came in with revenue of $275.1 million 23% higher than the prior year, exceeding analysts' expectations of $259 million. Earnings came in $46 million or $.60/share in the quarter up from $33.9 million or $.44/share the prior year and again exceeding expectations of $.55/share according to Thomson Reuters I/B/E/S.

Wells Fargo responded by upgrading its own assessment of the stock's prospects to "Market Perform" from "Underperform".

I have briefly discussed sleep apnea in my previous entry, needless to say it is widely diagnosed, associated with the much-discussed obesity epidemic, and can be successfully treated with positive airway pressure. For a more detailed review, you may wish to read this Mayo Clinic review of the subject.

ResMed (RMD) is far from a 'one-quarter-wonder'! If we revisit the Morningstar.com "5-Yr Restated" financials from Morningstar.com, we can see that the company has consistently grown its revenue from $426 million in 2005 to $921 million in 2009 and $1.002 billion in the trailing twelve months (TTM). Earnings have steadily improved (except for a dip between 2006 and 2007, from $.91/share in 2005 to $1.90/share in 2009 and $2.24/share in the TTM. No dividends have been paid. Outstanding shares have been stable at 75 million in 2005 increasing to 79 million in 2008 and then decreasing back to 77 million in the TTM.

Free cash flow has grown from $14 million in 2007 to $129 million in 2009 and slightly less at $114 million in the TTM. The balance sheet presented on Morningstar.com is exceptionally strong with the $451 million in cash reported enough not only to pay off the current liabilities of $240.6 million but also the $123.1 million in long-term liabilities as well! The company has an additional $476 million of other current assets beyond the cash on hand.

According to Yahoo "Key Statistics", RMD has a trailing p/e of 26.34 and has a forward p/e (fye 30-Jun-11) of 20.11. With the rapid growth anticipated the PEG comes in at an acceptable 1.34 level. The market cap is $4.12 billion. There are 74.96 million shares outstanding with 69.69 million that float. As of 1/15/10 there were 5.9 million shares out short representing 12 trading days of volume (the short interest ratio), above my own arbitrary '3 day rule' for short-interest significance and suggesting the possibility of some short-covering in yesterday's sharp price appreciation in the face of good news. The fact of a lot of shares out short is quite bullish in a stock like ResMed that reports results exceeding expectations.

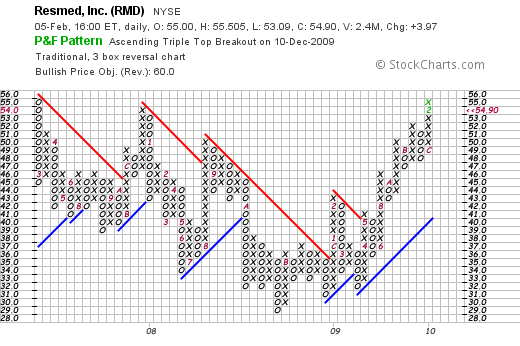

Examining the 'point and figure' chart on ResMed from StockCharts.com, we can see that the stock, which traded as low as $29 in October, 2008, has convincingly broken through resistance and is moving strongly higher at its current level which is higher than the $54-55 level hit in March, 2007, and again in December, 2007, before joining the correction that drove down most stocks in the market.

In summary, I too am kicking myself about why I didn't choose to add this stock to my own trading portfolio. Frankly, I have been quite anxious about the market and have been selecting larger dividend-paying stocks with the hope that I could avoid some of the downward pressures in the market. A stock like ResMed (RMD) demonstrates once again that while dividends are helpful, it is wise to emphasize earnings, revenue growth, and financial stability while understanding the product in a Peter Lynch fashion isn't a bad idea either!

Thanks again for visiting my blog! If you have any comments or questions, please feel free to leave them right here on the website or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Wednesday, 3 February 2010

Walgreen (WAG) "Is the Sky Falling?"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Earlier today I watched in morbid fascination as my shares of Walgreen Co (WAG) plunged from $36.00 at the open to close at $34.62 on the close, down $2.16 or (5.87)% on the day. It was enough to make me feel like traveling down to my local drug store and loading up on a shipment of antacids.

Walgreen (WAG) is one of the eight positions in my Trading Account, having purchased 77 shares on 3/27/09, almost a year ago at a cost basis of $26.73/share. I actually sold 1/7th of my holding, 11 shares, on 9/23/09 after the stock hit approximately $33.75 representing a 30% appreciation on my original shares. Without a disgressionary sale, my own trading system would give me a sale signal should WAG return to my original cost or $26.73 a share, a level considerably lower from its closing price. Today I chose to ride through this sell-off although I certainly came close to pulling the plug on this stock during the day.

Let's take a closer look at what drove the stock price lower. As the market opened Walgreen announced that January sales came in at $5.36 billion, a 2.7% increase over the $5.22 billion for the same month in 2009. However, sales in comparable stores open for the full year, so called "same-store sales", a more reliable retail figure, decreased (1.1)%. The company pointed out that the calendar itself had a negative effect on this figure as this January had one less Thursday and one more Sunday compared to January, 2009.

Overall pharmacy sales increased 1.6% but the same-store pharmacy numbers decreased (1.2)%. Similarly, so-called front-end sales (non-pharmacy), while overall showing an increase of 3.9% showed a decrease of (1.0)% when same-store figures were considered. Other factors attributed to this decline included a large number of generic sales as well as simply less illness in terms of decreased flu cases in 2010 compared to January, 2009.

As is often the case, while the drop in same-store sales wasn't really precipitous and could be explained through different observations, the fact remained that analysts had been expecting instead of a decline of (1.1)%, an increase of 3.2% according to Thomson Reuters. Certainly this 'disappointment' in sales results accounted for the plunge as the street was caught proverbially 'off-guard' and investors dumped shares of Walgreen in a day in which the market itself was performing in an anemic fashion with the Dow dipping 26.30 today to 10,270.55, and S&P dipping 6.04 or (.55)% to 1,097.28.

On January 28, 2009, Rite Aid (RAD), a competitor to WAG reported a decrease in same store sales of (2.1)%. Not only did Rite Aid attribute a drop in sales to increasing generics, unlike WAG, RAD reported a dip of (1.1)% in total prescriptions. Walgreen actually reported an increase of 2.7% in the number of prescriptions filled. CVS, another competitor does not report monthly sales figures.

Probably of equal impact to the January, 2009 sales numbers was the fact that December figure also disappointed when they reported a 0.3% drop in same store sales. Also that month, the 'street' had been expecting a 2.3% increase in sales. Thus even Walgreen (WAG) is subject to the continuing contraction in consumer spending after a United States record decline in 2009 of 6.2% in retail sales according to government records that track back to 1992. If you subscribe to the cockroach theory of financial news, two months does not truly make a trend, but a holder of shares might well be concerned that the next several months will continue to be challenges for Walgreen to get back onto its usual record of steady growth, although I am sure that expectations even now are being reduced by analysts.

And I had hoped that WAG would continue to resist this decline.

Walgreen (WAG) continues to work to restructure its marketing with new inclusions of fresh food, bringing back beer & wine to its stores after deleting this items more than ten years ago, and a generally more conservative expansion plan with few future store openings to save $500 million in 2011 in capital expenditures.

Last month, the company declared that the company should emerge from the downturn in 'an even stronger position'. I shall be patient as my small sale at my 30% appreciation level allows me to tolerate more price volatility within my own investment approach. Hopefully, Gary Kaminsky from "Fast Money" will be on the money and this pullback will be a buying opportunity. As he stated this evening: "I think it's a stock you want to own long term." As an owner of shares, I hope that Gary is right!

As always, if you have any comments or questions, you can reach me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Saturday, 9 January 2010

MedcoHealth Solutions, Inc. (MHS)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I continue to look for and report back to you both on my actual trades in my Trading Account, as well as stocks that I believe are 'suitable' for this blog and for consideration for inclusion in my own stock portfolio. My idea of 'quality' includes companies that show record of consistent revenue and earnings growth, possibly show increasing dividends, stable outstanding shares, positive and growing free cash flow, a reasonable balance sheet, and acceptable valuation. This may be a lot to ask for, but there are many stocks to choose from and neither you nor I can own them all. So why not own some of the best?

MedcoHealth Solutions (MHS) does not fit each and every one of these criteria, but it represents a model of a company that deserves inclusion in this blog as well as consideration for actual ownership because it does meet many of these objectives that I utilize in my own review. I do not currently own any shares nor have any options on this stock. Medco (MHS) closed at $65.05 on January 8, 2010.

MedcoHealth Solutions (MHS) does not fit each and every one of these criteria, but it represents a model of a company that deserves inclusion in this blog as well as consideration for actual ownership because it does meet many of these objectives that I utilize in my own review. I do not currently own any shares nor have any options on this stock. Medco (MHS) closed at $65.05 on January 8, 2010.

According to the Yahoo "Profile" on MHS, the company

"...is a health care company that provides clinically driven pharmacy services for approximately 60 million Americans. The company focuses on various segments of the healthcare industry. It engages in the management and dispensing of prescription medications through its mail-order pharmacies and its network of retail pharmacies."

Examining the latest quarterly report results, on November 3, 2009, Medco reported 3rd quarter results. Revenue for the quarter came in at $14.8 billion, up from $12.6 billion the prior year. Net income increased to $335.6 million or $.69/share up from $296.7 million or $.58/share the prior year. Just as important as the positive results was the fact that the company exceeded earnings expectations of $.71/share according to FactSet compilation of analysts' expectations. The company also exceeded expectations on revenue which had been expected according to Thomson Reuters to come in at $14.68 billion. In addition, the company raised full-year 2009 guidance to range of $2.58 to $2.60 from prior range of $2.54 to $2.59. In addition, the company provided 2010 guidance for earnings of $3.05 to $3.15/share.

For me, this represented an outstanding earnings report in which a company reported strong results which actually exceeded expectations. In addition, they went ahead and raised guidance signalling to analysts that their perspective on future prospects is even better than what is commonly accepted 'on the Street'.

In terms of a longer-term perspective, if we examine the Morningstar.com "5-Yr Expected" financials on Medco, we can see that revenue has been increasing from $35.4 billion in 2004 to $51.3 billion in 2008 and $57.5 billion in the trailing twelve months (TTM). Earnings have also steadily increased from $.88/share in 2004 to $2.13/share in 2008 and $2.45/share in the TTM. The company does not pay a dividend. Outstanding shares which did increase from 549 million in 2004 to 603 million in 2006, have subsequently been decreasing to 519 million in 2008 and 495 million in the TTM.

Free cash flow is positive and growing with $1.09 billion reported in 2006, increasing to $1.35 billion in 2008 and $3.10 billion in the TTM.

In terms of the balance sheet, the company has $2.02 billion in Cash and $5.33 billion in Other Current Assets. This $7.34 billion in Current Assets, when compared to the $5.7 billion yields a satisfactory current ratio of 1.29. The company also has an additional $5.2 billion in Long-Term Liabilities.

In terms of valuation, the company has a market cap of $31.01 billion according to Yahoo "Key Statistics" on MHS. The trailing p/e is a bit rich at 26.53 but with the rapid growth expected (fye 27-Dec-10), the forward p/e is a bit better at 19.42. Looking at the p/e in terms of the growth rate (5 yr expected) yields a reasonable PEG of 1.34. Yahoo reports 476.76 million shares outstanding with 11.57 million shares out short as of December 15, 2009. With an average volume of 2.7 million shares, this works out to a short interest ratio of 5.1 trading days of volume. My own '3 day rule' for short interest, suggests that this might be a significant amount of sales out short which might put upside pressure on this stock if positive results reported in the near future.

No dividends are paid and the last stock split was a 2:1 split on January 25, 2008.

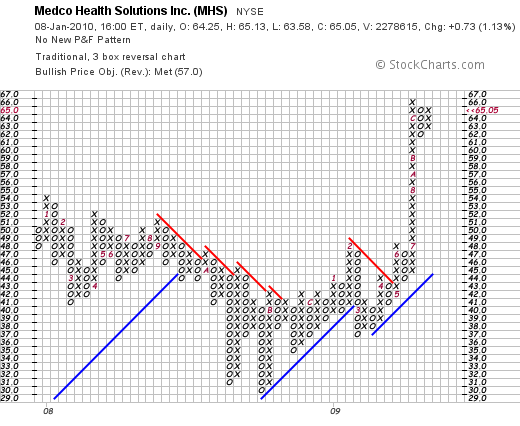

If we review the "point & figure" chart on MHS from StockCharts.com, we can see that the stock, which traded as low as $30 in July, 2008, has subsequently rallied strongly especially since June, 2009 when it climbed from $45 to a high of $66 in December, 2009. The stock has been consolidating between $62 and $66 since that time. If anything, the chart suggests that over the short-term, we may have missed at least one significant leg higher on this price chart and the price might be a bit over-extended technically, at least from this amateur's perspective!

To summarize, MedcoHealth Solutions (MHS) is a stock of a company which recently reported a terrific quarter in the midst of a mediocre economy. They beat expectations and raised guidance in the same announcement. This report was followed by a nice price appreciation of the stock and they should be reporting the next quarter soon.

They are a healthcare company that may well benefit from healthcare reform as additional previously uncovered patients are added to the insurance-covered population in America. They have a record of steadily increasing revenue and earnings over the past five years, have been reducing their outstanding shares the past few years, and are generating free cash flow while maintaining a solid balance sheet. Valuation, while not cheap, still appears reasonable with a PEG under 1.5. In addition, with the recent price appreciation, there are significant numbers of shares out short from speculators who likely bet a stock will decline only because it has risent previously. If the company continues its record of outstanding results, they may well be 'squeezed' adding to the upward momentum.

Thanks again for dropping by and sharing some of your time with me on this website. If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Monday, 28 December 2009

Johnson & Johnson (JNJ) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

This past Thursday (12/24/09) I sold a portion of my 3M (MMM) holding as it had appreciated to a 90% gain from my initial purchase. (I wrote about it here.) Having only 7 positions in my portfolio, well under my maximum of 20 holdings, this partial sale of my 3M holding as it appreciated gave me a 'buy signal' to be adding a new holding to my portfolio and to transfer some of my cash into equity. With that in mind, I chose to purchase 50 shares of Johnson & Johnson (JNJ) today at $64.93/share. The size of the purchase was based on my own calculation of the average size of my holdings in my trading account and what 125% of that size would allow me to purchase.

This past Thursday (12/24/09) I sold a portion of my 3M (MMM) holding as it had appreciated to a 90% gain from my initial purchase. (I wrote about it here.) Having only 7 positions in my portfolio, well under my maximum of 20 holdings, this partial sale of my 3M holding as it appreciated gave me a 'buy signal' to be adding a new holding to my portfolio and to transfer some of my cash into equity. With that in mind, I chose to purchase 50 shares of Johnson & Johnson (JNJ) today at $64.93/share. The size of the purchase was based on my own calculation of the average size of my holdings in my trading account and what 125% of that size would allow me to purchase.

Let's take a closer look at this bluest of blue-chip stocks Johnson & Johnson (JNJ) and why it might represent a good addition to my growing stock portfolio.

First of all Johnson & Johnson does quite a bit more than just make band-aids! As the Yahoo "Profile" on JNJ points out, the company

"...engages in the research and development, manufacture, and sale of various products in the health care field worldwide. Its Consumer segment provides products used in baby care, skin care, oral care, wound care, and women’s health care fields, as well as nutritional and over-the-counter pharmaceutical products...."

Johnson and Johnson is not the picture of uninterrupted growth that I prefer to find in my investments. It is a picture of a large growth stock with quality brands that due to the economic slowdown presents a compelling opportunity for investment from my perspective.

On October 13, 2009, JNJ reported 3rd quarter earnings. Revenue dipped (5.3)% for the quarter to $15.08 billion, down from $15.92 billion the prior year. Earnings however came in stronger at $3.35 billion or $1.20/share, compared to $3.31 billion or $1.17/share the prior year. The company beat expectations of $1.13 on earnings, but missed on revenue expectations which had been estimated to come in at $15.19 billion.

Longer-term, looking at the Morningstar.com "5-Yr Restated" financials on Johnson & Johnson, we can see the relatively steady growth in revenue from $47.3 billion in 2004 to a peak of $63.7 billion in 2008 before dipping to $60.5 billion in the trailing twelve months (TTM).

Earnings have increased in an uninterrupted fashion from $2.74/share in 2004 to $4.58/share in the trailing twelve months. Dividends have been paid and have been increased annually from $1.10/share in 2004 to $1.80/share in 2008 and $1.90/share in the TTM. Outstanding shares increased from 2.99 billion shares in 2004 to 3.00 billion in 2005 before beginning a steady descent as the company bought back shares dippping to 2.84 billion shares in 2008 and 2.79 billion in the TTM.

Earnings have increased in an uninterrupted fashion from $2.74/share in 2004 to $4.58/share in the trailing twelve months. Dividends have been paid and have been increased annually from $1.10/share in 2004 to $1.80/share in 2008 and $1.90/share in the TTM. Outstanding shares increased from 2.99 billion shares in 2004 to 3.00 billion in 2005 before beginning a steady descent as the company bought back shares dippping to 2.84 billion shares in 2008 and 2.79 billion in the TTM.

Free cash flow has grown slowly from an impressive $11.5 billion in 2006 to $12.6 billion in the TTM.

If we look at the balance sheet as presented on Morningstar.com, we can see that JNJ has $11.9 billion in cash, $23.7 billion in other current assets for a total of $35.6 billion in current assets. Compared to the $19.2 billion in current liabilities this yields a current ratio of 1.85. The company has a significant but apparently manageable long-term liabilties of $21.9 billion.

In terms of valuation, according to the Yahoo "Key Statistics" on Johnson & Johnson, the company has a market cap of $179.18 billion. The trailing p/e is a modest 14.18 with a forward p/e (fye 28-Dec-10) estimated at 13.17. The PEG is reported at 1.87 suggesting that the 5 yr expected growth rate is in the single digits.

Yahoo reports that there are 2.76 billion shares outstanding and that 21.33 million of them as of November 30, 2009, are out short. This represents only 1.8 trading days of volume. The company pays a forward dividend of $1.96/share with a yield of 3.00%. The dividend is well-covered by earnings with a payout ratio of only 41%. The company last split its stock in June, 2001.

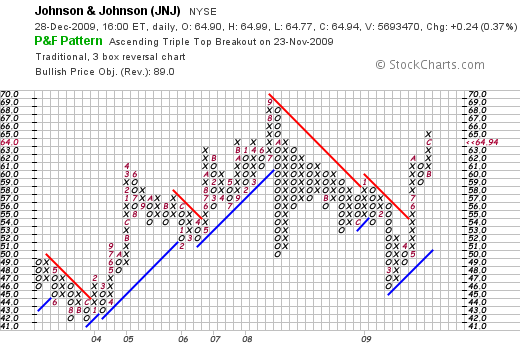

Examining a 'point & figure' chart on Johnson & Johnson (JNJ) from StockCharts.com we can see that the stock has rallied from a low of $42/share in December, 2003, to a peak of $69 in September, 2008, before dipping to a recent low of $46 in March, 2009. Since that time, the stock price has rallied strongly to break through resistance levels to its current level of $64.94/share.

To summarize, my partial sale of shares of my 3M stock entitled me to add a new position. In these uncertain times, Johnson & Johnson offers some comfort in its solid and growing dividend history, low p/e, steady history of revenue growth interrupted only by a recent dip in revenue, and strong free cash flow generation with a solid balance sheet. Johnson & Johnson has a whole flock of brands from Tylenol to Aveeno to Splenda, Sudafed and Motrin. Still having bruises from the market turmoil, it is nice to buy some Band-Aids to cover over some of my superficial financial injuries!

Thanks again for stopping by and visiting! If you have any comments or questions, please feel free to leave your comment here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Thursday, 24 December 2009

3M (MMM) "Trading Transparency" and 'Discussing my Trading Strategy'

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

One of the basic parts of my portfolio management system is to limit losses by selling declining stocks quickly and completely at set loss limits, and to capture the profits of appreciating stocks by selling them slowly and partially at appreciation targets after an initial purchase. On the downside I sell all of my shares if after an initial purchase the stock declines 8%. If I have sold a portion of a stock after an initial purchase after it had reached a single appreciation target (the first appreciation target being at a 30% appreciation level), then I sell all of the remaining shares if the stock should decline to break-even. If I have sold portions more than one time, then I set the tolerance on a price decline to 1/2 of the highest appreciation percentage that the stock was sold. For instance, if I have sold twice at both 30% and 60% appreciation levels, then the remaining shares would be sold if the stock should decline to 1/2 of the 60% appreciation target or at a 30% appreciation point (not 1/2 of the highest price but the 1/2 of the highest appreciation %).

On the upside, my appreciation targets remain at 30, 60, 90, 120, 180, 240, 300, 360, 450% etc. appreciation levels. At each of these levels, should one of my holdings reach it, my approach has been and continues to be to sell a little of that holding--I use 1/7th of the remaining shares (rounded downward).

On the upside, my appreciation targets remain at 30, 60, 90, 120, 180, 240, 300, 360, 450% etc. appreciation levels. At each of these levels, should one of my holdings reach it, my approach has been and continues to be to sell a little of that holding--I use 1/7th of the remaining shares (rounded downward).

Furthermore, these sales are the 'signals' that I utilize to determine my own response to the stock market. That is, sales on the downside, unless I am at my minimum of 5 holdings, do not trigger an additional purchase--instead proceeds are placed into cash. (At the minimum, a sale of one of my remaining 5 holdings does indeed result in another stock being purchased, but this purchase is made at 80% of the average size of the remaining holdings---thus again shifting some of the proceeds into cash but maintaining my 5 position minimum exposure to equities.)

On the upside, sales are also 'triggers' to take action in managing the portfolio. Interpreting an appreciation sale as 'good news' (as opposed to the 'bad news' of the downside sale), I have a signal, which I sometimes refer to as a permission slip, to purchase a new holding. (Once again except if at my maximum of 20 positions, in which case the proceeds are left in cash.)

Currently the top performing position in my portfolio has been my shares of 3M (MMM). I purchased 33 shares on 3/3/09 at a cost basis of $43.64/share. On April 24, 2009, I sold 5 shares (approximately 1/7th) of my holding (in retrospect I really should have sold only 4 shares--as I prefer to round out downward) at a price of $55.21. This represented the first partial sale with a gain of $11.57 or 26.5%.

On July 27, 2009, I sold 4 shares of my remaining 28 shares (1/7th of holding) at a realized price of $67.92. This represented a gain of $24.28 or 55.6% (after costs of transaction included). This was for my 2nd appreciation target of 60% price gain. At each of these sales on gains, I purchased a new holding, utilizing this "good news" trigger as a signal to be expanding my exposure to equities.

Today, with 3M (MMM) trading at $82.87, reaching a price appreciation of $39.23 or 89.9%, I sold 3 shares of my remaining 24 shares (approximately 1/7th of my holding). This sale resulted in a buy signal for me giving me that 'permission slip' to add a new holding. I shall be waiting over the Christmas holiday and considering which new stock I might now wish to be purchasing to add to my portfolio.

Thank you for bearing with me as I went through this rather wordy explanation. Sometimes, with the paucity of trading that I do in my account, it doesn't appear like anything is going on. To the contrary, I am continuously monitoring my stocks and slowly building up a portfolio depending on the actions of my own holding in this rather difficult market.

Thanks again for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Newer | Latest | Older