Stock Picks Bob's Advice

Saturday, 28 August 2010

Colgate-Palmolive (CL)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I wrote in the previous entry how my shares of McDonald's (MCD) had appreciated 30% since my purchase triggering a partial sale and a 'trading signal' to add a new holding to my own portfolio. I did this and purchased shares of Colgate-Palmolive (CL). Just catching up with this purchase, I wanted to share with you a few thoughts about this company.

I wrote in the previous entry how my shares of McDonald's (MCD) had appreciated 30% since my purchase triggering a partial sale and a 'trading signal' to add a new holding to my own portfolio. I did this and purchased shares of Colgate-Palmolive (CL). Just catching up with this purchase, I wanted to share with you a few thoughts about this company.

Probably like you I am uncertain about the health of our economy over the intermediate term. I tend to agree with Paul Krugman that the economic stimulus advanced by the Obama administration wasn't big enough. I am also concerned about our level of debt and the size of government but my own basic Economics education has convinced me that Keynes was right 'enough' that austerity right now is absolutely the wrong time to be cutting back.

I think the bail-out of GM, the TARP funds, the financial re-regulation is all medicine indicated for the illness this patient is facing. It disappoints me that in this difficult time of high unemployment, increasing disparity of wealth, and global financial stress that our Republicans in office do not give the newly elected President a chance and instead obstruct at every turn.

OK enough politics. Many of you who are my friends probably know that I love politics almost as much as I enjoy investing!

Let's talk Colgate (CL).

According to the Yahoo "Profile" on Colgate-Palmolive (CL), this company

"....together with its subsidiaries, manufactures and markets consumer products worldwide. It offers oral care products including toothpaste, toothbrushes, and mouth rinses, as well as dental floss and pharmaceutical products for dentists and other oral health professionals; personal care products, such as liquid hand soap, shower gels, bar soaps, deodorants, antiperspirants, shampoos, and conditioners; and home care products comprising laundry detergents, dishwashing liquids and detergents, household cleaners, and oil soaps, as well as fabric conditioners."

"....together with its subsidiaries, manufactures and markets consumer products worldwide. It offers oral care products including toothpaste, toothbrushes, and mouth rinses, as well as dental floss and pharmaceutical products for dentists and other oral health professionals; personal care products, such as liquid hand soap, shower gels, bar soaps, deodorants, antiperspirants, shampoos, and conditioners; and home care products comprising laundry detergents, dishwashing liquids and detergents, household cleaners, and oil soaps, as well as fabric conditioners."

While I purchased shares of Colgate (CL) as a 'comfort stock' their quarterly report on July 29, 2010, was less than stellar. Colgate reported earning $603 million or $1.17/share in the quarter ended in June, 2010. Those results are up from $562 million in earnings or $1.07/share in the prior year same period. The company beat expectations on earnings as analysts had been expecting $1.16/share but revenue came in light as analysts had been expecting $3.94 billion in revenue. Some of the problems came in from Venezuela where currency devaluation affected results.

Morningstar.com allows us a longer-term perspective on Colgate-Palmolive. We can see that revenue has grown steadily from $11.4 billion in 2005 to $15.330 billion in 2008 with a slight dip to $15.327 billion in 2009. Net income has grown uninterruptedly from $1.35 billion in 2005 to $2.29 billion in 2009. Diluted earnings have also increased without interruption from $2.43/share in 2005 to $4.37/share in 2009.

Free cash flow for CL has increased from $1.39 billion in 2005 to $2.70 billion in 2009. Most recent balance sheet numbes show $3.8 billion in total current assets compared to $3.60 billion in total current liabilities. The company also has $4.42 billion in long-term liabilities reported.

Looking at Yahoo "Key Statistics" on Colgate-Palmolive (CL), we can see that this is a large cap stock with a market capitalization of $36.09 billion. The stock has a trailing p/e of 17.71 with a forward p/e (fye Dec 31, 2011) estimated at 14.22. The PEG ratio is a bit rich at 1.69.

Yahoo reports 486 million shares outstanding with 483.37 million that float. As of August 13, 2010, there were 5 million shares out short representing a short ratio of only 1.40. The forward annual dividend is $2.12 working out to a 2.8% yield. The dividend is well covered with a 44% payout ratio. The last stock split was July 1, 1999, when the stock was split 2:1.

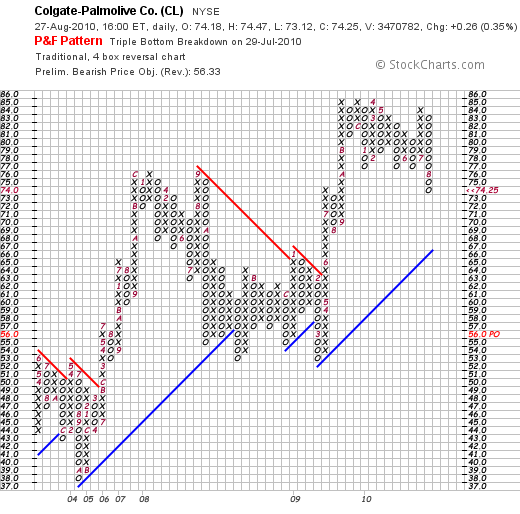

In terms of the technical performance of this stock, if we examine the 'point & figure' chart on Colgate-Palmolive (CL) from StockCharts.com, we can see that looking a little longer-term, CL has traded from a low of $37 back in October, 2004, to a high of $85 in August, 2009. Currently correcting from another pass at the $85 level in July, 2010, the stock has pulled back rather sharply to its current price of $74.25. While short-term a bit weak, longer-term, the trend appears higher.

In summary, I am aware of the difficult times we find ourselves living in, investing in, and even dealing with the politics of the 'cure'. Long-term, I am every bit as bullish on America as Kudlow. But right now, I need a comfort stock. A stock I have grown up with that I use to brush my teeth, clean my dishes, and even shampoo my hair. Colgate is a long-term winner as the rest of the world advances and starts increasingly demand consumer products that Colgate is prepared to deliver.

Long-term, Colgate "has paid uninterrupted dividends on its common stock since 1895 and increased payments to common shareholders every year for 47 years." A very blue blue-chip stock indeed!

Thanks so much for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them right here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Thursday, 19 August 2010

Colgate Palmolive (CL) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website

As part of my strategy of managing my portfolio, I have chosen to sell a small portion of my own holdings as they appreciate to targeted price levels. After an initial purchase, I sell 1/7th of my holding, if it appreciates to a 30% gain from my purchase price. After a sale of a portion of a holding at a gain, I use this action as a 'signal' to indicate to me that the health of the market is reasonable for a new purchase of stock.

As part of my strategy of managing my portfolio, I have chosen to sell a small portion of my own holdings as they appreciate to targeted price levels. After an initial purchase, I sell 1/7th of my holding, if it appreciates to a 30% gain from my purchase price. After a sale of a portion of a holding at a gain, I use this action as a 'signal' to indicate to me that the health of the market is reasonable for a new purchase of stock.

On August 18, 2010, my McDonald's (MCD) shares reached $73.51 and I sold 1/7th of my holding, 7 shares, at $73.51. These shares had been acquired September 23, 2009, at a cost basis of $56.39/share. Thus I had a gain of $17.12 or 30.4% since purchase. I still own 45 shars of MCD in my own portfolio after this sale.

Being under my maximum of 20 holdings, and with this 'permission slip' in hand, I went ahead and44 shares of Colgate Palmolive (CL) at $76.97/share. The size of this purchase was dictated by my own calculation of 125% of the average size of the remaining holdings.

CL has long been a favorite of mine, and along with its dividend and the incredible stability of its product mix, I chose to add it into my portfolio. I shall write up a little more about Colgate Palmolive (CL) and why I chose to add it to my portfolio in the near future.

Yours in investing,

Bob

Sunday, 15 August 2010

Medtronic (MDT) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

In the difficult market that we find ourselves, I also find it difficult to highlight new stocks that I find appropriate to include in this blog and possibly in my own portfolio. Picking up an old copy of "100 Best Stocks to own in America" by Gene Walden (7th edition), (which you can pick up here on Amazon), I opened up the page on Medtronic (MDT) and thought it might be worthwhile to revisit this stock. (Even though Walden's classic is nearly 10 years old, I still find inspiration in his philosophy and discipline.)

I last wrote up Medtronic (MDT) on Stock Picks on November 29, 2009. At this time, I do not own any shares of this stock. Medtronic (MDT) closed at $35.57 on August 13, 2010, down $(.42) on the day.

According to the Yahoo "Profile" on Medtronic (MDT), the company

According to the Yahoo "Profile" on Medtronic (MDT), the company

"...manufactures, and sells device-based medical therapies worldwide. Its Cardiac Rhythm Disease Management segment offers cardiac pacemakers, implantable defibrillators, cardiac resynchronization therapy devices, atrial fibrillation products, leads, ablation products, electrophysiology catheters, information systems, diagnostics and monitoring products, and patient management tools. The company’s Spinal segment offers thoracolumbar, cervical, and interbody spinal devices; bone growth substitutes; and devices for vertebral compression fractures and spinal stenosis. Its CardioVascular segment offers coronary and peripheral stents and related delivery systems, endovascular stent graft systems, distal embolic protection systems, perfusion systems, positioning and stabilization systems, products for the repair and replacement of heart valves, and surgical ablation products, as well as balloon angioplasty catheters, guide catheters, guidewires, diagnostic catheters, and accessories. The company’s Neuromodulation segment offers neurostimulators, implantable drug delivery systems, deep brain stimulation systems, and urology and gastroenterology devices. Its Diabetes segment offers external insulin pumps, continuous glucose monitors, carelink therapy management software, and blood glucose meters. The company’s Surgical Technologies segment offers tissue-removal systems, surgical drill systems, fluid-control products, cranial fixation devices, nerve monitoring systems, image-guided surgery systems, intra-operative imaging systems, a Ménière’s disease therapy device, and a portfolio of products to treat benign snoring and obstructive sleep apnea."

To summarize, they are involved in medical devices that treat heart rhythm, treatment, spinal, CNS, diabetic, and surgical and sleep apnea problems.

Medtronic has announced that it will be reporting on 1st quarter 2011 results on August 24, 2010. They recently announced their completed acquisition of ATS Medical for $370 million expanding their cardiac surgical and diagnostic line of products. Since the 4th quarter report, Medtronic announced a dividend increase of 9% from $.205/share to $.225/share.

On May 25, 2010, Medtronic (MDT) reported 4th quarter 2010 results with revenue growth of 10% from $3.8 billion in the year earlier perior to $4.2 billion this quarter. Analysts had expected $4.19 billion in revenue. Net income rose to $954 million or $.86/share in quarter ended April 30, 2010, up from $103 million or $.09/share the prior year. Adjusted earnings came in at $.89/share, a penny ahead of estimates.

On May 25, 2010, Medtronic (MDT) reported 4th quarter 2010 results with revenue growth of 10% from $3.8 billion in the year earlier perior to $4.2 billion this quarter. Analysts had expected $4.19 billion in revenue. Net income rose to $954 million or $.86/share in quarter ended April 30, 2010, up from $103 million or $.09/share the prior year. Adjusted earnings came in at $.89/share, a penny ahead of estimates.

Longer-term, checking the Morningstar Financials on MDT, we can see that revenue has increased from $11.3 billion in 2006 to $15.8 billion in 2010. Net income has increased from $2.5 billion in 2006 to $3.1 billion in 2010 after a dip in both 2008 and 2009, results rebounded in 2010.

Earnings per share similarly climbed from $2.09/share in 2006 to $2.41/share in 2007, before dipping to $1.95 in 2008 and $1.93 in 2009. Earnings rebounded to $2.79/share in 2010. Outstanding shares have gradually dipped from 1.2 billion in 2006 to 1.1 billion in 2010.

Free cash flow has been strong with $963 million reported in 2006 increasing steadily to $3.56 billion in 2010.

Medtronic's balance sheet appears solid with latest Morningstar results showing $9.8 billion in current assets in 2010 with total current liabilities reported at $5.12 billion. Non-current liabilities are recorded at $8.3 billion.

Checking the Yahoo "Key Statistics" on Medtronic (MDT), we can see that this stock is a large cap stock with a market capitalization of $38.52 billion. The company has a very modest p/e of 12.74 with a forward p/e (fye Apr 30, 2012) of 9.34 with a resultant PEG (5 Yr Expected) of 1.05.

The company has 1.08 billion shares outstanding. As of July 30, 2010, there were 11.46 million shares out short representing a short ratio of only 1.90. The company currently pays a forward dividend of $.90/share with a forward yield of 2.5%. The payout ratio is only 29% suggesting ample room for dividend payment and growth.

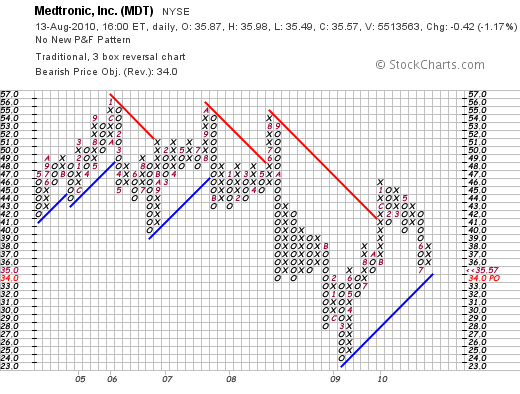

If we examine the "point & figure" chart on Medtronic from StockCharts.com, we can see that the share price broke down from a high of $54 in August, 2008, to a low of $24 in February, 2009, before moving higher through resistance at $41. After a recent peak at $47 in January, 2010, the stock has sold off testing its recent support levels at $35. Overall, the stock appears to be nominally in an uptrend and certainly not over-extended.

In conclusion, Medtronic (MDT) is an old favorite of mine that represents excellent value with a p/e just over 12, a PEG just over 1.0 and a dividend yield of 2.5%. The company reported 2010 results that reversed a two-year slide in earnings and revenue growth. However, they are set to report earnings once again in next ten days.

As we look for 'safe' places to park our investment money, Medtronic may well represent the value and long-term prospects that make this a timely investment.

Thank you again for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them right here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Wednesday, 11 August 2010

Thanks to Fred Wilson!

Hello Friends! Instead of listing the usual disclaimer, I would like to publicly thank Fred Wilson for his kind comments on AVC "musings of a VC in NYC".

Fred is a Venture Capitalist who has invested in and organized investments in a multitude of new organizations including Twitter, Covestor, and foursquare, three of the internet enterprises that occupy a great deal of my own time! Through Union Square Ventures, he has been a powerful influence on social media and social investing websites. Thank you for all you do Fred!

Fred is a Venture Capitalist who has invested in and organized investments in a multitude of new organizations including Twitter, Covestor, and foursquare, three of the internet enterprises that occupy a great deal of my own time! Through Union Square Ventures, he has been a powerful influence on social media and social investing websites. Thank you for all you do Fred!

Fred was kind enough to discuss my own activity with Covestor. (Here is the link to my Covestor page.) Covestor has allowed me to monitor and evaluate my own trading activity and performance and to allow me to share this information with all of you my readers. In addition, if you are so inclined, Covestor allows individuals to shadow fellow investors with portfolios that seek to duplicate the activity of model managers. Visit Covestor to find out more.

We live in very difficult investing times and indeed difficult times even for Venture Capitalists. I shall continue to work to share with you my ideas and rationales for each of the decisions I make as I try to learn along with all of you how to deal with financial markets that can climb 2% one day only to dip 3% the next. Steadiness and consistency are key as well as continued evaluation of the information, assumption, and actual performance that results from any given strategy.

Thank you all for visiting and participating with me on this journey.

If you have any comments or questions, please feel free to leave them right here on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 8 August 2010

PerkinElmer, Inc. (PKI)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Before I get on with my entry about PerkinElmer (PKI), I would like to share with you a special new place on my travel list, Dickey Farms. I just came back from a trip to Atlanta, with a side-stop to visit cousins in Macon, Georgia, who were kind enough to take me to Musella, Georgia to try some famous Georgia Peaches with attention to the soft-serve peach ice cream!

OK I also enjoyed some samples of the peach bread, some fresh free-stone peaches, and drooled over the fried peach pies, peach fritters, peach preserves, and everything peach.

I took this picture this weekend of a couple of the people at Dickey's who help make it all possible. If you stop by, tell them Bob sent you!

I haven't been very active in the trading department as none of my stocks have hit sales on the downside or upside. Unfortunately, the street was very disappointed with Church & Dwight (CHD) which reported 2nd quarter results that while beating expectations, the company forecast profit margins under pressure. On the upside, McDonald's (MCD) continued to show strength even as the economy showed new weakness threatening a double-dip recovery.

Returning to my usual haunts in the top % gainers lists, I came across PerkinElmer, Inc. (PKI) which closed at $22.29 on August 6, 2010, up $2.24 or 11.17% on the day. I do not own any shares of this stock.

Returning to my usual haunts in the top % gainers lists, I came across PerkinElmer, Inc. (PKI) which closed at $22.29 on August 6, 2010, up $2.24 or 11.17% on the day. I do not own any shares of this stock.

PKI moved higher on the back of 2nd quarter earnings that came in at $42.6 million or $.46/share compared with $38.2 million or $.20/share the prior year same period. Sales climbed 14% to $497.8 million. Adjusted earnings came in at $.38/share, ahead of the $.33/share estimate.

PerkinElmer went ahead and raised guidance for the full-year to $1.49 to $1.54/share from prior guidance of $1.43 to $1.48/share ahead of analysts who have been expecting $1.46/share.

The outstanding results led Robert W. Baird analyst Quintin Lai to comment:

"PerkinElmer expects high single-digit organic revenue growth in second-half 2010 with contributions from both human health and environmental health segments," he wrote. Lai rates the stock at "Outperform" with a price target of $29 per share."

According to the Yahoo "Profile" on PerkinElmer (PKI), the company

"...provides technology, services, and solutions to the diagnostics, research, environmental, safety and security, industrial and laboratory services markets. PerkinElmer has the portfolios of functional cellular science research technologies, as well as GPCR and kinase products used in researching approximately 75% of drug pathways. The company operates through two segments, Human Health and Environmental Health."

"...provides technology, services, and solutions to the diagnostics, research, environmental, safety and security, industrial and laboratory services markets. PerkinElmer has the portfolios of functional cellular science research technologies, as well as GPCR and kinase products used in researching approximately 75% of drug pathways. The company operates through two segments, Human Health and Environmental Health."

Looking longer-term at the Morningstar.com "Financials" on PerkinElmer (PKI), we can see that revenue has grown from $1.47 billion in 2005 to $1.94 billion in 2008 before dipping to $1.81 billion in 2009.

PKI has struggled with net income which dipped from $268 million in 2005 to as low as $86 million in 2009. Similarly diluted earnings per share have dipped from $2.04 in 2005 to $.73/share in 2009.

Reviewing the Morningstar information regarding their balance sheet, we can see that the company has current assets of $884 million, easily covering the total current liabilities of $496 million. Total non-current liabilities totals $939 million. The company generated $117 million in free cash flow in 2009 down slightly from the $175 million in free cash flow the prior year.

In terms of valuation, the Yahoo "Key Statistics" on PKI reveal that the market capitalization of $2.63 billion makes this company a mid cap stock. The trailing p/e is a relatively rich 26.22. However, the forward p/e is a reasonable 13.19 (fye Jan 3, 2012), with a PEG (5 yr estimated) even more reasonable at 1.09.

The company has 117.81 million shares outstanding with a float of 116.44 million. As of July 15, 2010, there were 1.73 million shares out short with a modest short ratio of only 1.0.

The company pays a forward annual dividend rate of $.28/share yielding an anticipated 1.4% based on the current price. The last stock split was a 2:1 back on June 4, 2001.

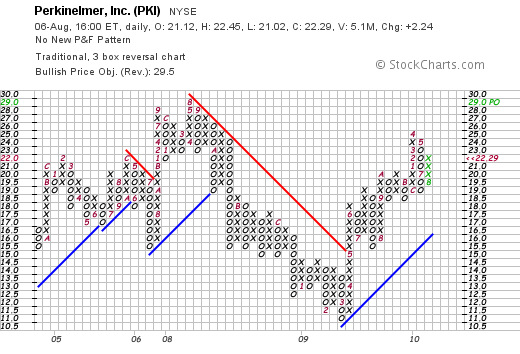

Technically, the 'point & figure' chart from StockCharts.com is encouraging. This stock peaked back in June, 2008, at the $29 level, dipped as low as $11.00 in March, 2009, before rallying back, breaking through resistance at $15 and moving to the current $22.29 level, below the recent high of $25 set in April, 2010.

In summary, PerkinElmers (PKI) appears to be firing on all cylinders after several years of relatively mediocre financial performance. They reported a strong quarter in both of their business segments that beat expectations. They also went ahead and raised guidance for the year. The stock appears to be reasonably priced, pays a small dividend, and has a nice chart to boot! This is the kind of stock that I might consider buying for my own portfolio if the right buy signal could be recorded. Meanwhile, I shall add it to my burgeoning list of appealing stocks on this blog!

Thanks again for visiting! If you have any comments or questions, please feel free to leave them right here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 25 July 2010

Informatica Corporation (INFA)

Hello Friends! Thanks so much for stopping by and visiting my blog Stock Picks Bob's Advice! As always, please remember that I am an amateur so please remember to always consult with your professional investment advisers prior to making any investment decisions based on the information on this website.

With the difficult stock market environment that we have experienced recently, you may have observed and I have written about my move towards 'value' rather than 'growth' investing. I have selected stocks for my own portfolio as well as for this blog to discuss that are what I would call investment 'stalwarts' that are reasonably priced, pay good dividends, and can weather the vagaries of the economy. You have seen me discuss stocks such as Coca-Cola (KO), Sysco (SYY) and McDonald's (MCD). These are certainly terrific companies but I want to try with this post to tip-toe back towards the original intent of this blog, to discuss those companies with steady revenue and earnings growth.

With the difficult stock market environment that we have experienced recently, you may have observed and I have written about my move towards 'value' rather than 'growth' investing. I have selected stocks for my own portfolio as well as for this blog to discuss that are what I would call investment 'stalwarts' that are reasonably priced, pay good dividends, and can weather the vagaries of the economy. You have seen me discuss stocks such as Coca-Cola (KO), Sysco (SYY) and McDonald's (MCD). These are certainly terrific companies but I want to try with this post to tip-toe back towards the original intent of this blog, to discuss those companies with steady revenue and earnings growth.

Informatica (INFA) closed at $30.43, up $3.38 or 12.5% on the day, enough to make the list of top % gainers on the NASDAQ. I do not own any shares of this stock.

According to the Yahoo "Profile" on Informatica (INFA), the company

"...provides enterprise data integration and data quality software and services in the United States and internationally. Its software handles various enterprise-wide data integration initiatives, including data warehousing, data migration, data consolidation, data synchronization, and data quality, as well as the establishment of data hubs, data services, cross-enterprise data exchange, and integration competency centers."

This is not exactly what I would call a "Peter Lynch" style of investment! Not a stock that my daughter is talking about in the local mall. What is compelling about this stock is the financial results that they have and continue to generate.

On July 22, 2010, Informatic reported 2nd quarter results after the close of trading. Revenue for the quarter came in at $155.7 million, ahead of estimates of $143.7 million and earnings came in at $.25/share, also ahead of estimates of $.23/share.

Reviewing the Morningstar.com '5 Years' financials, we can see that revenue has grown from $267 million in 2005 to $325 million in 2006, $391 million in 2007, $456 million in 2008 and $501 million in 2009. It is not just the growth but the consistency of growth that makes this so impressive.

Net income similarly has grown consistently from $34 million in 2005 to $64 million in 2009. Diluted earnings per share have increased from $.37/share in 2005 to $.66/share in 2009 without missing a beat! Outstanding shares have grown modestly from 92 million shares in 2005 to 103 million shares in 2009.

Free cash flow has increased from $28 million in 2005 to $95 million in 2008 but did slip slightly to $74 million in 2009 according to Morningstar.com.

Looking at the Morningstar balance sheet numbers on Informatica (INFA), the company has, as of December, 2009, $614 million in current assets compared to $256 million in current liabilities, yielding a solid current ratio of 2.4. The company is reported to also have what appears to be a very manageable amount of non-current liabilities totaling $251 million.

Reviewing the Yahoo "Key Statistics" on INFA, we can see that this is a mid cap stock with a market capitalization of $2.79 billion. The trailing p/e is rich at 46.46 but with the rapid growth estimated the forward p/e (fye Dec 31, 2011) is estimated at a bit more reasonable 24.34. However, the PEG still comes in a bit rich as well at 1.63. The stock certainly isn't undiscovered :).

INFA has 91.8 million shares outstanding with 90.86 million that float. As of 6/30/10, there were 6.15 million shares out short representing a short ratio of 3.40, just ahead of my own 3 day rule for significance. The company does not pay a dividend and last split its shares with a 2:1 split back on December 14, 2000.

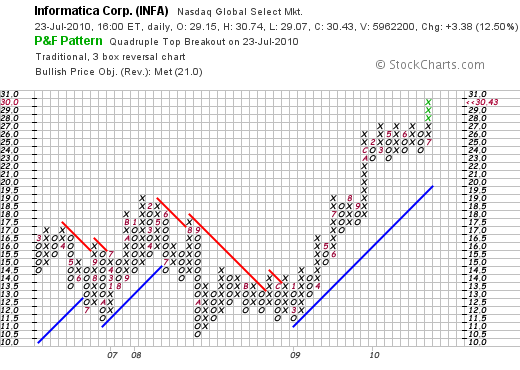

Reviewing the 'point & figure' chart on Informatica (INFA), we can see that the stock traded in a fairly tight range between March, 2006 and July, 2009, between approximately $10.50 and $19.00. In September, 2009, the stock broke out to the upside to a new range between $23 and $27 where it traded in a configuration known as a 'high tight flag' as I understand technical patterns. The stock with its recent move has broken out into a higher price range on good news.

To summarize, Informatica (INFA) had a strong day Friday moving out to new highs on an earnings report that beat expectations. The company has steadily grown its revenue and earnings for the past five years and has a strong balance sheet. However, valuation is a bit rich with a p/e and PEG a big higher than I would like if I were to suggest a 'value' investment. But this represents a terrific tech stock that clearly is capitalizing on the never-ending growth of the information business.

Simply put, it would be a great addition to my own portfolio if I had a signal to be buying a stock!

Thanks again for stopping by and visiting my blog. If you have any comments or questions, please feel free to leave them here on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 18 July 2010

Dr Pepper Snapple Group (DPS)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

We have been having a heat wave in Boston, Southern California, in fact much of the United States, including New York City, as well as overseas in London, and across Russia. Putting it plainly, it has been a hot summer for many across the globe.

We have been having a heat wave in Boston, Southern California, in fact much of the United States, including New York City, as well as overseas in London, and across Russia. Putting it plainly, it has been a hot summer for many across the globe.

It is this hot weather and a bit of a sunburn today after doing a bit of bike-riding that leads me to think about Snapple, and in particular the Dr Pepper Snapple Group (DPS). I do not have any shares of this company but believe it is the kind of stock I would like to be owning! DPS closed at $38.25 on July 16, 2010, down $(.73) or (1.87)% on the day as the market sold off rather severely with the Dow closing at 10,097.50 down 261.41 or (2.52)% on the day. Full disclosure: Diet Peach Tea by Snapple is one of my favorite drinks!

According to the Yahoo "Profile" on Dr Pepper Snapple Group (DPS), the company

According to the Yahoo "Profile" on Dr Pepper Snapple Group (DPS), the company

"...operates as a brand owner, manufacturer, and distributor of non-alcoholic beverages in the United States, Canada, Mexico, and the Caribbean. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, and mixers. The company offers its CSD products primarily under the Dr Pepper, Sunkist soda, 7UP, A&W, Canada Dry, Crush, Schweppes, Squirt, RC Cola, Diet Rite, Sundrop, Welch’s, Vernors, Country Time, IBC, Mistic, and Venom Energy brand names; and NCB products principally under the Snapple, Mott’s, Hawaiian Punch, Clamato, Yoo-Hoo, Country Time, Nantucket Nectars, ReaLemon, Mr and Mrs T, Rose’s, and Margaritaville brand names."

Snapple has a fascinating history beyond its recent association with Quaker Oats and with Dr Pepper:

"Snapple was founded in 1972 by Arnold Greenberg, Leonard Marsh, and Hyman Golden. Greenberg operated a health food store on the lower east side of Manhattan. His boyhood friend Marsh ran a window-washing service with his brother-in-law, Golden. In the early 1970s, the three founded Unadulterated Food Products, Inc., to sell pure fruit juices in unusual blends to health food stores. Products were bottled at a small plant in the New York metropolitan area. The partners ran the business in their spare time while all three kept their regular jobs, and the enterprise plodded along until the late 1970s.

In 1978, Unadulterated Foods began to market carbonated apple juice. The company called the product "Snapple," after purchasing the name for $500."

Dr Pepper Snapple Group (DPS) is a very young company:

"The company was established in 2008 following the spin-off of Cadbury Schweppes Americas Beverages (CSAB) from Cadbury Schweppes plc. On May 7, 2008, DPS became a publicly traded company listed on the New York Stock Exchange."

Snapple became part of Cadbury Schweppes in 2000 after it was purchased from Triarc Group which had acquired Snapple back in 1997.

In any case, in a Peter Lynch fashion, I like their tea and their financial results are attractive. On May 6, 2010, DPS announced 1st quarter results that were a bit less than stellar. Earnings came in at $89 million or $.35/share down from $132 million or $.52/share last year. Excluding one-time charges, the company earned $.40/share, which while behind last year's $.52 result, came in ahead of the $.32/share expected by analysts.

Revenue for the quarter dipped to $1.25 billion from $1.26 billion last year under the $1.28 billion expected by analysts. The company maintained sales guidance for the year with DPS expected to grow sales by 3-5% for the year. In addition, they raised earnings guidance to a new range of $2.29 to $2.37/share, up from prior guidance of $2.27 to $2.35. While reporting a mixed earnings report, the outlook was decidedly upbeat and the stock price has performed well since that report.

Watching my weight (without much success) I also enjoy an occasional Diet Dr. Pepper (for full disclosure!)

Watching my weight (without much success) I also enjoy an occasional Diet Dr. Pepper (for full disclosure!)

If we review the Morningstar Income Statement on Dr Pepper Snapple Group Inc. (DPS), we can see that revenue has grown steadily from 2005 to 2007 from $3.2 billion to $5.7 billion. In 2008 this dipped to $5.7 billion and the company has reported $5.5 billion in the trailing twelve months (TTM).

Earnings dipped from $2.01 in 2006 to a loss of $(1.23) in 2008 and has come in at $2.17/share in the TTM.

Outstanding shares have been stable with 254 million reported in 2006 and 255 million in the TTM.

According to the Morningstar Balance Sheet, the company has $1.28 billion in current assets including $280 million in cash and has total current liabilities of $854 million, yielding a current ratio of nearly 1.5.

Looking at the Morningstar Cash Flow page, we can see that free cash flowhas improved from $373 million in 2007 to $405 million in 2008 and $548 million in 2009.

Some recent news stories affecting the company include an announcement on July 13, 2010, that the board approved a $1 billion buyback of shares to be completed over the next three years. In another positive development for the company, the Coca-Cola Co. (KO) announced on June 7, 2010, that they would be paying $715 million to the Dr Pepper Snapple Groups for rights to distribute Dr Pepper and Canada Dry in United States. They also will be distributing Canada Dr., C Plus, and Schweppes in Canada. Another bullish announcement was made on May 19, 2010, when the company announced a 67% increase in the dividend to $.25/share or $1.00/share on an annual basis.

Examining the Yahoo "Key Statistics" on DPS, we can see that this is a larger 'mid cap stock' with a market capitalization of $9.4 billion. The trailing p/e is a moderate 19.08 with a forward p/e of 13.66 (fye Dec 31, 2011). Thus, the PEG is reasonably valued at 1.37.

Other valuation numbers include the Price/Sales ratio (TTM) which comes in at 1.75, below the industry average of 2.62 according to the Fidelity.com eresearch website. However, profit margins which include Return on Sales (TTM) come in at 9.28% under the industry average of 14.96%. Similarly return on investment comes in at 7.28% below the industry average of 17.06%.

Yahoo reports that as of June 30, 2010, there were 6.25 million shares out short representing only 1.7 trading days, well below my own arbitrary 3 day rule for short interest. As noted above, the company pays a forward dividend of $1.00/share yielding a not-insignificant 2.60%. The company has a payout ratio of only 15%.

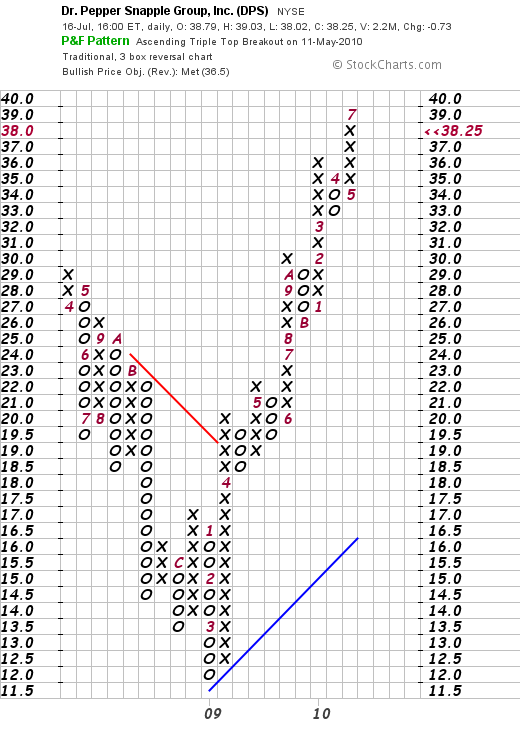

Reviewing the StockCharts.com 'point & figure' chart on Dr Pepper Snapple Group (DPS) we can see that after coming public in April, 2008, the stock peaked at $29 before slipping to a low of $12.00 in March, 2009. Since then the stock has been quite strong hitting a recent high this month at $39/share. Overall the chart looks quite strong if a bit extended.

To summarize, in the heat of this summer with the market acting quite cold, I would like to share with you a cold drink and a warm investment :). Dr Pepper Snapple Group (DPS) is a relatively new company with a stable of beverage products well established in the market. While their latest quarterly report was still showing the effects of the recession, the company guided earnings higher, maintained revenue growth expectations, and recently sharply increased the dividend and announced a three year $1 billion stock buy-back.

I do not own any shares and still limit my new position purchases from signals generated by my own portfolio as it reaches selling points on gains. These signals do not appear to be imminent but DPS is the kind of investment that deserves to be on your tray, or should I say an investment that deserves to be consumed over ice?

Thanks again for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them right here on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Tuesday, 29 June 2010

Ecolab (ECL) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers.

The stock market had a miserable day today. The Dow closed down 268 points or (2.65)%, the Nasdaq was worse with an 85 point or (3.85)% loss. Even the S&P was hit, closing at 1041, down 33 or (3.10)% on the day.

The stock market had a miserable day today. The Dow closed down 268 points or (2.65)%, the Nasdaq was worse with an 85 point or (3.85)% loss. Even the S&P was hit, closing at 1041, down 33 or (3.10)% on the day.

In the midst of this bloodbath, my Ecolab (ECL) stock, which I had recently purchased last month on 4/30/10 in my swith from Schlumberger (SLB), was made at a cost basis of $49.10. I sold all 65 of my shares today at $45.05/share, yielding me a loss of $(4.05) or (8.2)% since purchase.

I did not sell this stock because of any particular fundamental piece of information that disturbed me. I like this company and would prefer to be a shareholder of its shares.

However, my own trading system demands of me to sell shares in companies in which I have made an initial purchase when they have declined (8)% since that purchase. That is exactly what happened to my Ecolab (ECL) shares.

It is also not surprising that this holding was a recent purchase.

It makes sense that the positions that would be 'undone' first would be the recent purchases that are most vulnerable to a downdraft in the market.

One of my goals in pursuing this blog and putting my own real holdings, my successes and failures out publicly is to test whether one can reall do what I am striving to do. I am working to minimize my losses both individually by selling stocks quickly should they decline and also to utilize that sale as an indicator in itself that something is rotten with the market. Thus the proceeds of this sale are remaining in cash.

My cash position is approximately 40% now. I didn't do this on purpose. It wasn't a stroke of genius. It was my own strategy of selling holdings on declines and putting the proceeds in cash. I am avoiding reinvesting these sales on losses so I shall not make a bigger mistake and compound these losses with additional sales on losses.

I shall be waiting for a sale on a gain to be adding a new holding. This may be awhile. Meanwhile, I shall be patient. Monitor my own holdings and am prepared to unload additional stocks until I am at my minimum of 5 holdings. Even then, I shall not tolerate losses but rather shall sell these at 8% declines, replacing them as well with new positions (because I need 5 holdings) but am planning to do this with even smaller in size positions as I work to reduce my exposure to equities as indicated by my own sales.

Thank you again for stopping by and visiting. I hope that my explanation is comprehensible for you. If not, please let me explain more. You can leave your questions or comments right here on the blog or contact me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 27 June 2010

PetSmart (PETM) Podcast

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions.

Click HERE to get to my Podomatic Podcast page to listen to my podcast on PetSmart (PETM).

Thanks again for stopping by! If you have any comments or questions, please feel free to leave them here or drop me a line at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

PetSmart Inc. (PETM) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

The United States economy remains stuck in a slow recovery from a deep recession. Latest figures suggest that the first quarter resulted in a 2.7% growth rate, slightly under the 3% expected.

The United States economy remains stuck in a slow recovery from a deep recession. Latest figures suggest that the first quarter resulted in a 2.7% growth rate, slightly under the 3% expected.

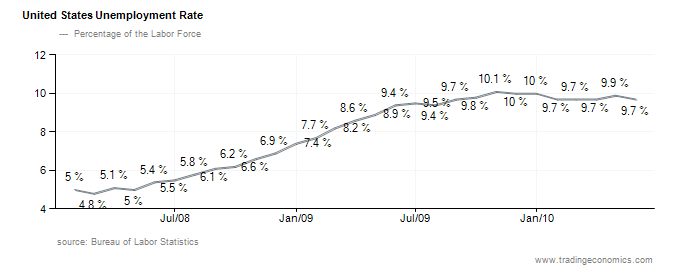

Meanwhile, the United States Unemployment rate remains mired just under 10% with 9.7% unemployed as of May, 2010. As the following chart reveals, while the deterioration in unemployment has stabilized, the United States has not yet convincingly turned the corner in reducing unemployment.

In the midst of this, Democrats in the Senate failed to get through any extension of unemployment benefits in a bill that also would provide federal aid to cash-strapped states and raise taxes on executives of buyout firms.

Republicans are concerned about the ever-growing national debt which just topped $13 Trillion. Democrats, however, argue that the time for dealing with debt is in times of expansion, and that the current economic environment requires expansionary fiscal policy. Republicans have built their recent rebound on Americans distrust of Keynesian economic theory that advocates government spending in times of economic weakness. As this poll suggests, most Americans believe we should be concerned about our debt even as our nation is mired in a recession.

It is in this environment that stock-picking is difficult at best. I remain committed to identifying the highest quality companies which show persistence in growth both in terms of revenue and earnings, and are also able to operate in a financially sound fashion.

There is some evidence that the pet industry may be a recession-resistant sector. PetSmart (PETM) is an important player in this field. I last reviewed PetSmart on May 21, 2009, when the stock was trading at $20.35/share. PetSmart (PETM) closed at $30.91 on June 25, 2010, for a gain of $10.56 or 51.9% since my write-up last year. Unfortunately, I no longer own any shares but do believe this is a stock that belongs in my blog and should be considered for my own portfolio.

Let's take another look at some of the things that keep me interested in this company!

According to the Yahoo "Profile" on PetSmart, the company

According to the Yahoo "Profile" on PetSmart, the company

"... together with its subsidiaries, operates as a specialty retailer of products, services, and solutions for pets in North America."

and

"As of March 25, 2010, it operated 1,149 retail stores; and 162 PetsHotels. Additionally, the company operated 740 hospitals under the registered trade names of Banfield and The Pet Hospital; and had 12 hospitals, which are operated by other third parties in Canada."

In terms of news, the company announced last week (6/22/10) two actions that should be considered 'bullish' for the company stock price. PETM announced that the quarterly dividend would be increased 25% to $.125/share. In addition, the company also announced a new $400 million share repurchase program to replace its current $350 million buyback.

On May 26, 2010, PetSmart announced 1st quarter results. First quarter earnings came in at $44.6 million, or $.46/share for the quarter, ahead of last year's $46.3 million or $.37/share. This exceeded analysts' expectations of $.43/share. Revenue came in at $1.4 billion, slightly ahead of analysts' expectations of $1.38 billion. As I like to see, PETM management also raised guidance for the full year to $1.82 to $1.92/share, ahead of current guidance of $1.73 to $1.83/share. Beating expectations and raising guidance are bullish indicators for a stock price.

The company was impacted by currency fluctuations with net sales positively boosted by $12 million. During the quarter, same-store sales growth was reported at 2.8%.

Reviewing the Morningstar.com "5-Yr Restated" financials on PetSmart, we can see that revenue growth steadily climbed from $3.76 billion in 2006 to $5.34 billion in 2010 with $5.4 billion reported in the trailing twelve months (TTM). Earnings, however, increased from $1.25/share in 2006 to a peak of $1.95/share in 2008, dipped to $1.52/share in 2009, increased to $1.59 in 2010 and $1.69 in the TTM as the company recovered its earnings growth.

The company pays a dividend and increased it from $.12/share in 2008 to $.33/share in 2010 and again to $.40/share in the TTM. With the quarterly increase to $.125/share noted above, the current dividend rate is at $.50/share. Outstanding shares have been decreasing recently from 146 million in 2006 to 125 million in 2010 and 123 million in the TTM.

Free cash flow is solidly positive, increasing from $38 million in 2008 to $454 million in 2010 with a slight decrease to $373 million in the TTM.

The balance sheet looks solid with $242 million in cash reported and $788 million in other current assets. This compares with $537.8 million in current liabilities yielding a 'current ratio' of 1.92.

(Image from article on 'The pet economy')

In terms of valuation, checking the Yahoo "Key Statistics" on PetSmart, we find that the company is a mid-cap stock with a market capitalization of $3.66 billion.

Yahoo reports the company with a trailing p/e of 18.33, with a forward p/e (fye Jan 31, 2012) estimated at 14.18. With the rapid growth in earnings predicted, this somewhat rich p/e is more reasonable in light of this growth with a PEG (5 yr expected) of 1.19, within my own range of 1.0-1.5 for 'value'. According to the Fidelity eresearch website, the company has a Price/Sales (TTM) ratio of 0.70, well under the industry average of 0.85. Its Return on Sales (TTM) at 3.84% is under the industry average of 5.37%, also its Return on Investment (TTM) of 11.83% also is a bit below the industry average of 15.41%.

According to Yahoo, there are 118.33 million shares outstanding with 117.07 million that float. 5.84 million shares are reported out short as of 6/15/10, with a short ratio of 3.60 slightly ahead of my own arbitrary 3 day rule of significance. (Higher short positions might be considered bullish.)

As I noted above, the company has a forward dividend yield of 1.60% based on a forward dividend rate of $.50/share annually. The last stock split was a 2:1 split back in July, 1996.

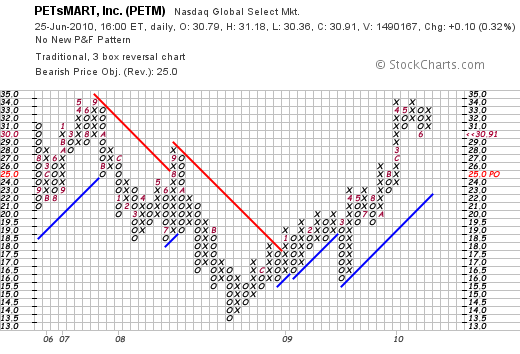

Reviewing the 'point & figure' chart on PETM from StockCharts.com, we can see that this stock bottomed back in August, 2008 at $13/share. Since then, except for a slight setback in March, 2009, the stock has shown remarkable strength as it currently trades above support lines just below the recent highs in the $34 range.

OK maybe I do have a soft spot for animals. (This is a picture of my cat Rahmmy, who was named Mickey, when I picked him up at PetSmart! He was a cat from the Coulee Region Humane Society and couldn't be better! (except when he's naughty.) ). But seriously, PetSmart, a stock that I have owned in the past and have also reviewed deserves consideration.

OK maybe I do have a soft spot for animals. (This is a picture of my cat Rahmmy, who was named Mickey, when I picked him up at PetSmart! He was a cat from the Coulee Region Humane Society and couldn't be better! (except when he's naughty.) ). But seriously, PetSmart, a stock that I have owned in the past and have also reviewed deserves consideration.

They have recently raised their dividend, announced an expanded stock buy-back, and reported earnings which exceeded expectations and raised guidance for the full year. Their long-term financial record is excellent if not perfect, and their chart looks quite strong.

Now, if only the general economy would cooperate a bit!

Thank you for stopping by and visiting my blog. Please feel free to leave any comments or questions right here on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in invesiting,

Bob

Posted by bobsadviceforstocks at 3:34 PM CDT

|

Post Comment |

Permalink

Updated: Sunday, 27 June 2010 9:29 PM CDT

Newer | Latest | Older