Stock Picks Bob's Advice

Sunday, 16 November 2008

NEW PODCAST on Haemonetics (HAE) and "Investment Philosophy" and "Position Sizing"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Click HERE for my podcast on "Investment Strategy, and Haemonetics (HAE)".

Thanks for visiting!

If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing!

Bob

Thursday, 13 November 2008

Esco Technologies (ESE) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please rememeber that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Earlier this morning, with the market appearing to move moderately higher (before a dip and then another rally!), I looked to find that 5th position to complete my 5 position minimum in my portfolio. Applying my reduced size strategy, the average size of the other 4 positions was $3000, so looking to invest 1/2 of that amount to complete my five postion minimum, I saw that Esco (ESE), one of my old favorites on the blog was on the list of top % gainers on the NYSE, and I purchased 47 shares at $32.56/share.

Earlier this morning, with the market appearing to move moderately higher (before a dip and then another rally!), I looked to find that 5th position to complete my 5 position minimum in my portfolio. Applying my reduced size strategy, the average size of the other 4 positions was $3000, so looking to invest 1/2 of that amount to complete my five postion minimum, I saw that Esco (ESE), one of my old favorites on the blog was on the list of top % gainers on the NYSE, and I purchased 47 shares at $32.56/share.

As I write, shortly before the close of trading today, Esco (ESE) is continuing to move higher (along with the rest of the market) and is quoted at $34.36, up $3.97 or 13.06% on the day. Relative to my own purchase price, the stock is higher by $1.80 or 5.5% since my acquisition of shares.

Let me try to briefly review some of the things that led me to select Esco today to fill out my minimum portfolio holdings. First of all, after the close of trading yesterday, Esco announced 4th quarter 2008 and full year results. For the quarter ended September 30, 2008, the company reported net sales of $196.0 million, a 40.1% increase over the same quarter last year's result of $139.9 million in sales. Net earnings came in at $20.1 million, up 34.9% from last year's $14.9 million result or on a per share basis, this worked out to$.17/share, up over 100% from $.07/share last year.

Longer-term, if we review the Morningstar.com "5-Yr Restated" financials on ESE, we can see the steady rise in revenue from $397 million in 2003 to $528 million in 2007 and $651 million in the trailing twelve months (TTM). Earnings have been a bit less consistent increasing from $1.00 in 2003 to a peack of $1.70 in 2005, before dipping back to $1.20 in 2006 then increasing steadily once again to $1.70/share in the TTM. No dividend is paid. The outstanding shares have been very stable at 26 million in 2003 and 26 million in the TTM.

Free cash flow is positive but decreasing (not a positive sign imho), with $60 million in 2005, dipping to $50 million in 2006 and $26 million in 2007. The balance sheet appears adequate with $23 million in cash and $223 million in other current assets, resulting in a total of $246 million in current assets which when compared to the $135.1 million in current liabilities, yields a current ratio of 1.82. The company has an additional $308.9 million in long-term liabilities per Morningstar.

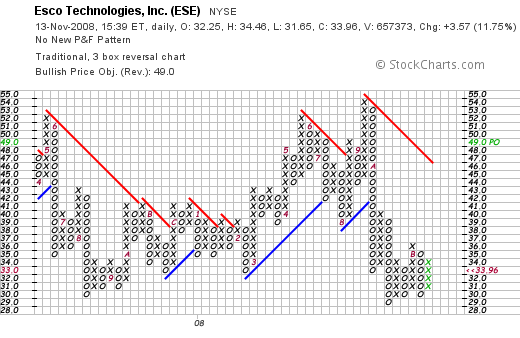

Looking at the "point & figure" chart on Esco from StockCharts.com, we can see that after peaking at $54 in September, 2008, the company continues to be under pressure, bottoming at $29 in October, 2008, and appearing to be trying to work its way slowly higher. This appears fairly typical for the severe bear market that we find ourselves in today.

In terms of valuation, looking at Yahoo "Key Statistics" on Esco (ESE), we can see that the company is a mid-cap stock with a market capitalization of $883.89 million. The trailing p/e is 22.94, but with the rapid growth expected, the forward p/e (fye 30-Sep-09) is only 15.57. Thus, the PEG ratio comes in at a very reasonable 0.61.

In terms of valuation, utilizing the Fidelity.com eresearch website, we can see that the Price/Sales (TTM) ratio of 1.33, is higher than the industry average of 0.66. Even by profitability, the Retorn on Equity (TTM) comes in at 10.25%, compared ot the industry average of 20.87%. Neither of these indices come out particularly flattering to ESE relative to its peers.

Finishing up with Yahoo, there are 26.04 million shares outstanding with 25.34 million that float. Currently, there are 2.42 million shares out short (as of 10/10/08), representing 8.1 trading days. This is significant relative to my own arbitrary '3 day rule' for short interest.

As noted, no dividend is paid, and the last stock split was a 2:1 split back on September 26, 2005.

To summarize, being under my 5 position minimum (my own trading rule), I had a 'permission slip' to be adding another position to bring be back to my minimum in equities exposure. Esco made the list today, was a fairly good fit for my blog and my strategy and I purchased a 'reduced' position for my trading account. The latest quarterly report was strong, the last 5 years have been strong, valuation is reasonable with a PEG well under 1.0, but the chart looks rather dismal.

It is good that I have a little price appreciation today as so many of the time I have purchased shares recently on a positive earnings announcement, many have declined on profit-taking even the same day. The follow-through today is encouraging.

Thanks again for stopping by and visiting! If you have any comments or questions, please leave them on the website or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Wednesday, 12 November 2008

Anticipating a Bull Market: Reconsideration of Position Size

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your investment advisers prior to making any investment decisions based on information on this website.

I have been tinkering with my investment strategy recently. As I have discussed previously, my portfolio management system requires me to be invested with at least some exposure to the market, regardless of the health or tone of the underlying business climate.

I have been tinkering with my investment strategy recently. As I have discussed previously, my portfolio management system requires me to be invested with at least some exposure to the market, regardless of the health or tone of the underlying business climate.

For me that means owning at least 5 positions at most times (I am presently at 4 waiting to find something to buy to bring it back to 5 after selling my BEAV shares this morning). I do this because my own strategy depends on the actions of my own holdings to let me know whether I should be moving further into equities or moving instead towards cash.

Sales on good news generate 'buy signals' to add positions (assuming I am under 20 holdings), and sales on bad news--or declines--generate the opposite signal---that is they instruct me to 'sit on my hands'--unless I am at my minimum of 5--in which case these sales also give me a buy signal (as I received with my sale of my BE Aerospace shares this morning).

However, instead of buying a 'full' position, I am purchasing a reduced position equal to 1/2 of the average size of the remaining four positions. Thus, instead of just continuing to compound my losses over and over on the way down, I do a bit of compounding but continue to pull back from stocks each transaction with continuing reduced exposure to equities.

I hope you follow.

I have assumed that on the way up, I would instead add an 'average' of the remaining positions as the size of the new holding.

But that isn't enough.

Otherwise I would be adding a tiny position resulting from past sales. I need to be a bit more aggressive than that.

With that in mind, I am proposing on the way up that I shall be adding positions that are 125% of the average. Thus in that way, I shall be putting my foot on the accelerator just like I put my foot on the brake pedal when times are bad. I need to commit greater amounts of funds to the market as the eventual bull market unfolds.

Is 125% the right amount? I don't know. It took me awhile to get to the 1/7th position sales on the upside. If you all have a better idea, please feel to leave your comments on the blog or email me at bobsadviceforstocks@lycos.com.

This is all new to me. But it makes intrinsic sense in the midst of the chaos that is Wall Street.

Wish me luck. I wish all of you luck as well!

Yours in investing,

Bob

BE Aerospace (BEAV) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

There are many things to like about BE Aerospace (BEAV). That is why I recently added it to my portfolio. Things like the great recent quarterly result, and the "5-Yr Restated" financials from Morningstar.com.

There are many things to like about BE Aerospace (BEAV). That is why I recently added it to my portfolio. Things like the great recent quarterly result, and the "5-Yr Restated" financials from Morningstar.com.

But this blog is not about a love-fest of stocks. It is about building a portfolio of terrific stocks of terrific companies and then managing that portfolio of stocks in response to the vagaries of the market--the bullish and bearish influences that bear down upon each of us.

Recently I have modified my trading strategy to acknowledge that there are times that are so terribly negative that naively replacing stocks on 8% losses and continuing to maintain the same size of positions only allows a certain compounding of losses.

To deal with the negative environment that drives me down to under 5 positions (my minimum), I have chosen to do two things: to reduce my replacement size of a position being replaced to maintain that minimum to 1/2 of the average size of the remaining positions, and to allow each stock to dip to a 16% loss (instead of an 8% loss) to hopefully avoid unnecessarily replacing stocks that are victim of the increased volatility we are all observing.

Directly to the point, my BE Aerospace (BEAV) stock hit a 16% loss this morning, and I sold my 215 shares at $9.4154. I had just purchased these shares 10/27/08 at $11.23, thus I had a loss of $(1.81) or (16.15)% since purchase.

With my holdings now down to 4, I have another "permission slip" in my pocket to purchase a new position to make 5, however, I am not in a big hurry to do anything. After having burnt my fingers over and over in this treacherous market, the nickel feels rather cool in my pocket.

Doesn't appear to be burning a hole at all this time!

Thanks again for visiting. I shall continue to update my own actions and thoughts on this market.

If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Wednesday, 5 November 2008

Expeditors International of Washington (EXPD) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I do not like to get whipsawed and do so publicly. And yet, I am committed to implementing my own idiosyncratic system of limiting losses and responding to market influences in some sort of rational fashion.

I do not like to get whipsawed and do so publicly. And yet, I am committed to implementing my own idiosyncratic system of limiting losses and responding to market influences in some sort of rational fashion.

Earlier this morning the market handed me my quick 8% loss on Expetitors (EXPD) and I sold my 45 shares at $36.8506. These shares were just purchased yesterday, yes yesterday, at a price of $40.1894. Thus, my loss was $(3.34) or (8.3)% since purchase. With this being the sixth position in my portfolio, I am implementing my (8)% loss limit, and now back to five positions, my loss tolerance is increased to (16)% with the 'final five' of my 20 position maximum.

I hope this all makes sense.

My sale of EXPD is not representative of any dislike of this stock. I find the numbers on this company intriguing, the consistency of growth, etc.. My sale is just a reflection of my own amateur attempt of limiting losses and responding to market influences. The volatility is just killing me though.

I know there are lots of readers over at Seeking Alpha who are pointing out the VIX levels and I am learning this the hard way.

Since my sale is at a loss, and I still am now at 5 positions (my minimum), I shall not be replacing this holding.

Thank you for visiting. If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Rock-Tenn Co. (RKT) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please consult with your professional investment advisers before making any investment decisions based on information on this website.

That "nickel" was burning a hole in my pocket! I always talk about having a nickel in my pocket when I have sold a portion of one of my holdings at a gain. Indeed yesterday my recently purchased holding, WMS Industries hit a first appreciation target and I sold 1/7th of my small holding. These sales are the barometers I use to determine my own equity exposure in the market. With that sale, I started to look for a new position that met my own criteria for a holding, and a purchase that would be at the 'average' of my remaining holdings in size.

That "nickel" was burning a hole in my pocket! I always talk about having a nickel in my pocket when I have sold a portion of one of my holdings at a gain. Indeed yesterday my recently purchased holding, WMS Industries hit a first appreciation target and I sold 1/7th of my small holding. These sales are the barometers I use to determine my own equity exposure in the market. With that sale, I started to look for a new position that met my own criteria for a holding, and a purchase that would be at the 'average' of my remaining holdings in size.

Looking first to the list of top % gainers, I came across Rock-Tenn (RKT) which closed at $32.94, up $3.79 or 13% on the day. I purchased 93 shares at $33.06.

Rock-Tenn climbed yesterday after releasing 4th quarter 2008 results. The company reported that it earned $28.4 million or $.74/share, up from $19.7 million or $.50/share last year. "Excluding one-time items, Rock-Tenn earned $34.5 million or $.90/share."

I place great significance on expectations of earnings in trying to determine how 'good' an earnings report really is. In this case, the company easily outperformed expectations as analysts polled by Thomson Reuters had been expecting earnings of $.84/share.

But of course, a single quarterly result isn't enough to get my own 'seal of approval' on a stock!

Reviewing the Morningstar.com '5-Yr Restated' financials on RKT, we can see the steady growth in revenue from $1.4 billion in 2003 to $2.3 billion in 2007 and $2.7 billion in the trailing twelve months (TTM).

Earnings, however, have been far more erratic, dipping from $.85/share in 2003 to a low of $.49/share in 2005. Since 2005, earnings have grown to $.77/share in 2006, $2.07/share in 2007, and per Morningstar a dip to $2.07/share in the TTM. However, with the latest quarterly result, we can see that the increase is 'back on track'.

The company has a record of paying dividends and has been increasing that dividend from $.32/share in 2003 to $.39/share in 2007 and $.40/share in the TTM.

Outstanding shares have been fairly stable with 35 million outstanding in 2003 increasing to 38 million in the TTM.

Free cash flow is positive and growing with $99 million in 2005, $160 million in 2007 and $175 million in the TTM. The balance sheet appears adequate with $57 million in cash and $618 million in other current assets, compared to $636.5 million in current liabilities---a current ratio just over 1.0, and $1.7 billion in long-term liabilities on the balance sheet.

This isn't a perfect fit to my own strategy of steady earnings growth and solid balance sheets. But the overall fit works for me.

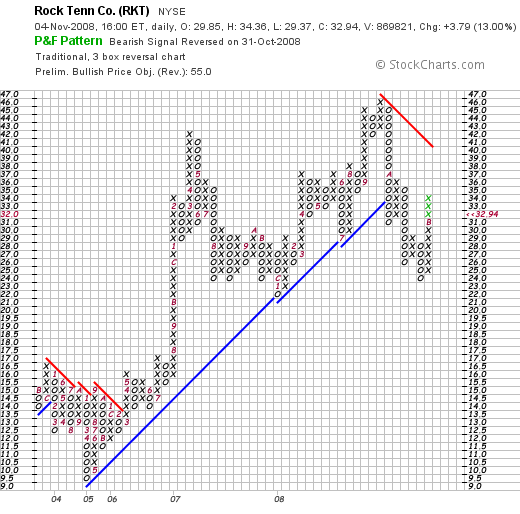

Let's take a quick look at the 'point & figure' chart from StockCharts.com:

We can see that the price moved higher between April, 2005, when it dipped to a low of $9.50, to a peak of $46 in September, 2008. The stock broke down after that dipping to a low of $24 in October, 2008, just last month. The stock appears to be attempting to break through resistance at $40, but actually has a ways to go.

Like so many stocks in today's bear market, the charts are under pressure.

With my own 'leash' on every investment, and my own signal to be adding a position, this one works for me. This company that "manufactures packaging products, paperboard, and merchandising displays in North America" according to the Yahoo "Profile". This is a mid-cap stock with a market cap of $1.26 billion, a p/e of 17.33, and a PEG of 1.18 per the Yahoo "Key Statistics".

Wish me luck.

I shall try to keep you posted with all of my holdings, my own trades, my own thoughts and fears and hopes and aspirations in the market.

By the way, congratulations are in order to all of my friends who supported Obama for President! For those of you who supported McCain or others, I feel your pain as well and offer you my understanding.

But isn't it great that all of the campaigning is over?

If you have any comments or questions, please feel free to leave them on the blog, or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Tuesday, 4 November 2008

Expeditors International of Washington (EXPD) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Earlier today I sold my shares of Graham (GHM) on a plunge in the stock price below my purchase price on what appeared to be a reasonably good earnings report. I suppose with the rise in the price of oil and this earnings report, the stock reacted to the news. It doesn't matter to me. My sale is based on the price performance of my holding and not my own expectations of the future prospects.

Dipping below my minimum of 5 positions generated a 'buy signal' for me to replace it with a position of reduced size (1/2 of the average size of the remaining positions.) I have initiated purchases based on sales on good news to be sized at the average of the remaining holdings.

Looking through the lists of top % gainers on the NASDAQ today, I came across Expeditors (EXPD) and felt it would fit well into my own portfolio.

Let me share with you briefly why I made this decision and decided to purchase 45 shares of EXPD at $40.19. As I write, EXPD is trading at $38.68, a bit below my own purchase, trading up $6.68 or 20.88% on the day.

First of all, what drove the stock higher today was the announcement of 3rd quarter 2008 results. Earnings came in at $85.6 million during the 3rd quarter, up from $74.3 million during the same period last year. Diluted earnings per share worked out to $.39/share this year, up from $.34/share last year. The company reported "same-store" results, with same store net revenue climbing 11%, and same store operating income climbing 13% year-over-year. Revenue for the quarter came in at $1.56 billion, up from $1.41 billion last year.

The company exceeded expectations on earnings and apparently met expectations on revenue results. Analysts had been looking for $.37/share (the company beat this by $.02).

Longer-term, if we check the Morningstar.com "5-Yr Restated" financials on EXPD, we can see that revenue has been steadily increasing with $2.6 billion in sales in 2003, climbing to $5.2 billion in 2007 and $5.6 billion in the trailing twelve months (TTM).

Earnings have also steadily increased from $.46/share in 2003 to $1.21/share in 2007 and $1.28/share in the TTM.

The company pays a dividend and has been increasing the dividend annually from $.08/share in 2003 to $.30 share in the TTM.

Outstanding shares have been very stable with 216 million shares in 2003, increasing only to 221 million in the TTM.

Free cash flow has been positive and growing from $176 million in 2005 to $243 million in the TTM.

The balance sheet appears solid with $703 million in cash and $1.04 billion in other current assets. This yields a current ratio of 2.0. The company reports only $95 million of long-term liabilities.

Looking at some valuation numbers, we can see that this is a large cap stock with a market cap of $8.22 billion according to Yahoo "Key Statistics".

The trailing p/e is 30.27 with a forward p/e (fye 31-Dec-09) of 25.43. The PEG (5 yr expected) works out to an acceptable 1.51.

Yahoo reports 213 million shares outstanding with 209 million that float. 9.18 million shares are out short representing a short ratio of 2.2 days. The company, as noted, pays a dividend with a forward yield of 1.0%. The last stock split was a 2:1 split back on June 26, 2006.

And the chart?

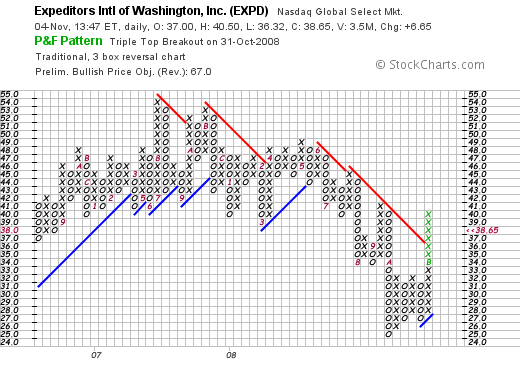

If we examine a

'point & figure' chart on EXPD from StockCharts.com, we can see that the stock has been relatively weak since peaking at $54 in August, 2007, and has traded as low as $25 in October, 2008. The stock has recently broken through resistance at the $36 level, and short-term appears to be a bullish chart.

To summarize, with my sale of Graham (GHM) putting me under 5 positions, my own strategy requires a minimum of 5 holdings in my portfolio (with my own maximum of 20 positions). I set out to find a new holding starting with the top % gainers lists. Expeditors was performing well today, and a closer look reveals a terrific earnings report, a longer-term record and financial fundamentals quite impressive, and a less than impressive chart.

But it was enough to get me to bite and nibble away I went.

Thanks again for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Graham Corp (GHM) and WMS Industries (WMS) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

There is no doubt that Graham (GHM) a relatively thinly-traded AMEX stock has been one of the most volatile of my holdings. It has performed for me on the upside, and I have burned my fingers on this stock more than once. Add today to that list of burnt fingers!

There is no doubt that Graham (GHM) a relatively thinly-traded AMEX stock has been one of the most volatile of my holdings. It has performed for me on the upside, and I have burned my fingers on this stock more than once. Add today to that list of burnt fingers!

Graham (GHM) was purchased in my Trading Account last month, purchased 10/8/08 at a cost basis per share of $16.34. I sold my first portion of Graham at a 30% gain only 5 days later on 10/13/08 at $22.37. Today, after the 2nd quarter 2009 earnings report was released, the stock slumped, even though the rest of the market was enjoying an Election Day rally. As I write, GHM is trading at $15.43, down $(5.52) or (26.35)% on the day.

I sold my 360 remaining shares of Graham (GHM) earlier this morning at $15.441. This represented a loss of $(.90) or (5.50)% from my purchase.

This sale was not at a 16% loss limit as I have discussed in my previous posts that I have been implementing for my remaining 5 positions. But this represents my still employed strategy of selling stocks if they break through my purchase cost if I have sold once at a gain. And this is exacly what has happened.

Going down to 4 positions, this entitled me to add a new position, and I did purchase 45 shares of Expeditors Intl (EXPD) at $40.19/share. I shall try to discuss this later today.

But what I wanted to discuss further was my partial sale of WMS Industries, sold almost immediately after my Graham sale, but this time on 'good news' due to an appreciation in that stock's price!

WMS Industries (WMS) is a recent purchase of mine, having acquired 96 shares at a cost basis of $20.12 on 10/28/08. This morning I sold 1/7th of my WMS holding or 13 shares at $26.67. This represented a gain of $6.55 or 32.6% since purchase. My next targeted appreciation point for a sale of 1/7th of my remaining shares would be at a 60% gain or 1.6 x $20.12 = $32.19. On the downside, just like my sale today of my Graham (GHM) shares, after a single partial sale at a 30% appreciation level, I sell my shares should they decline or pass through break-even. Thus remaining shares would be sold if WMS should decline to $20.12.

WMS Industries (WMS) is a recent purchase of mine, having acquired 96 shares at a cost basis of $20.12 on 10/28/08. This morning I sold 1/7th of my WMS holding or 13 shares at $26.67. This represented a gain of $6.55 or 32.6% since purchase. My next targeted appreciation point for a sale of 1/7th of my remaining shares would be at a 60% gain or 1.6 x $20.12 = $32.19. On the downside, just like my sale today of my Graham (GHM) shares, after a single partial sale at a 30% appreciation level, I sell my shares should they decline or pass through break-even. Thus remaining shares would be sold if WMS should decline to $20.12.

These two sales demonstrate my philosophy of selling both on bad and good news. Both of these sales have triggered buys in different fashions. My Graham (GHM) sale brought me under my minimum of 5 positions and I did go ahead and purchase a small position of EXPD (1/2 of the average size of my remaining positions), and now have a 'permission slip' to be adding a 6th position which would be slightly larger, actually at the average size of my remaining holdings.

Thanks so much for stopping by and visting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 2 November 2008

A Reader Writes "Do I understand correctly...?"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

One of my favorite activities on this blog is to receive and respond to emails. I am always interested in discussing stocks and my methods with fellow investors who are also interested in understanding investment methods.

One of my favorite activities on this blog is to receive and respond to emails. I am always interested in discussing stocks and my methods with fellow investors who are also interested in understanding investment methods.

I received a great letter from Don who is a fellow Covestor participant over on the Covestor website who also has a great website, Crossing the Threshold. Please visit Don's website and tell him 'Bob sent you!'

I received a great letter from Don who is a fellow Covestor participant over on the Covestor website who also has a great website, Crossing the Threshold. Please visit Don's website and tell him 'Bob sent you!'

But let me get right to Don's letter as he has some questions for me about my own idiosyncratic approach to buying and selling stocks and managing my portfolio in the face of a volatile market that swings from bear into bull and leaves many an investor scrambling to figure the appropriate strategy.

Don wrote:

"Hi Bob,

I started a fairly ambitious project in response to your note about the changes to your system, but just plain ran out of time this weekend. I'll keep at it. I think you'll find the results interesting.

And on a semi related note, I attended a seminar on Fidelity's Wealth Lab Pro system testing software, and, as a minimum it looks interesting. Once you have the rules for a system set up, you can run it on any portfolio of stocks going back 30 years. It's virtually instantaneous.

Do I understand correctly that if you're at 6+ trades, that you'll liquidate any trade at +30%, and then liquidate another 1/7th at each of these levels, "30, 60, 90, and 120% appreciation, then 180, 240, 300, 360 and 450% appreciation targets, then 540, 630, 720 and 810% appreciation levels, etc."

My question is this, if you buy 700 shares, do you sell 100 at each of those levels, or, does it mean 100 (leaving 600), then 85 (1/7th of 600), then 74 (1/7 of 515), etc?

Thanks, and good luck in this market!

Don"

First of all I would like to thank you Don for taking the time to write! I have enjoyed reading many of your own entries and watching you gather many 'fans' of your own on your Covestor page. There is nobody on Covestor with as much enthusiasm as you have in teaching and sharing ideas with fellow investors!

But let me get back to your letter.

I will not spend much time talking about stock selection as you understand some of the basic premises with recent price momentum, solid recent quarterly and longer-term results, positive free cash flow, stable outstanding shares, and reasonable balance sheets as ideas that many of us share.

Currently I am trying to keep my portfolio at between five and twenty positions. As you know, as my stocks appreciate to set appreciation levels (the 30%, 60%, 90%, 120%, 180, 240, 300, and 360%, and then 450, 540, 630%....etc.), I have chosen to sell a portion of my holding.

Initially selling 1/4 of my remaining shares, I have gradually reduced this amount and have now chosen to sell 1/7th of remaining shares. Thus if I had 700 shares, I would first sell 1/7th of 700 or 100 shares, then 1/7th of 600 shares or 85 shares, then 1/7th of 515 shares or 73 shares, etc.

With these sales at individual positions reaching targeted levels, I use these sales as 'signals' that give me 'permission slips' to be adding a new position (assuming I am below my maximum of 20 holdings. If at the maximum, I simply move the sale of the shares into my cash holding.)

However, I have not previously detailed my amount of a new position to purchase. Mathematically, I have recently chosen to purchase a new position equal to the average size in dollars of the remaining positions. I do this as long as I have at least 5 positions in my portfolio.

As you know, I have sales of positions on declines as well. Simply put, after an initial purchase, I sell my entire position at an 8% decline if I have not sold these shares previously, and I am at 6 or greater number of holdings. At 5 or less holdings, I am assuming that the bear market is severe and my tolerance has now been increased to a 16% decline.

After a holding has reached the first partial sale point at a gain, I move my sale point up from an 8% loss to break-even. After more than a single sale at a gain, I have moved my sale point up to 1/2 of the highest appreciation point for a sale of the entire position. Again I emphasize that sales on the downside are entire positions rather than partial sales as I implement on the upside.

As I get down to 5 positions, my sale target changes to a uniform 16% loss from the purchase price.

But I believe in maintaining 5 positions as a minimum. Even if I am in a bear market and am handed losss after loss. It is my reliance on my own exposure to equities that determines my own actions and response in the market. Much like a parrot in a coal mine, these positions offer me a rational (?) approach to determining the market environment and guiding me in my own investment decisions.

I hope you are following me.

In addition, I have changed something else. Previously, I have been pretty 'seat of the pants' in determining the size of the positions I shall be buying. If I am buying shares in a position just to get me back to my 5 position minimum, obviously, the market environment is pretty awful (as it has been recently) and I should be working to reduce my exposure. Since I am determined to have those five positions, I should at lease reduce the size of those holdings---and this is one of the changes I have implemented--these replacement holdings are now set as 1/2 of the average size of the remaining positions.

If I get up to 5 positions and I get a permission slip to be buying a new position as one of my 5 has hit a sale point on a gain----then I increase the size of the new position back to the 'average' of the remaining positions I hold. Thus, as I move back up to 20 positions, the holdings should increase, I continue to be in a relatively bullish posture until I get down to 5 positions---as I should---because between 5 and 20, I only get 'buy signals' because one of my holdings has been performing properly and has hit a sale point on an upward gain.

However, at 5 or less positions, as I sell them, I am buying new positions only to get my portfolio back to 5 and thus I am paradoxically getting a buy signal after selling something at a loss. Thus, with these sales, I still replace to get back to 5, but buy a smaller position---1/2 of the average size of the remaining holdings.

Don, I hope this answers your basic question. I know that my entire process seems far more complicated than necessary. However, I believe it is a logical process and look forward to hearing more of your thoughts on this and whether you think it might in fact work!

If you have any other questions or comments, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Thursday, 30 October 2008

A Few Comments on Stock Picks and Trading Philosophy and This Blog

Hello Friends!

I start out each entry or almost every entry with that comment because I mean it. I also mean it when I say I am an amateur. So always keep that in mind.

You may have reached this website because you searched "stock pick" on Google. Or maybe you were looking for "stock advice" or maybe you have been here before and understand what I am doing as I write my stock selections and share with you my actual trades and results.

That doesn't really matter.

For picking stocks may well be the easiest part of the entire equation. There are many ways to evaluate stocks, for the most part I am a momentum investor. I select stocks with daily momentum of price, recent momentum of earnings, longer-term momentum of improving fundamentals, with reasonable financials, desirable valuation, and an acceptable chart.

I don't always get all of those criteria met, but those are the bulk of the things I consider. I am not much different from many other investors who similarly look to select stocks with similar criteria.

But a larger question remains. When do you buy a stock? When do you sell a stock? And how do you respond to the market environment in making your decision--in other words--is there any way to avoid bear markets by minimizing equity exposure during these difficult times, and is there similarly any way to maximize equity exposure during bull markets and positive market environments? And can we do this automatically?

It is tough enough to select a stock, but managing your portfolio and responding automatically to market action is even a larger demand put upon my own strategy.

And to top it off, I am trying to do this publicly. To share my successes and failures with all of you and try to stick to a strategy in a disciplined fashion. And my strategy isn't refined, I am learning that I need to make changes as I implement my own decisions. I still lose money when stocks decline and make money when stocks advance.

But if I can develop an approach that adjusts automatically to the market, that guides me to select certain stocks, that lets me know when to be selling those same positions--whether in part or in entirety--I shall achieved something far greater than any particular 'great call'.

Thank you for coming along with me in this journey.

Yours in investing,

Bob

Newer | Latest | Older