Stock Picks Bob's Advice

Sunday, 17 December 2006

St Jude Medical (STJ) "Long-Term Review" A New Entry in Stock Picks!

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decision based on information on this website.

This blog is now over 3 1/2 years old! It is walking and talking and I hope you enjoy my entries! I do a weekend review on the blog, and I am a bit over a year out from those reviews. It occurred to me that I needed to once again dig back into the early entries, and try to find out how these stocks are doing. I want to try to keep these reviews briefer (is it possible) and mostly just examine the price and the latest stock chart. Let's at least start out that way.

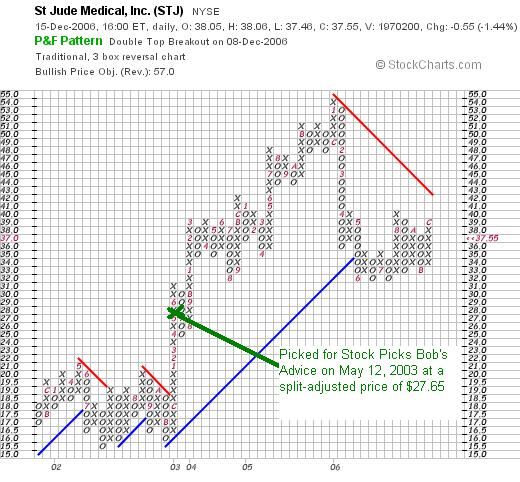

This blog commenced on May 12, 2003, when I wrote up St Jude Medical (STJ). I wrote:

"This is one I picked up today. STJ is the stock symbol. I do not as I write and publish this own any shares. Am thinking about suggesting this to my stock club. Company had a great day today with a nice move on the upside. Last Quarter was good and the past five years have been steady growth. Closed at $55.30 up $2.92. So the daily momentum helped it make the list."

Wouldn't it be nice if all of my entries were that short! You of course, can examine and review all of my entries by date by 'clicking' on the dates along the left side of the blog.

STJ actually had a 2:1 stock split on November 23, 2004, making my effective stock pick price actually $27.65. STJ closed at $37.55 on December 15, 2006, giving my first pick an appreciation of $9.90 or 35.8% since posting.

I hope these longer-term views of past stock picks....I shall try to do them in the order they are posted as long as they are still traded....and write them up on intervals.

Thanks again for visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. If you get a chance, be sure and visit my Stock Picks Podcast Site where I discuss many of the same stocks and investing issues that I review here on the blog!

Have a great week investing everyone!

Bob

Posted by bobsadviceforstocks at 10:12 PM CST

|

Post Comment |

Permalink

Updated: Monday, 18 December 2006 7:44 AM CST

"Looking Back One Year" A review of stock picks from the week of August 15, 2005

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

The weekend is almost over and I really need to get to the 'review'! I like to examine past stock picks and find out how they would have turned out if I had indeed purchased them. I occasionally do buy stocks for my trading portfolio, but when I do, I post a "trading transparency" entry! The overall performance is the average of each of the performances from the week selected. This assumes a 'buy and hold' strategy.

In practice, I advocate and utilize a disciplined portfolio management system that requires me to sell any stock which incurs a small (8%) trading loss. It also requires me to sell portions (1/6th of remaining shares) at targeted apprreciation points. Thus, this difference in portfolio management would certainly affect portfolio performance. However, for the ease of review, I have chosen to consider that I am employing a buy and hold strategy and have purchased equal-$ amounts of each stock discussed.

On August 16, 2005, I "revisited" Fargo Electronics (FRGO) when it was trading at $17.76. This was the second time I had written up this stock, first writing up Fargo on October 6, 2003, when it was trading at $14.82/share. On May 24, 2006, Assa Abloy's HID Global Corporation was reported to have completed plans for the acquisition of Fargo (FRGO) at a price of $25.50/share. Based on the latest pick price of $17.76, this represents a gain of $7.74 or 43.6% since posting.

On August 16, 2005, I "revisited" Fargo Electronics (FRGO) when it was trading at $17.76. This was the second time I had written up this stock, first writing up Fargo on October 6, 2003, when it was trading at $14.82/share. On May 24, 2006, Assa Abloy's HID Global Corporation was reported to have completed plans for the acquisition of Fargo (FRGO) at a price of $25.50/share. Based on the latest pick price of $17.76, this represents a gain of $7.74 or 43.6% since posting.

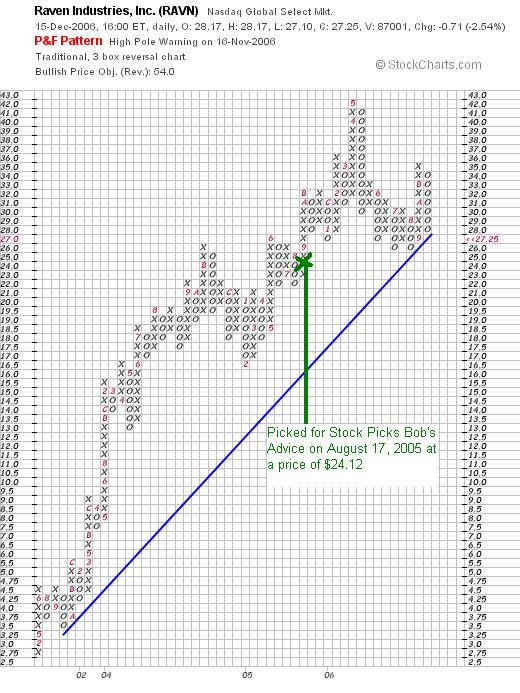

On August 17, 2005, I posted Raven Industries (RAVN) on Stock Picks at a price of $24.12. RAVN closed on December 15, 2006, at a price of $27.25, for a gain of $3.13 or 13.0%.

On August 17, 2005, I posted Raven Industries (RAVN) on Stock Picks at a price of $24.12. RAVN closed on December 15, 2006, at a price of $27.25, for a gain of $3.13 or 13.0%.

On November 16, 2006, Raven Industries (RAVN) announced 3rd quarter 2006 results. For the quarter ended October 31, 2006, net sales rose 6% to $57.4 million from $54.1 million in the same quarter in 2005. Net income came in at $7.0 million, up slightly from $6.9 million or $.38/share, up from $.37/share last year.

As noted, the company also issued guidance for relatively 'flat' fourth quarter earnings compared to the prior year. So even though I give them a "thumbs-up" it isn't a very enthusiastic one at that!

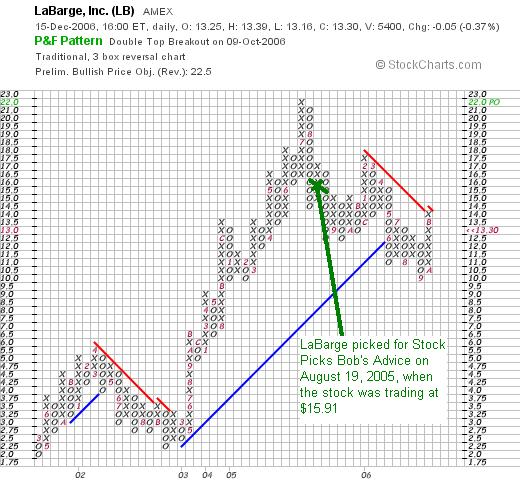

On August 19, 2005, I picked LaBarge (LB) for Stock Picks when it was trading at $15.91. LaBarge closed at $13.30 on December 15, 2006, for a loss of $(2.61) or (16.4)% since being posted.

On November 2, 2006, LaBarge (LB) reported 1st quarter 2007 results. For the quarter ended October 1, 2006, net sales came in at $49.9 million, up 26% from the $39.6 million in the first quarter of 2006. Net earnings for the quarter increased 19% to $2.4 million or $.15/diluted share from $2.03 million or $.13/diluted share in the 2006 first fiscal quarter.

So how did I do picking stocks back in 2005 for the week of August 15th? I picked one stock (Fargo) that was acquired on a significant gain, one stock had a small gain another had a small loss for an average gain of 13.4%.

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to drop me a line at bobsadviceforstocks@lycos.com or leave your comments right on the blog. If you get a chance, please visit my Stock Picks Podcast Website, where you can download sound files of me discussing many of the same stocks I write about herre on the blog!

Have a great week investing everyone!

Bob

A Reader Writes "I am intrigued by Zoltek (ZOLT)...."

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

A few moments ago I was checking my email and saw a notice that my good friend George K. had written a note on the blog. George and I are both members of the same stock club and have gotten to be good friends over the last few years. George wrote:

A few moments ago I was checking my email and saw a notice that my good friend George K. had written a note on the blog. George and I are both members of the same stock club and have gotten to be good friends over the last few years. George wrote:

"Hi Bob,

Again, thank you for your Blog...I really enjoy the way you have been editing the point/figure charts with your comments on buy/sell points...very insightful...

...Now my question...I am intrigued by Zoltek (ZOLT) and would really appreciate your comments...carbon fiber production has usually been in composite braking systems, but recently wind entergy, and sporting goods have near-term potential. I'd be very interested in your take.

Again, thanks for the fine blog

Geo"

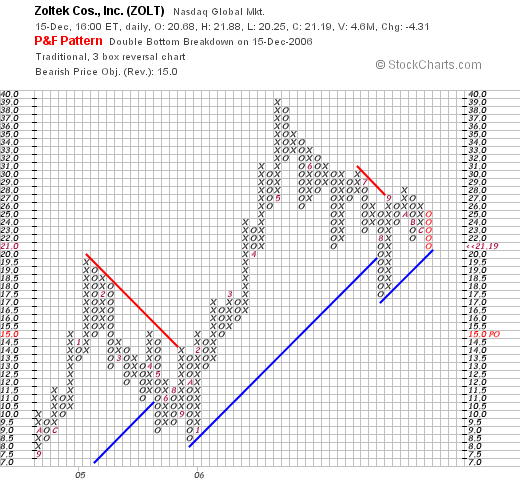

As I wrote right on the blog, I am very apprreciative of your continued support, interest, and participation on the blog. As transparency is my foremost concern on the blog, I did point out that you are in reality a good friend of mine and fellow stock club member! But that doesn't mean you can't participate here and write comments and make inquiries! Please continue George! Let me take a look at Zoltek (ZOLT) and I will give you my off the cuff 'take' on the stock today. ZOLT closed at $21.19 on 12/15/06, down $(4.31) or (16.9)% on the day.

My comments on Zoltek do not mean that I am 'picking' this stock for this blog. I frankly don't know if it meets my 'criteria', but I would be happy to review the company

My own personal awareness of this Carbon Fiber company, came while still a subscriber to the Cabot Market Letter, a subscription that I have allowed to lapse. I did find the newsletter provocative and like everything that I read, I must assume that in some fashion it affected my own philosophy of investing. If so, for that I am thankful.

My own personal awareness of this Carbon Fiber company, came while still a subscriber to the Cabot Market Letter, a subscription that I have allowed to lapse. I did find the newsletter provocative and like everything that I read, I must assume that in some fashion it affected my own philosophy of investing. If so, for that I am thankful.

Several years ago, Zoltek (ZOLT) was a favorite of Timothy Lutts, the editor of the letter. You can read more about that episode here. I am sure that I was even a shareholder of Zoltek stock. I have not owned any shares of this company for at least several years and do not own any shares or options now.

What exactly does this company do?

According to the Yahoo "Profile" on Zoltek (ZOLT), the company

"...through its wholly owned subsidiaries, engages in the manufacture, marketing, and development of carbon fibers for various applications."

"...through its wholly owned subsidiaries, engages in the manufacture, marketing, and development of carbon fibers for various applications."

Is there any recent news of significance?

Apparently the biggest news story affecting this company was the fourth quarter 2006 results.

What were the latest quarterly results?

On December 14, 2006, Zoltek reported 4th quarter 2006 results for the quarter ended September 30, 2006. For the quarter, net sales increased 60% to $23.8 million from $14.9 million in the fourth quarter of fiscal 2005. However due to a litigation expense of $(23.1) million, the company reported a net loss of $(15.7) million from continuing operation, compared to a net loss of $(7.6) million in the same quarter last year. This works out to a net loss per diluted share of $(.89), compared to a net loss last year of $(.57)/diluted share.

These results failed to meet analysts' expectations of revenue of $31.3 million according to Thomson First Call. The company also reduced guidance on the upcoming first quarter with guidance of 'more than $30 million' suggested. Analysts are looking for revenue of $37.1 million in that quarter. In addition, the company is delinquent in its filings of its 2006 10-K as it works to 'complete documentation and other arrangements related to the funding of an appeal bond for its litigation.'

Briefly, let me just assert that in my perspective, I require a company to not only grow its revenue, as ZOLT did, but to be profitable and have growing earnings. Not only did the company lose money, but it expanded its loss year-over-year. If we take out that litigation expense, the company actually is profitable. However, revenue also failed to meet expectations and the company reduced guidance for the upcoming quarter. There are just too many questions about these results for me to endorse this one.

How about longer-term results?

Let's take a look at the Morningstar.com "5-Yr Restated" financials on this stock. First of all, a positive note is the revenue 'turn-around'. While dropping revenue from $43 million in 2001 to a low of $34 million in 2003, the company then did turn that around to $40 million in 2004, $60 million in 2005 and $88 million in the trailing twelve months (TTM). There isn't a single profitable year on this page :(. Losses initially declined from $(1.91) in 2001 to $(.48)/share in 2002. But get this: each and every year, losses have been GROWING and not shrinking or even turning profitable! The company lost $(.96)/share in 2003, $(1.40)/share in 2004, $(2.23)/share in 2005 and $(2.53)/share in the TTM.

To top this off, the company has been increasing its shares outstanding about as fast as it has been growing its revenue: 17 million shares in 2001 and 18 million in 2005, but 26 million reported in the TTM.

Free cash flow is NEGATIVE and growing increasingly poor the past few years. $(6) million in 2003, $(13) million in 2004, $(24) million in 2005 and $(29) million in the TTM.

The balance sheet looks find to me with $19.7 million in cash and $51.2 million in other current assets. Compared with the $22.4 million in current liabilities, this yields a current ratio of 3.17, about the strongest number on this page. The company is also reported to have $34.8 million in long-term liabilities.

What about the chart?

If we review the StockCharts.com "Point & Figure" chart on Zoltek, we can see a fairly strong couple of years of stock price movement from $7.50 in late 2004 to a recent high of $39 in May, 2006. The company has been under some pressure recently dropping to the $21 level, but still the chart shows relatively good strength for what appears to me to be very anemic fundamentals.

Summary: What do I think about this stock?

In general, in my Peter Lynch investing perspective, as you appear to be using in your letter, tells me that carbon fiber does have terrific potential. In fact, one potential use that you didn't discuss is in aviation, where the new Boeing 787 using this material in a very significant fashion. As has been reported:

"Commercial aerospace is considered a major driver of the capacity expansions: Each Boeing 787, for example, will use about 165,000 lb of carbon fiber composites; each Airbus A380 will use about 65,000 lb."

But you know that I am not a Peter Lynch investor, at least not in the sterotyped fashion. This is in no way a critique of his philosophy. It is just the usual 'buy what you know' type advice isn't my approach.

There are so many great stocks out there and I cannot buy them all! I stick with stocks with a certain profile that I write about over an over. I want them to have consistent revenue and earnings growth. I want them to be profitable and free-cash positive. With great balance sheets, valuation, and charts. I want it all!

ZOLT is losing increasing amounts of money. It is now issuing new shares of stock. It is burning up increasing amounts of free cash and is missing and lowering guidance on its revenue. They do have a decent balance sheet and a reasonable chart. But that simply isn't enough for me to include a stock on my list.

I do believe that the revenue growth was impressive year over year. And I like the potential for carbon fiber. But it isn't how I pick stocks.

Thanks again for writing and inquiring. ZOLT might turn out to be a TERRIFI investment, and I may have just panned the best stock for 2007. I can live with that possibility. I am just honing my own investing philosophy. Not to make a killing, but just to consistently make money.

See you next month at Stock Club where we can discuss this one further! If you or anyone else have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. If you get a chance, be sure and visit my Stock Picks Podcast Website! Have a great week investing everyone!

Bob

Thursday, 14 December 2006

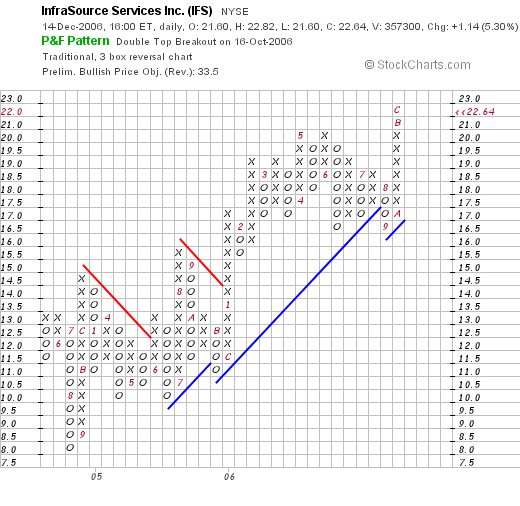

InfraSource Services Inc (IFS)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decision based on information on this website.

It is getting rather late and I intend to be up early walking, so let me try, if I can, be as brief as possible about this stock. I was looking through the top % gainers list this afternoon, looking to see if I could come up with a new name. I have been revisiting lots of my past picks and I wanted to try to find some name I hadn't looked at previously, yet a stock that met the criteria that I set up for my blog. I believe I found one with Infrasourc (IFS). Let's briefly look at this stock and I will try to tell you why!

First of all, Infrasource (IFS) closed at $22.64, up $1.14 or 5.30% on the day. That was enough, even in today's strong market, to make the top % gainers list on the NYSE. I do not own any shares of IFS nor do I have any options.

First of all, Infrasource (IFS) closed at $22.64, up $1.14 or 5.30% on the day. That was enough, even in today's strong market, to make the top % gainers list on the NYSE. I do not own any shares of IFS nor do I have any options.

According to the Yahoo "Profile" on the stock, the company "...operates as a specialty contractor in the United States. It operates in two segments, Infrastructure Construction Services and Telecommunication Services. The Infrastructure Construction Services segment provides design, engineering, procurement, construction, testing, and maintenance services for utility infrastructure. The company offers its services to electric power utilities, natural gas utilities, telecommunication customers, and government entities, as well as heavy industrial companies, such as petrochemical, processing, and refining businesses."

I couldn't find any particular news to explain today's move.

On November 1, 2006, IFS reported their 3rd quarter 2006 results. Revenue for the quarter ended September 30, 2006, came in at $275.9 million, up 22% from the $226.6 million reported in the same period last year. Net income was $10.8 million or $.27/diluted share, up sharply from the $6.6 million or $.16/diluted share reported in the same quarter in 2005. They beat expectations as analysts had expected a profit of $.23/share on revenue of $270 million, 'according to a poll by Thomson Financial.'

For a longer-term view, we can review the Morningstar.com "5-Yr Restated" financials for IFS, which shows that from 2001 to 2003, revenue actually declined sharply from $609 million to $135 million, however, this turned around in 2004 and by 2005, revenue came in at $866 million with $977 million reported in the trailing twelve months (TTM).

Earnings were $.34/share in 2005 and $.60/share in the TTM.

Morningstar shows 39 million shares in 2005 and 40 million in the TTM.

Free cash flow which was $(3) million in 2004, $(11) million in 2005, turned positive at $61 million in the TTM.

The balance sheet appears solid with $15.8 million in cash and $275.3 million in other current assets, which easily covers both the $165.1 million in current liabilities and the $95.9 million in long-term liabilities combined. The 'current ratio' works out to be just under 2.

Checking Yahoo "Key Statistics" on IFS, we can see that this is a mid-cap stock with a market capitalization of $906.69 million. The trailing p/e is a bit rich at 37.18 and the forward p/e (fye 31-Dec-07) is estimated at 25.44. However, the '5 yr expected' PEG also is a bit rich at 2.41.

Yahoo reports 40.05 million shares outstanding with 25.57 million that float. As of 11/10/06, there were 1.15 million shares out short, working out to 3% of the float or 4.4 trading days of volume. No dividend is paid and no stock splits are reported.

Looking at the "point and figure" chart on InfraSource from StockCharts.com, we can see a very nice graph going back to May, 2004, when the stock bottomed at $8.00. Since then, the stock has moved steadily higher and is currently pushing into new highs in the $22 range. At least for the last two or so years, the chart looks strong.

To summarize, this is a mid-cap stock that moved higher today. They had a great recent quarter and the company has been growing strongly the past few years turning itself around from a poor financial performance to strong results. Earnings have been growing nicely, the company beat expectations on its latest quarterly report, they have turned from negative cash flow to strongly positive free cash flow and the balance sheet looks nice.

This is an interesting company to consider. If I were in the market to be buying stocks today, this is the kind of stock I would be buying. Of course, I am waiting for my own "buy signal" that would be generated by a partial sale of one of my existing holdings at a targeted gain....and I don't have that yet. Meanwhile, I shall be adding this to my "vocabulary" and shall be ready to pick it up should it be on the top % gainers list again and I have 'permission' to buy!

Thanks again for stopping by. This was a bit abbreviated, but I wanted to get it recorded as I think it deserves attention. Have a great weekend!

Bob

Posted by bobsadviceforstocks at 11:42 PM CST

|

Post Comment |

Permalink

Updated: Thursday, 14 December 2006 11:43 PM CST

Tuesday, 12 December 2006

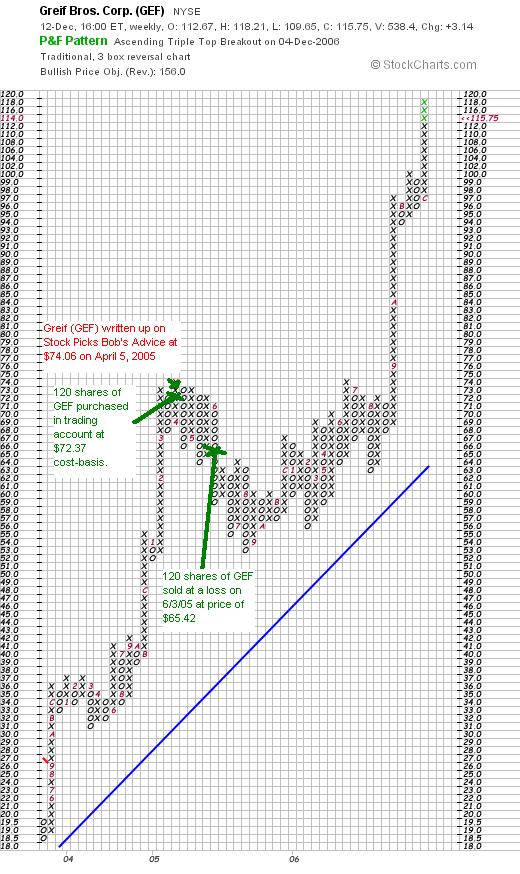

Greif (GEF) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I was looking through the list of top % gainers on the NYSE and saw an "old favorite" of mine Greif (GEF) on the list. GEF closed at $115.75, up $6.01 or 5.48% on the day. I do not currently own any shares or options on this stock. I did own some shares for a few months, took my (8)% loss or so, and sold my shares. That is another story!

I was looking through the list of top % gainers on the NYSE and saw an "old favorite" of mine Greif (GEF) on the list. GEF closed at $115.75, up $6.01 or 5.48% on the day. I do not currently own any shares or options on this stock. I did own some shares for a few months, took my (8)% loss or so, and sold my shares. That is another story!

I first wrote up Greif on April 5, 2005, on Stock Picks Bob's Advice when the stock was trading at $74.06. With today's close at $115.75, this represents a gain of $41.69 or 56.3% since posting about a year-and-a-half ago! Usually I bemoan the fact that 'only if I had purchased some shares...etc.'. In this particular case, I did purchase some shares.

I first wrote up Greif on April 5, 2005, on Stock Picks Bob's Advice when the stock was trading at $74.06. With today's close at $115.75, this represents a gain of $41.69 or 56.3% since posting about a year-and-a-half ago! Usually I bemoan the fact that 'only if I had purchased some shares...etc.'. In this particular case, I did purchase some shares.

In fact I did purchase 120 shares for my trading account on April 4, 2005, at a cost basis of $72.34. Unfortunately, this was a case of very bad timing, as the stock declined rather steadily to $65.42 where I sold my shares on June 3, 2005. I had taken a loss of $(6.92)/share or (9.2)%, and using my (8)% loss limit, out the shares went. Most of the time, these sales have worked well for me. But in this case, my stock picked rebounded and moved sharply higher without me :(. This only shows the limitations of any trading strategy. Overall, I am quite content with my disciplined approach, but there are times like this that I look back....well you know the feeling!

Anyhow, let me show you why I think that Greif still deserves a spot on the blog!

First of all, what does the company do?

According to the Yahoo "Profile" on Greif (GEF), the company

"...and its subsidiaries engage in the manufacture and sale of industrial packaging products, and containerboard and corrugated products worldwide. The company operates in three segments: Industrial Packaging and Services; Paper, Packaging, and Services; and Timber."

Was there any news to explain today's price jump?

Greif (GEF) is still apparently moving higher from the effect of last week's earnings report.

What was the latest earnings report?

On December 6, 2006, Greif reported 4th quarter 2006 results. For the quarter ended October 31, 2006, net sales climbed 195 to $735.6 million from $619.7 million in the fourth quarter of 2005. For the quarter, GEF reported GAAP net income of $41.7 million or $1.41 per diluted Class A share, vs. $22.0 million or $.75/diluted class A share in the same quarter in 2005.

How about longer-term?

Reviewing the Morningstar.com "5-yr Restated" financials on Greif, we can see the steady increase in revenue from $1.5 billion in 2001 to $2.4 billion in 2005 and $2.5 billion in the trailing twelve months.

Earnings, however, do not show the same steady rise. In fact, earnings dropped from $3.14/share in 2001 to a low of $.34/share in 2003 before turning sharply around to $1.66/share in 2004, $3.56/share in 2005 and $4.17/share in the TTM.

The company does pay a dividend and has been increasing it, with $.54/share paid in 2001, increasing to $.56/share in 2002, $.60/share in 2004, $.80/share in 2005 and $1.08/share in the TTM.

Nicely, the company shows 28 million shares outstanding in 2001, and has decreased this to 23 million in the TTM.

Free cash flow has been strongly positive with $34 million in 2003, increasing to $103 million in 2005 and $128 million in the TTM.

The balance sheet, as reported by Morningstar, looks adequate with $167.7 million in cash and $577.5 million in other current assets. This combined $745.2 million in current assets, when compared against the $447.6 million in current liabilities yields a strong current ratio of 1.66. The company does have an additional $786.6 million in long-term debt, but with the solid free cash flow, this doesn't appear to be much of a problem.

What about some valuation numbers?

Reviewing Yahoo "Key Statistics" on GEF, we can see that this company is a mid cap stock with a market capitalization of $2.68 billion. The trailing p/e is a moderate 27.91, but the forward p/e (fye 31-Oct-07) is estimated at a much more reasonable 17.46. With the rapid growth in earnings anticipated, the '5 yr expected' PEG is reported at a very nice 1.13.

The Fidelity.com eresearch website suggests that valuation is also reasonable with a Price/Sales (TTM) ratio of .96, with an industry average of .95, the company is sitting at the 69th percentile of its industrial group.

Besides being a 'good value' by the above measure, Fidelity also suggests it is one of the more profitable firms in its industrial group with a Return on Equity (ROE) (TTM) of 17.95%, compared to an industry average of 10.27%. This puts GEF at the 70th percentile of its group.

Returning to Yahoo, we find that there are only 23.11 million shares outstanding with 14.02 million that float. Pertinently, as of 11/10/06, there were 720,030 shares out short, which with an average trading volume of only 97,229 shares, works out to a 'short ratio' of 8 trading days. With my own peculiar 3 day rule for significance, we may well be witnessing some pressure on the short-sellers who may be feeling a bit of a squeeze as they scramble to buy shares to cover their previously sold shares in light of the sharp rise of the stock price on good news. That is just a hunch, but it probably has a bullish effect on the stock price currently.

As I noted above, the company is paying a dividend with the forward dividend rate being $1.44/share with a yield of 1.30%. No stock splits are reported on Yahoo.

What does the chart look like?

Simply Gorgeous! Take a look at the "point and figure" chart on Greif (GEF) from StockCharts.com. The weekly chart shows the stock trading as low as $18.50 in May, 2003, only to climb quickly to $74 in April, 2005, (unfortunately exactly where I entered the stock). The stock had a small "shake-out" of investors (including me!) to a level of $54 in August, 2005. The stock has been steadily increasing since to its current level of about $118.

Summary: What do I think?

Certainly, the company made a nice move the last few days. The earnings report appears solid. The Morningstar.com report also looks nice with steady revenue growth, and after turning-around the earnings results, steady earnings growth the past few years as well. The company even pays a nice dividend and has been growing that as well. In fact, the company has been buying back shares and has fewer shares than a few years ago!

Valuation-wise, the stock price, although much higher than six months ago, still appears reasonably valued, with an average Price/Sales, a high Return on Equity, a PEG just over 1.1, and a forward p/e in the teens. There are even a lot of short-sellers, who likely feel the current rise is unsustainable. But until the eventual pull-back, they are feeling the heat and likely adding to the upward price pressure.

Only if I also hadn't been shaken out :(. Anyhow, it still is an interesting stock and deserves your awareness even if it doesn't have my own ownership!

Thanks again for stopping by! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. If you get a chance, drop by and visit my Stock Picks Podcast Website where I discuss many of the same stocks and issues that I cover here on the blog. Have a great week investing!

Bob

Monday, 11 December 2006

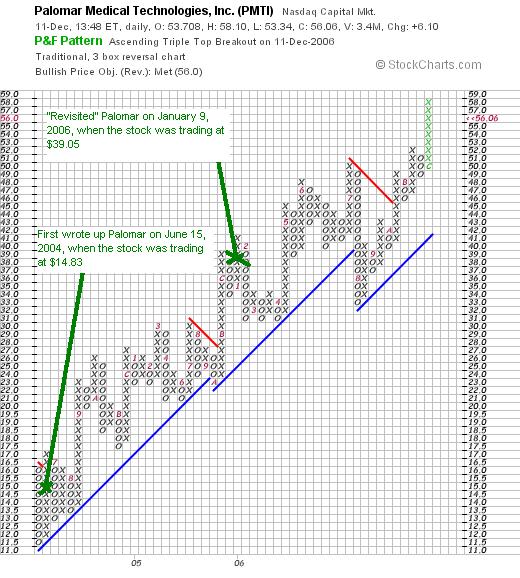

Palomar Medical Technologies (PMTI) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I was looking through the list of top % gainers on the NASDAQ and came across an old favorite of mine, Palomar Medical Technologies, which, as I write, is trading at $55.67, up $5.61 or 11.23% on the day. I do not currently own any shares nor do I have any options on this stock.

I was looking through the list of top % gainers on the NASDAQ and came across an old favorite of mine, Palomar Medical Technologies, which, as I write, is trading at $55.67, up $5.61 or 11.23% on the day. I do not currently own any shares nor do I have any options on this stock.

I first wrote up Palomar on Stock Picks Bob's Advice on June 15, 2004, when Palomar was trading at $14.83. With today's price of $55.67, this represents an appreciation of $40.84 or 275.4% since posting. On January 9, 2006, I "revisited" this stock when it was trading at $39.05. Since that time, less than a year ago, this stock has appreciated another $16.62 or 42.6%!

Let's take another quick look at this stock and see if it still deserves a spot on the blog!

What does this company do?

What does this company do?

According to the Yahoo "Profile" on Palomar, the company

"...engages in the research, development, manufacture, marketing, sale, and distribution of light-based products for medical and cosmetic treatments. It offers products for hair removal; non invasive treatment of facial, leg veins, and other benign vascular lesions, such as rosacea, spider veins, port wine stains, and hemangiomas; removal of benign pigmented lesions, such as age and sun spots; tattoo removal; acne treatment; wrinkle removal; Pseudofolliculitis Barbae or PFB treatment; treatment of red pigmentation in hypertrophic and keloid scars; treatment of verrucae, skin tags, and seborrheic keratosis; deep tissue heating for relief of muscle and joint pain; and other skin treatments."

Was there any news to explain today's move?

According to a news story, the company received FDA approval to market an over-the-counter device for hair removal for home use. Apparently, with this approval, it is anticipated that this will greatly expand the potential sales of Palomar's products.

How did they do in the latest quarterly report?

On October 26, 2006, Palomar (PMTI) reported 3rd quarter 2006 financial results. Revenue for the quarter ended September 30, 2006, came in at $28 million, up over 40% from $19.3 million in the third quarter of 2005. Net income came in at $8.4 million or $.41/share, up sharply as well from the $4.6 million or $.24/diluted share the prior year.

And longer-term results?

Reviewing the Morningstar.com "5-Yr Restated" financials for PMTI, we can see a very pretty picture of strongly growing revenue, with $17 million in 2001, increasing to $76.2 million in 2005 and $109 million in the trailing twelve months (TTM).

Earnings, which were at a negative $(.54)/share in 2001, improved to break-even in 2002 then up to $.91/share in 2005 and $1.86 in the TTM.

The company has been increasing its shares outstanding from 10 million shares in 2001 to 18 million in the TTM. This 80% increase in shares has been accompanied by a more than 300% increase in both revenue in earnings, so it hasn't been a big problem for stockholders from my perspective.

Free cash flow has also been improving nicely with $1 million in 2003, growing to $11 million in 2004, $20 million in 2005, and $34 million in the TTM.

Per Morningstar.com, the balance sheet is pristine with $81.2 million in cash and $28.4 million in other current assets. This $109.6 million in current assets, when compared to the $20.4 million in current liabilities yields a current ratio over 5! The company has no long-term liabilities reported!

What about some valuation numbers?

According to the information on Yahoo "Key Statistics" on PMTI, the company is a mid cap stock with a market capitalization of $988.42 million. The trailing p/e is a tad rich at 29.83, and peculiarly (is this an old estimate?) the forward p/e (fye 31-Dec-07) is estimated at 32.44. In any case, analysts are not expecting the company to actually be shrinking its earnings as the "5 yr expected" PEG is reported at 0.73, making the p/e seem quite reasonable considering the expected growth in earnings.

Looking at the Fidelity.com eresearch website, we find that the Price/Sales (TTM) works out to 8.00, with an industry average of 30.83. This still puts it at the 87th percentile in its industry. The company is quite profitable with a Return on Equity (ROE) (TTM) of 53.06% compared to an industry average of 33.01%, putting it at the 91st percentile in this regard in its group.

Finishing up with Yahoo, we find that there are 17.68 million shares outstanding with 16.56 million that float. Of those that float, 31.90% are out short (!) representing 5.28 million shares or 11.6 trading days of volume. Using my "3 day rule" of short interest, this appears quite significant. And indeed, with today's announcement, we may have found the short-sellers scrambling to cover their bets against the company and maybe, they are finding that shares are tough to locate to buy! In any case, the sharp rise in stock price may well put additional pressure on the remaining shorts.

The company does not pay a dividend. The last stock split reported on Yahoo was a reverse 1:7 stock split back in May, 1999.

What about the Chart?

Taking a look at the "Point and Figure" chart on PMTI from StockCharts.com, we can see a gorgeous graph with a steady appreciation in stock price from $11.50, in June, 2004, to its current level around $58. There is no appreciable weakness, and in fact, the rate of the rise, does not appear to make the stock appear technically 'over-extended' imho. I have written in my stock pick prices and dates on the chart for your review as well!

Summary: What do I think?

Well I wish I had mortgaged my house and borrowed from my credit cards and every relative I had to buy shares when I first wrote up this stock! Anyhow, the stock made a nice move on what may well be quite significant news of an over-the-counter sale of its appliances. The latest quarter was beautiful, the Morningstar.com report is gorgeous, and the balance-sheet is amazing! (Am I in love or what?) The chart looks great and valuation appears reasonable with a PEG under 1.0 and a Return on Equity near the top of its group. This is the kind of stock I would be buying today if I had permission as I call it. Meanwhile, I shall be keeping it in my "vocabulary" of investable stocks!

Thanks so much for visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, please feel free to visit my Stock Picks Podcast Website, where I talk about many of the same stocks I write about on the blog!

Have a great week investing everyone!

Bob

Saturday, 9 December 2006

Coach (COH) "Weekend Trading Portfolio Analysis"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

Thank goodness for weekends! They give us all a chance to unwind a little and catch up with the things we put off all week long. Lord knows I have a huge list of things I need to be doing! On this blog, I have used the weekend to basically provide two types of discussions. First of all, I like to look back about a year (I am thinking of looking back three years now that I have had the blog up over that long!), and also review my actual holdings in my own trading portfolio.

I believe that both of these reviews are helpful. One, a theoretical look at stocks discussed here, and the second, a real review of my actual holdings in my own trading account. I do have other investments in managed accounts and also manage a couple of small accounts for my children. Whenever I discuss stocks I try very hard to remember to let you know whether I own any stocks or if any accounts that I have control over own those equities. I also have some retirement accounts that are managed independently of my own input. I do not always know or remember what stocks are owned in those accounts.

Currently, I own 11 stocks in my Trading Account. If you can recall my discussions elsewhere, I will own anywhere from 6 stocks (my minimum number) to 25 stocks (my maximum). I use the actual performance of my own holdings to determine whether I should be adding new positions (in the event of a partial sale on good news) or sitting on my hands, so to speak, in the even of a sale of a holding on bad news or poor stock price performance. I have been using this system for several years as my own trading barometer for investing.

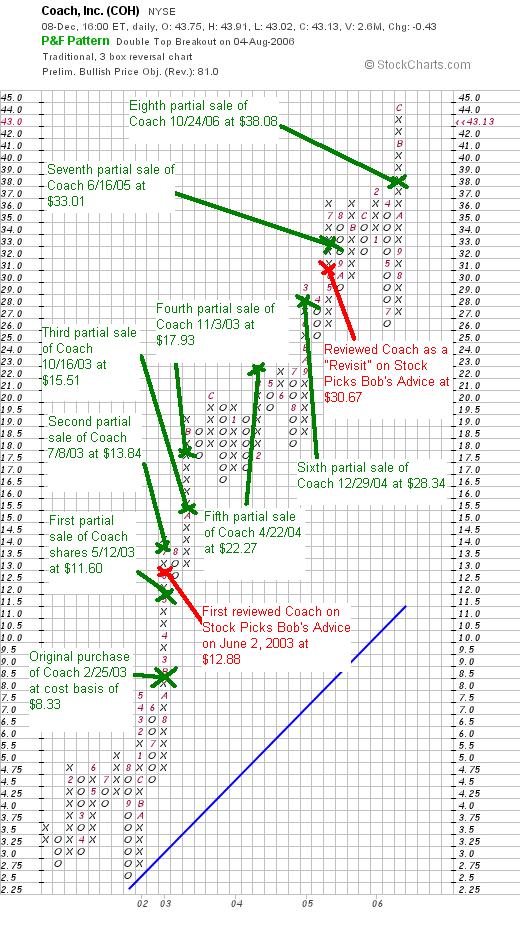

About every two weeks, I have been trying to review one of my holdings, which would work to about once every 6 months with the current size of the portfolio. Two weeks ago, on November 25, 2006, I reviewed my holding of Wolverine Worldwide. Going alphabetically, I am back to the start of my list, and would like to share with you my most successful investment story of my portfolio, my purchase of Coach (COH).

Currently in my trading portfolio, I own 85 shares of Coach (COH) which were purchased February 25, 2003, at a cost basis of $8.33. COH closed at $43.13 on December 8, 2006, for an unrealized gain of $34.80 or 417% since my purchase.

Currently in my trading portfolio, I own 85 shares of Coach (COH) which were purchased February 25, 2003, at a cost basis of $8.33. COH closed at $43.13 on December 8, 2006, for an unrealized gain of $34.80 or 417% since my purchase.

I first discussed Coach on Stock Picks Bob's Advice only three weeks after I started the blog when the stock was trading at $51.53 on June 2, 2003. Adjusted for two subsequent 2:1 stock splits this works out to a "pick price" of $12.88. I "revisited" Coach on June 1, 2005 on Stock Picks when the stock was trading at $30.67.

As is my strategy with all of my purchases, I try to sell portions of my holdings, currently 1/6th of remaining shares at targeted appreciation points. I use appreciation levels of 30, 60, 90, and 120%, then 180, 240, 300, and 360%, (then by 90% intervals): 450, 540, 630, and 720% appreciation levels. I plan on continuing to increase intervals by 30% each group of four sales if I ever get there :). In any case, I have now sold portions of my Coach holding eight times! (Please review the chart below for details.)

With eight sales, when would my next sale happen? Having sold at 30, 60, 90, 120, 180, 240, 300, and 360%, my next sale would be at a gain of 450%, or calculated, works out to 5.50 x $8.33 = $45.82. At that point, I would be selling 1/6th of my 85 shares or 14 shares. On the downside, half of the top sale would be at a 180% gain or 2.80 x $8.33 = $23.32. If Coach declines to that level, I plan on selling all of my shares. With all of my partial sales have extracted my purchase price and more, I shall try to exercise the appropriate discipline and let the stock price determine my trading action!

Let's take another look at this stock and see if it still deserves a spot on this blog.

What does the company do?

According to the Yahoo "Profile" on Coach, the company

"...engages in the design and marketing of handbags and accessories in North America and internationally. Its primary product offerings include handbags; women’s and men’s accessories, such as money pieces, wristlets, cosmetic cases, key fobs, belts, electronic accessories, wallets, and other leather accessories; outerwear, gloves, hats, and scarves; men’s computer bags, messenger-style bags, and totes; and luggage and travel accessories. The company’s product offerings also comprise watches, footwear, and eyewear. Its products are sold through direct-to-consumer channels, including company-operated retail and factory stores in North America and Japan; and its online store and catalogs."

How did they do in the latest quarter?

On October 24, 2006, COH reported 1st quarter 2007 results. Net sales came in at $554 million, up from $449 million in the same quarter last year. Net income grew 34% to $126 million or $.34/share, up from $94 million or $.24/share. Analysts had been expecting $.31/share, and the company actually exceeded its own guidance of $.30/share. Comparable store sales in the United States grew at 21.4% inthe quarter. Comparable store sales in Japan grew at a "mid-single-digit" rate for the quarter. The company also raised guidance for the upcoming quarter to $.56 shares ahead of analysts' expectations of $.55. For fiscal year 2007, the company raised guidance to sales of $2.55 billion, and earnings per diluted share of at least $1.63. This is ahead of the analysts who apparently have been expecting $1.58 for 2007.

This really was a terrific report with solid same store sales reported, beating expectations AND raising guidance. This is what I would generally refer to as a "trifecta-plus"!

What about longer-term results?

If we look at the Morningstar.com "5-Yr Restated" financials on Coach, you can see a BEAUTIFUL picture which I believe explains the phenomenal performance of this stock. Revenue growth works out to $719 million in 2002, increasing steadily to $2.11 billion in 2006 and $2.22 billion in the trailing twelve months (TTM). Earnings have also steadily increased, and dramatically at that, from $.21/share in 2002 to $1.27/share in 2006 and $1.37/share in the TTM. No dividends are paid. The number of shares outstanding has been quite stable at 360 million in 2002 to 380 million in 2006. The company has been apparently buying back shares as Morningstar reports 367 million shares for the TTM.

Free cash flow has been positive and increasing with $286 million in 2004, increasing to $381 million in 2005, $463 million in 2006 and $474 million in the TTM.

The balance sheet, like the rest of the numbers on Coach from this page is also gorgeous. They have $456.3 million in cash and $567.1 million in other current assets. This is a total of $1023.4 million, which when compared to the current liabilities of $394.9 million yields a current ratio of 2.59. The long-term liabilities are a very modest $89.4 million per Morningstar.

What about some valuation numbers?

Looking at Yahoo "Key Statistics" we can see that this is a large cap stock with a market capitalization of $15.85 billion. The trailing p/e is a bit rich at 31.50, but the forward p/e (fye 01-Jul-08) is estimated at a much nicer 21.57. In fact, with the rapid growth in earnings, the PEG still comes in at a reasonable 1.19.

Reviewing the information from the Fidelity.com eresearch website, we find that the Price/Sales for Coach is indeed rich at 7.39 for the TTM, with an industry average of 2.59, placing Coach at the 97th percentile for "richness" in Price/Sales ratio.

Perhaps pertinently, in terms of profitability, Coach is very profitable with a return on equity (ROE) coming in at 40.05% with an industry average of 20.77%. This puts Coach at the 94th percentile for profitability.

Returning to Yahoo, we find that there are 367.48 million shares outstanding with 361.23 million that float. Currently there are 6.49 million shares out short, representing 1.8% of the float or a short ratio of 1.8 trading days. Not too many short-sellers appear willing to speculate against this company!

No dividend is paid, and as noted earlier, the last stock split was a 2:1 split on April 5, 2005.

What about the Chart?

Looking above, we can see the unbelievable strength in this stock ever since it corrected back in September, 2001, when the stock dipped to a split-adjusted price of $2.50/share. Since then the stock has been charging ahead without much of any sign of a correction. In fact, if anything, the stock is overextended, way above the support levels. However, as long as good news is not in short supply, there is no sign that the stock will be pulling back to lower levels imho.

Summary: What do I think?

In a word, this stock has been AMAZING. I believe this stock, and this company, represent the archetypical firm I am looking for. Aren't all of us looking for stocks like this? They have grown their revenue, their earnings, beat expectations and repeatedly raised guidance. WOW. Unfortunately, early on, I was selling 1/4 positions of my holdings and the size of my holding dropped a bit, but overall, I am pleased with my sales which have allowed me to grow my portfolio with other positions.

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. If you get a chance, drop by and visit my Stock Picks Podcast Site. Have a great rest of the weekend!

Bob

"Looking Back One Year" A review of stock picks from the week of August 8, 2005

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

One of the things I try to do around here is to continue to examine past stock "picks" and selections and see how they turned out. There isn't anything magic about my selection process. These analyses assume a "buy and hold" strategy to investments. In practice I employ, and advocate, a disciplined portfolio management strategy that requires sales of stocks that decline to pre-determined levels as well as partial sales of stocks as they appreciate and reach pre-determined price targets. My goal is always to avoid large losses and preserve large gains as much as possible.

To help us get a better handle on what happened after stocks have been selected, I am starting to post "point & figure" charts from StockCharts.com with these reviews to let you see what I did and when and what happened later. I hope that you find these charts helpful!

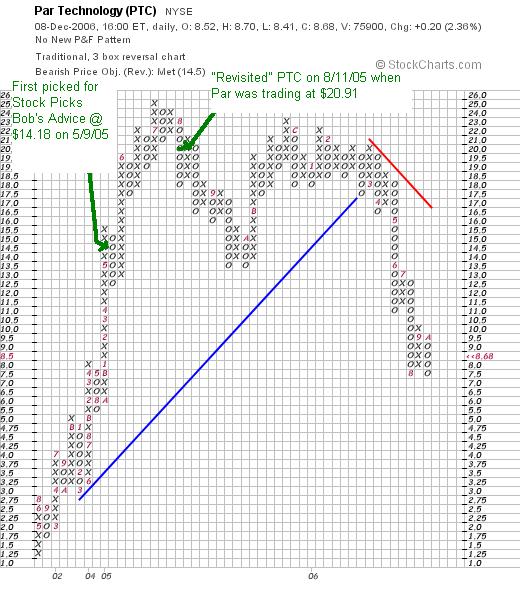

On August 11, 2005, I "revisited" Par Technology (PTC) on Stock Picks Bob's Advice when the stock was trading at $31.36. This was a repeat post for Par which was first reviewed on this blog on May 9, 2005, when it was trading at $22.17. Par had a 3:2 stock split on January 9, 2006, making my August, 2005, stock pick price effectively $20.91 (and my May, 2005 "pick" effectively $14.78). Par closed at $8.68 on December 8, 2006, giving my August selection a loss of $(12.23) or (58.5)%. (This particular pick shows the potential of loss of any and all stocks selected on this blog!)

On August 11, 2005, I "revisited" Par Technology (PTC) on Stock Picks Bob's Advice when the stock was trading at $31.36. This was a repeat post for Par which was first reviewed on this blog on May 9, 2005, when it was trading at $22.17. Par had a 3:2 stock split on January 9, 2006, making my August, 2005, stock pick price effectively $20.91 (and my May, 2005 "pick" effectively $14.78). Par closed at $8.68 on December 8, 2006, giving my August selection a loss of $(12.23) or (58.5)%. (This particular pick shows the potential of loss of any and all stocks selected on this blog!)

Looking at the stock chart below, we can see how the chart appeared to break down in March, 2006, when the stock price broke through apparent support at the $17 level.

On October 26, 2006, Par (PTC) reported 3rd quarter 2006 results. For the quarter ended September 30, 2006, the company reported revenues of $48.5 million down 7% from revenues of $52.2 million in the same quarter in 2005. Net income came in at $550,000, down over 75% from the $2.5 million reported the same quarter last year. Similarly, diluted earnings per share came in at $.04 during the quarter, down sharply from $.17/share last year.

On October 26, 2006, Par (PTC) reported 3rd quarter 2006 results. For the quarter ended September 30, 2006, the company reported revenues of $48.5 million down 7% from revenues of $52.2 million in the same quarter in 2005. Net income came in at $550,000, down over 75% from the $2.5 million reported the same quarter last year. Similarly, diluted earnings per share came in at $.04 during the quarter, down sharply from $.17/share last year.

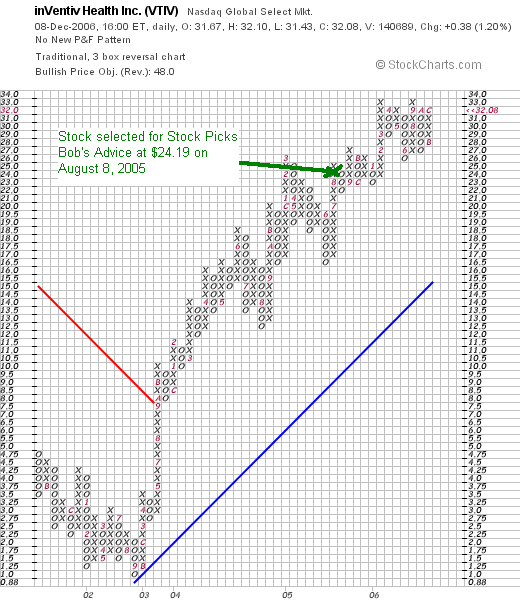

On August 8, 2005, I posted Ventiv Health (VTIV) (which subsequently in June, 2006, changed its name to inVentiv Health (VTIV)) at a price of $24.19. VTIV closed at $32.08 on December 8, 2006, for a gain of $7.89 or 32.6% since posting.

On August 8, 2005, I posted Ventiv Health (VTIV) (which subsequently in June, 2006, changed its name to inVentiv Health (VTIV)) at a price of $24.19. VTIV closed at $32.08 on December 8, 2006, for a gain of $7.89 or 32.6% since posting.

On November 7, 2006, inVentiv (VTIV) reported 3rd quarter 2006 results. Total revenues increased 54% to $197.8 million in the quarter compared with $128.4 million in the same quarter in 2005. While GAAP earnings actually declined to $.34/share from $.53/share, $.24/share in 2005 were for a $6.7 million tax benefit which would have worked out to $.30/share in 2005. Since I generally go with GAAP earnings without looking at all of the one-time items, etc., I gave this stock a 'thumbs-down', but looking harder at the numbers produces a more-encouraging picture and the "street" was not bothered by this report.

In addition, in another bullish note the company raised guidance for 2006 from $705-$725 million to $735-$745 million and adjusted earnings per share guidance for 2006 from $1.46-$1.48 to $1.46-$1.50. They also provided initial revenue guidance for 2007 of $830-$850 million, and initial 2007 eps guidance of $1.70 to $1.80.

All-in-all, a much nicer picture at VTIV than PTC!

So how did I do with these two stock picks? Well, due to the large decline in the PTC stock, the average performance of these two picks works out to a loss of (13.0)%. This emphasizes the importance of limiting losses to small amounts and allowing gains to grow! As I noted above, my "performance" on these reviews is always a "buy and hold" strategy that is not what I actually advocate or practice.

Thanks so much for stopping by and visiting! I hope you enjoyed my inclusion of stock charts noting my own "calls" on the stocks! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. If you get a chance, stop by and visit my Stock Picks Podcast Site, where I discuss many of the same stocks and strategies that I write about here on the blog.

Bob

"Looking Back One Year" A review of stock picks from the week of August 1, 2005

Hello Friends! Thanks so much for visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

Usually I am doing a review in this space. However, on this particular week, as occasionally is the case, I did not review or pick any stocks to discuss. Thus, I shall not be "looking back" at that week, but shall, if I get a chance, advance to the following week, as I am a bit behind :) in this year ago review process as has been pointed out to me :) several times!

Thanks so much for stopping by! If you have any questions or comments, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Bob

Friday, 8 December 2006

Bolt Technology (BTJ) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I was looking through the list of top % gainers on the AMEX today and came across an old 'favorite' of mine, Bolt Technology (BTJ), which I first reviewed on Stock Picks Bob's Advice on January 19, 2006, when the stock was trading at $17.86. As I write, Bolt is trading at $22.81, up $1.60 or 7.54% on the day. The stock is currently higher by $4.95 or 27.7% since I posted the stock here a little under a year ago. I do not own any shares of Bolt nor do I own any options on the stock.

What does this company do?

According to the Yahoo "Profile" on Bolt, the company

"...through its subsidiaries, engages in the development, manufacture, and sale of seismic energy sources used in the seismic exploration for oil and gas worldwide. The company operates in two segments, Geophysical Equipment and Industrial Products. The Geophysical Equipment segment offers marine seismic energy sources and underwater electrical connectors and cables, seismic source monitoring systems, air gun signature hydrophones, and pressure transducers used by the marine seismic industry. The company’s Industrial Products segment offers miniature industrial clutches, brakes, and sub-fractional horsepower electric motors."

"...through its subsidiaries, engages in the development, manufacture, and sale of seismic energy sources used in the seismic exploration for oil and gas worldwide. The company operates in two segments, Geophysical Equipment and Industrial Products. The Geophysical Equipment segment offers marine seismic energy sources and underwater electrical connectors and cables, seismic source monitoring systems, air gun signature hydrophones, and pressure transducers used by the marine seismic industry. The company’s Industrial Products segment offers miniature industrial clutches, brakes, and sub-fractional horsepower electric motors."

How did they do in the latest quarter?

On October 24, 2006, BTJ announced 1st quarter fiscal 2007 results. Sales for the quarter ended September 30, 2006, climbed 25% to $10.0 million, up from $8.0 million in the same period last year. Net income grew 96% to $2.0 million or $.35/share, up from $1.02 million or $.18/share in the year earlier same period.

What about longer-term results?

Reviewing the Morningstar.com "5-Yr Restated" financials, we can see that the company did have a drop in revenue from $18 million in 2002 to $11 million in 2003. However, since then Bolt has been growing its revenue steadily to $19 million in 2005 and $33 million in 2006. Similarly, earnings dropped from $.35/share in 2002 to a loss of $(.03)/share in 2003. However, the company was once again profitable in 2004 at $.16/share, and has grown earnings strongly since with $.30/share reported in 2005 and $.86/share in 2006. The number of shares outstanding has been fairly stable (and small) with 5 million in 2002, 5 million in 2006, and 6 million in the trailing twelve months (TTM). No dividend is reported.

Free cash flow, while small, has been positive at $1 million in 2004 and $1 million in the TTM.

The balance sheet looks solid to me with $4.6 million in cash and $16.3 million in other current assets, giving us a total of $20.9 million in current assets, which easily covers botht the $5.8 million in current liabilities and the small $.4 million in long-term debt. Dividing this out yields a current ratio of 3.6.

What about some valuation numbers?

Reviewing Yahoo "Key Statistics" on Bolt (BTJ) we see that this is a small "small cap" company with a market capitalization of only $125.38 million. The trailing p/e is a reasonable (imho) 21.74. No PEG is reported, but if the current growth in earnings were to continue, the PEG would certainly be well under 1.0.

Checking the Fidelity.com eresearch website, we can see that the Price/Sales (TTM) ratio works out to 3.39 with an industry average of 3.42. The Return on Equity (ROE) is reported at 21.15%, slightly below the industry average of 29.93% per Fidelity.

Finishing up with Yahoo, we can see that there are only 5.59 million shares outstanding and 5.13 million that float. As of 11/10/06, there were only 54,890 shares out short, representing 1.10% of the float or 0.5 trading days of volume....not a very significant short interest at all.

As noted, no stock dividends are reported, and Yahoo does not report any stock splits either.

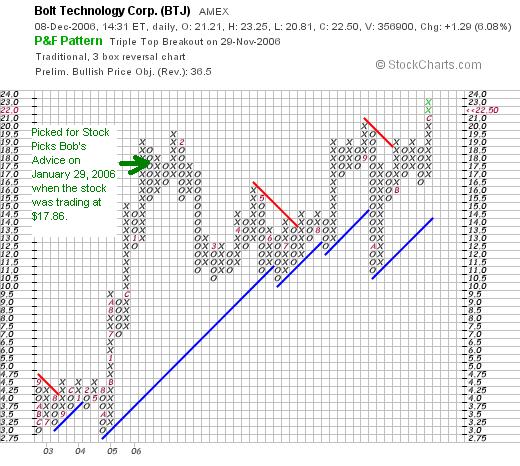

What about the chart?

If we look at a "Point & Figure" chart from Stockcharts.com on BTJ, we can see that the stock, which was trading around $2.75 to $4.50 between much of 2002 to 2004, moved sharply higher late in 2004 and into early 2006 to the $19.00 range. More recently, the stock once again appears to be moving higher into new territory. The chart looks interesting to me!

Summary: What do I think about the stock?

Well, if I didn't like it I wouldn't be writing it up again :). Seriously, the stock looks interesting. It is a tiny company that is dependent on the oil service industry but unless the entire oil market collapses, it appears this company may well be a good performer. Valuation isn't bad, and the Morningstar.com report is attractive. If I were in the market to be buying a stock, this is the kind of stock I would be buying today!

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, when you get a chance, drop by and visit my Stock Picks Podcast Site, where I discuss many of the same stocks I have written about on the blog.

Bob

Newer | Latest | Older