Stock Picks Bob's Advice

Wednesday, 26 June 2013

Heartland Payment Systems (HPY)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please consult with your professional investment advisers prior to making any investment decisions based on information on this website.

With the market's recent correction, I found myself selling a couple of recent purchases including Interxions Holdings NV (INXN) after accruing a small loss after my initial purchase in my Covestor Growth and Momentum Model. However, with the stock market rebounding on realization that the sky was indeed not falling, I found myself looking around for a new position and decided upon Heartland Payment Services (HPY). On June 25, 2013, I picked up shares of Heartland Payment Systems (HPY) at a cost of $34.46. HPY closed at $35.96 on 6/26/13, up $1.50 or 4.35% on the day. Thus far, it has been a good purchase for the portfolio.

With the market's recent correction, I found myself selling a couple of recent purchases including Interxions Holdings NV (INXN) after accruing a small loss after my initial purchase in my Covestor Growth and Momentum Model. However, with the stock market rebounding on realization that the sky was indeed not falling, I found myself looking around for a new position and decided upon Heartland Payment Services (HPY). On June 25, 2013, I picked up shares of Heartland Payment Systems (HPY) at a cost of $34.46. HPY closed at $35.96 on 6/26/13, up $1.50 or 4.35% on the day. Thus far, it has been a good purchase for the portfolio.

According to the Yahoo "Profile" on HPY, the company

"...provides bankcard payment processing services in the United States  and Canada. It facilitates the exchange of information and funds between merchants and cardholder’s financial institutions; and offers end-to-end electronic payment processing services, including merchant set-up and training, transaction authorization and electronic draft capture, clearing and settlement, merchant accounting, merchant assistance and support, and risk management to merchants. The company also provides other merchant services comprising payroll processing, gift and loyalty programs, and prepaid and stored-value solutions; paper check processing; payroll and related tax filing services; and secure point-of-sale solutions, as well as sells and rents point-of-sale devices and supplies."

and Canada. It facilitates the exchange of information and funds between merchants and cardholder’s financial institutions; and offers end-to-end electronic payment processing services, including merchant set-up and training, transaction authorization and electronic draft capture, clearing and settlement, merchant accounting, merchant assistance and support, and risk management to merchants. The company also provides other merchant services comprising payroll processing, gift and loyalty programs, and prepaid and stored-value solutions; paper check processing; payroll and related tax filing services; and secure point-of-sale solutions, as well as sells and rents point-of-sale devices and supplies."

On April 30, 2013, Heartland Payment Services announced 1st quarter 2013 results. Revenue came in at $501.2 million, up 7% from the prior year's $467.6 million. This was slightly under analysts expectations of $511.5 million. Earnings, however, came in at $.41/share (after stock-based compensation and other items) ahead of analysts' expectations of $.40/share. Net income climbed 42% year-over-year to $19.6 million or $.51/share compared to the prior year result of $13.8 million or $.34/share.

The company also raised guidance for 2013 results to adjusted earnings between $2.29 and $2.33/share ahead of analysts who had been expecting earnings of $1.94/share. All-in-all a very solid report in a relatively weak economic environment.

Longer-term, reviewing the Morningstar.com "Financials" on Heartland Payment Systems, we can see that revenue has grown steadily from $1.54 billion in 2008 to $2.013 billion in 2012 and $2.047 billion in the trailing twelve months (TTM). Operating income came in at $71 million in 2008 then dipped to $46 million in 2010 then rebounded strongly to $78 million in 2011, $110 million in 2012 and $114 million in the TTM.

Similarly earnings per share dipped from $1.08 in 2008 to a loss of $(1.38) in 2009, then rebounded sharply to $.88/share in 2010, $1.09/share in 2011, $1.64/share in 2012 and $1.81/share in the TTM.

Looking at the HPY "Balance Sheet" figures from Morningstar.com, this company is reported to have total current assets of $409 million and total current liabilities of $495 million, yielding a Current Ratio of .83, a bit below a minimum of 1.0 suggesting that the company might have some financial stress meeting current obligations. Free cash flow of $106 million in the TTM however suggests that the company is generating enough cash to pay its current obligations and also pay a dividend. In fact, the company has been paying a dividend since 2006 and has been raising iton a regular basis as this payment history reflects.

In terms of valuation, examination of some of the Yahoo "Key Statistics" on Heartland reveals that the company is a small cap stock with a Market Capitalization of only $1.31 billion. The trailing P/E is a moderate 19.77 with a forward P/E (fye Dec 31, 2014) estimated at 16.35. With its rapid growth in earnings, the "G" in the PEG ratio is large enough that the PEG ratio works out to a modest 1.13.

Yahoo reports only 36.33 million shares outstanding with 35.02 million that float. As of May 31, 2013, there were 9.54 million shares out short creating a very significant short interest ratio of 13.20. (Generally I arbitrarily view 3 days as my own 'cut-off' for significance). With good news and an increasing stock price, we may be setting the stage for a 'squeeze' on short-sellers of this stock. As a holder of these shares, one can only hope!

Heartland Payment Systems (HPY) pays a forward estimated dividend of $.28/share with a modest yield of 0.80%. This is ahead of the trailing dividend of $.26/share. No stock splits are reported on Yahoo.

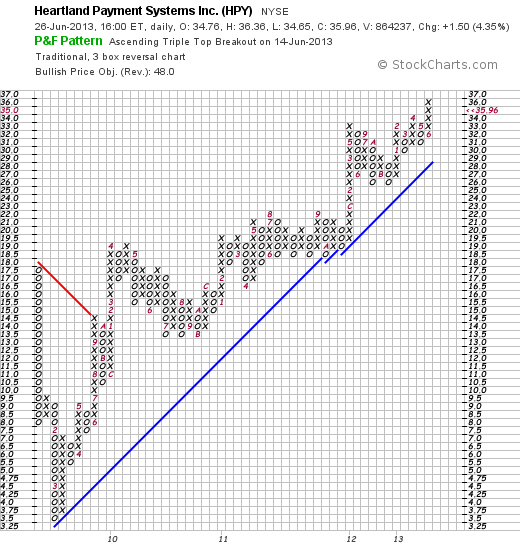

Examining the 'point and figure' chart on HPY from StockCharts.com, we can see that after a sharp sell-off in early 2009 from $17.50/share to a low of $3.50/share in February, 2009, HPY has had a remarkable record of price appreciation to its current level of $35.96. This is a very strong technical chart in my amateur perspective.

If we put this all together we have an interesting company involved in credit card processing and online payment processing for businesses that recently reported a strong quarter that while coming in a bit under expectations in terms of revenue, exceeded analysts' views in terms of earnings. The company confidently raised guidance for the year ahead of what was expected. This all done in a relatively weak economic environment.

Looking at some of the financials from Morningstar, the company has grown its revenue and earnings in a very strong fashion the past few years. Their current ratio is a bit weak which deserves some attention but the strong free cash flow and the confidence the company has demonstrated with boosting its cash dividend and expanding its share buyback, suggest that this isn't very significant. Furthermore, the valuation is really modest with the strong growth in earnings giving us a PEG just over 1.0. To top it off, there are a lot of naysayers outstanding with a large short interest ratio suggesting lots of shares that are waiting to be covered with purchases likely to support the stock price appreciation.

There aren't any perfect stocks. I suppose like there aren't any perfect investors. Yours truly included. I also get anxious as markets decline and confess to occasional euphoria as they climb. I will maintain my discipline of selling stocks, even ones like this, if they do decline in the market to limit my losses. However, if we as investors can get a bit lucky and get ahead of the stock price we may be able to ride a stock higher as it grows hopefully for a very long time.

Thanks so much for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them right here.

Yours in investing.

Bob

Monday, 17 June 2013

Medtronic (MDT)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

One of my recent purchases for my Covestor Healthcare Model is Medtronic, Inc. (MDT). I purchased shares May 1, 2013, at an effective cost of $47.00. Medtronic closed at $53.51, up $.59 or 1.11% on the day (June 17, 2013). This is already a strong performer in my portfolio.

One of my recent purchases for my Covestor Healthcare Model is Medtronic, Inc. (MDT). I purchased shares May 1, 2013, at an effective cost of $47.00. Medtronic closed at $53.51, up $.59 or 1.11% on the day (June 17, 2013). This is already a strong performer in my portfolio.

Being located in the midwest, I am always proud of America's most innovative companies originating in the 'heartland'. Medtronic is headquartered just north of Minneapolis in the city of Fridley.

Medtronic has a classic history of American innovation. As the Medtornic website relates:

"Today, we are the world's largest medical technology company, but we come from humble beginnings. Medtronic was founded in 1949 as a medical equipment repair shop by Earl Bakken and his brother-in-law, Palmer Hermundslie.

"Today, we are the world's largest medical technology company, but we come from humble beginnings. Medtronic was founded in 1949 as a medical equipment repair shop by Earl Bakken and his brother-in-law, Palmer Hermundslie.

Did these two men set out to change medical technology and the lives of millions of people? No. But they did have a deep moral purpose and an inner drive to use their scientific knowledge and entrepreneurial skills to help others."

According to the Yahoo "Profile" on Medtronic, the company

"...provides products to diagnose, treat, and manage heart rhythm disorders and heart failure, including implantable cardiac pacemakers, implantable cardioverter defibrillators, cardiac resynchronization therapy devices, arctic front cardiac cryoablation catheters, arctic front cardiac cryoablation catheters, and patient management tools. The company also offers cardio vascular products, such as percutaneous coronary intervention device that is used to treat  patients with coronary artery disease; renal denervation for the treatment of chronic uncontrolled hypertension; endovascular stent grafts to treat abdomen and thoracic regions of the aorta; peripheral vascular intervention that encompasses various procedures to treat patients with peripheral vascular disease; surgical valve replacement and repair products for damaged or diseased heart valves; transcatheter heart valves; a line of blood-handling products used in arrested heart surgeries; positioning and stabilization technologies that assist physicians performing beating heart surgery; and surgical ablation system, which allows cardiac surgeons to create ablation lines during cardiac surgery. In addition, it provides medical devices and implants that are used in the treatment of the spine and musculoskeletal system comprising thoracolumbar, cervical, and biologics products; neurostimulators for chronic pain, implantable drug delivery systems, and deep brain stimulation systems, as well as urology, fecal, and gastroenterology devices; and integrated diabetes management solutions. Further, the company offers products and therapies to treat diseases and conditions of the ear, nose, and throat, as well as certain neurological disorders; and image-guided surgery and intra-operative imaging systems."

patients with coronary artery disease; renal denervation for the treatment of chronic uncontrolled hypertension; endovascular stent grafts to treat abdomen and thoracic regions of the aorta; peripheral vascular intervention that encompasses various procedures to treat patients with peripheral vascular disease; surgical valve replacement and repair products for damaged or diseased heart valves; transcatheter heart valves; a line of blood-handling products used in arrested heart surgeries; positioning and stabilization technologies that assist physicians performing beating heart surgery; and surgical ablation system, which allows cardiac surgeons to create ablation lines during cardiac surgery. In addition, it provides medical devices and implants that are used in the treatment of the spine and musculoskeletal system comprising thoracolumbar, cervical, and biologics products; neurostimulators for chronic pain, implantable drug delivery systems, and deep brain stimulation systems, as well as urology, fecal, and gastroenterology devices; and integrated diabetes management solutions. Further, the company offers products and therapies to treat diseases and conditions of the ear, nose, and throat, as well as certain neurological disorders; and image-guided surgery and intra-operative imaging systems."

Medtronic (MDT) has been a favorite on my blog. I first wrote up Medtronic on November 13, 2003 (excuse the typo on the entry that says incorrectly 2002). I then revisited this stock pick on November 29, 2009. One has to be impressed with the wide breadth of medical technology products coming out of this company and the continued innovation. In fact, in 2010 Medtronic was recognized by the Massachusetts Institute of Technology Review as one of the 50 most innovative companies in the world.

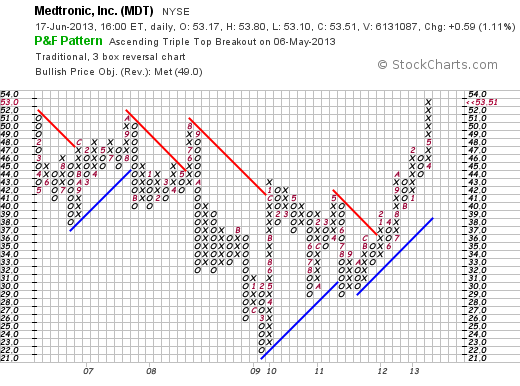

What really attracted me to the company last month was the strong technical strength of the stock as it began to clear past stock price 'highs' set in 2007 and 2008. As this StockCharts.com 'point & figure' chart shows, the company has had a superb performance since bottoming out at about $21 in March, 2009, and has moved strongly ahead, at first with a sharp correction in May, 2011.

To be sure, Medtronic (MDT) has found itself embroiled in controversy over the years with the Medtronic Infuse scandal being typical as accusations of payments from Medtronic to investigators publishing review articles. In May, 2012, the Department of Justice closed their investigation of Medtronic without finding any wrongdoing in regards to the Infuse Bone Graft product. For the most part this 'overhang' of litigation that has suppressed the stock price, from my perspective, has been removed. However, trial attorneys are still seeking plaintiffs for continued litigation against the company. In any case, the above chart suggests that investors have breathed a collective sigh of relief with the Justice Department decision and the company stock appears to be continuing to appreciate to multi-year highs.

Part of the continued bump in the stock price has been the company's latest financial results. On May 21st Medtronic (MDT) reported 4th quarter results. Net income came in at $969 million, or $.96/share ahead of last year's $991 million or $.94/share. Sales also grew to $4.46 billion against last year's $4.3 billion. Adjusted earnings were $1.10/share ahead of analysts' estimated $1.03 in earnings. Sales also exceeded expectations of $4.38 billion. The company raised guidance for revenue to $17.1 billion to $17.3 billion in 2014 ahead of FactSet estimates of $16.9 billion.

Reviewing the Morningstar.com financials on MDT, we can see that Medtronic is continuing to grow its revenue with $13.5 billion reported in 2008 increasing to $16.2 billion in 2012 and $16.4 billion in the trailing twelve months (TTM). More recently the rate of revenue growth has decreased from rates of growth between 2008-2010.

Diluted earnings per share have grown from $1.95/share in 2008 to $3.41 in 2012 and a slight dip to $3.38 in the TTM. Outstanding shares have steadily decreased from 1.14 billion in 2008 to 1.03 billion in the TTM. Medtronic continues to actively buy back its own shares supporting some of the 'per share' results noted.

In terms of the balance sheet, Morningstar reports Medtronic with current assets of $9.5 billion, and current liabilities of $5.9 billion yielding a Current Ratio of 1.61. Medtronic has nicely grown free cash flow from $2.88 billion in 2008 to $3.97 billion in 2012 and $4.28 billion in the TTM.

Looking at some Key Statistics on Medtronic from Yahoo, we can see that this is a large cap stock with a market capitalization of $54.37 billion. The trailing P/E is a moderate 15.88 with a forward P/E (fye Apr 26, 2015) working out to 12.99. The PEG ratio, however, remains rich at 2.03 with only a modest growth in earnings expected.

Yahoo reports 1.02 billion shares outstanding with 1.01 billion that float. As of May 31, 2013, there were 10.64 million shares out short yielding a short interest ratio of only 2.0. (Under my own arbitrary 3 day rule for significance). The company pays a nice dividend of $1.04 yielding 2%. The payout ratio is a moderate 31% suggesting ample room for further dividend boosts. The last time the stock was split was back in September, 1999, when shareholders got a 100% stock dividend for a 2:1 stock split.

To summarize, Medtronic has over the past several years been embroiled in some controversy regarding research results and payments to investigators. The Justice Department has found no evidence of significant wrongdoing and has closed its case. The company meanwhile has continued to generate very large amounts of cash, using it to pay an increasing stock dividend and purchase back its own shares.

The company produces many innovative products spanning multiple fields of medicine from Orthopedics, to Cardiology to Nephrology. It is unnecessary to remind anyone that as our population ages and as more people in this country through the Affordable Care Act ('Obamacare") and overseas through growing middle class populations in nations like India and China find their access to healthcare improving, that purchases of medical devices by practitioners is likely to continue to grow.

Finally, after years of essentially going 'nowhere' the stock appears to be breaking out to multi-year highs and demonstrates strong price momentum. I liked this stock enough to buy some shares and thus far it appears to be a good decision. Like all of my purchases, I always reserve the right to sell any position on either technical or fundamental weakness, a discipline I believe is essential to success in investing.

Thank you so much for stopping by and visiting this website once again. If you have any comments or questions, please feel free to leave them right here.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 10:44 PM CDT

|

Post Comment |

Permalink

Updated: Monday, 17 June 2013 10:47 PM CDT

Sunday, 9 June 2013

Tile Shop Holdings, Inc. (TTS)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on this website.

Last week I purchased shares of Tile Shop Holdings, Inc. (TTS) in my Covestor Growth and Momentum model. The shares were acquired on June 6, 2013, at a cost of $27.12/share. TTS closed at $28.78 on June 7th, 2013, for a gain of $1.66 or 6.12% on the day.

Last week I purchased shares of Tile Shop Holdings, Inc. (TTS) in my Covestor Growth and Momentum model. The shares were acquired on June 6, 2013, at a cost of $27.12/share. TTS closed at $28.78 on June 7th, 2013, for a gain of $1.66 or 6.12% on the day.

The Tile Shop appears to be benefiting from the housing rebound and the recent news of a rebound in the price of housing in the United States. A similar argument could made for Lumber Liquidators (LL) that I reviewed here previously and is a strong performer in my Covestor Growth and Momentum Model already. This same housing rebound is driving other stocks like Home Depot to all-time highs.

According to the Yahoo Profile on Tile Shop Holdings, the company

According to the Yahoo Profile on Tile Shop Holdings, the company

"...operates as a specialty retailer of manufactured and natural stone tiles, setting and maintenance materials, and related accessories in the United States. It offers floor, wall, natural stone, ceramic, porcelain, glass, and metal tile products; tile patterns; basins; fixtures; listellos/borders; and profiles. The company also provides installation products consisting of heated floors, shower pans, tile threshold and edging products, sealants and caulks, tile maintenance and cleaning products, adhesives, substrates, and recessed shelves, as well as installation, cutting, and grout tools; and care and maintenance products. As of January 2, 2013, it operated 68 stores in 21 states."

On May 1, 2013, The Tile Shop (TTS) reported 1st quarter 2013 results. Net sales increased 23.9% to $56.8 million for the quarter ended March 31, 2013 up from $45.9 million in sales for the same quarter the prior year. Importantly, comparable store sales grew 10.4%, and sales in new stores added $6.2 million. Adjusted EBITDA grew 17.9% to $16.4 million, up from $13.9 million the prior year. However, going forward analysts have decreased their estimates for the next quarter to a profit of $.15 from $.16 and for the year estimates have dropped to $.51/share from $.55/share previously estimated.

Reviewing the Morningstar.com Financials on TTS, we can see that the data is limited as the company went public in 2012.The Tile Shop is not a new outfit as it dates back to 1985 when it opened its first shop in Rochester, Minnesota. In 1992, the company expanded outside of Minnesota and has continued to add stores and expand its business territory since.

The Morningstar report shows that the company increased its revenue from $183 million in 2012 to $194 million in the trailing twelve months (TTM). Earnings have actually decreased as the company is still losing money with $(1.31) reported in 2012, and $(2.61) reported in the TTM. The company has increased its float from 6 million shares in 2010 to 36 million in 2012 and 39 million in the TTM.

In terms of the Morningstar-reported balance sheet for TTS, the company has $72 million in total current assets and $36 million in total current liabilities yielding a current ratio of 2.0. The company is generating postive free cash flow as reported by Morningstar, with $18 million reported in 2012 and $12 million in the TTM.

In terms of some valuation numbers, referring to the Key Statistics on Yahoo for Tile Shop Holdings (TTS), Tile Shop Holdings is a small cap stock with a market capitalization of $1.53 billion. With a trailing loss, there is no P/E ratio, but going forward the PEG ratio (5 yr expected) is a bit rich at 2.26. There are 53.13 million shares outstanding with 20.35 million that float. As of May 15, 2013, there were 421,830 shares out short yielding a short interest ratio of 2.20. (This is below my own arbitrary 3 day rule for significance.) No dividends are paid and no stock splits are reported by Yahoo.

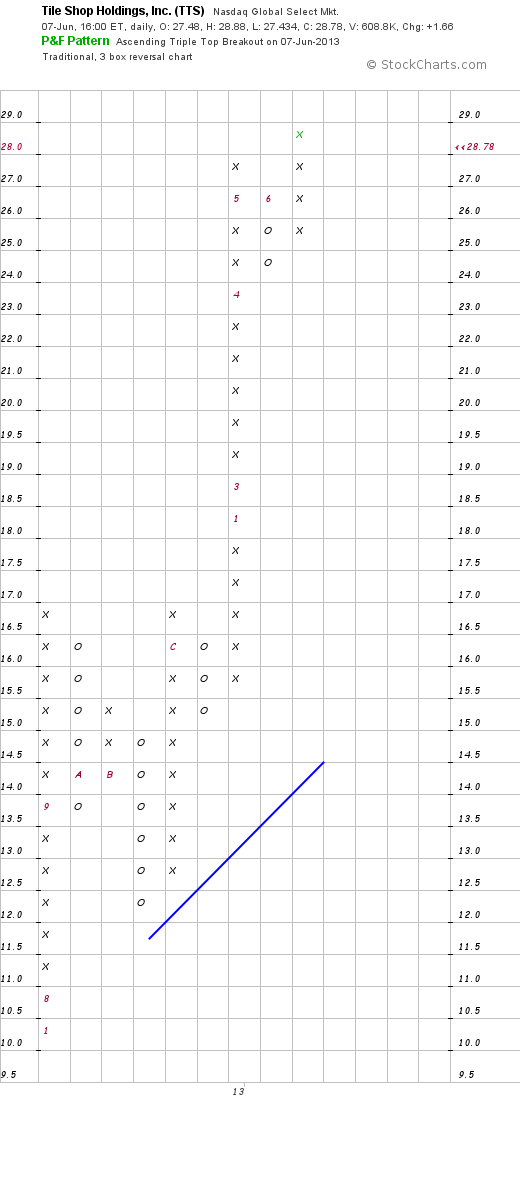

Looking at the 'point and figure' chart on Tile Shop Holdings (TTS) from StockCharts.com we can see a very strong but limited chart.

Reviewing some of the recent analyses on Tile Shop Holdings, Motley Fool published a nice article on this company's ability to play 'America's Housing Boom'. Josh Arnold also wrote a nice review of The Tile Shop on Seeking Alpha.

To summarize, I am a recent purchaser of Tile Shop Holdings (TTS) stock in my Covestor Growth and Momentum Model. This is a very small company that is growing quickly and participating in the rebound of real estate, especially housing in this country. This strategy has worked well with my purchase of Lumber Liquidators (LL) which also is involved in flooring but hardwood floors rather than tile sales. In general, I am a big advocate of identifying retail concepts that can be 'rolled out' from a small base to a larger number of stores in a broader geographic area. The fact that TTS has done so this past year with strong (10%+) same-store-sales growth is very encouraging.

On the negative side, the company is still losing money and even going five years out, the current valuation is a bit rich as estimated by the PEG ratio reported.

With the very strong chart and technical strength and with a 'story' that is quite compelling, I added a position to my own holdings and am optimistic that this will prove to be a good move. Like any of my purchases, if the stock incurs a loss, I shall be quick to part company regardless of my belief in the long-term outlook.

Thank you so much for stopping by and visiting. If you have any comments or questions, please feel free to leave them right here.

Yours in investing,

Bob

Saturday, 30 March 2013

Lumber Liquidators (LL)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Lumber Liquidators represents the strongest holding in my Covestor "Growth and Momentum" model. (This model was formerly called "Buy and Hold Value" but was renamed to reflect the underlying strategy more accurately.) I first purchased shares of Lumber Liquidators (LL on June 26, 2012 at a cost of $32.46 and subsequently took some profits by selling a few shares on September 11, 2012 at $48.13 and again sold a few shares at $65.25 on March 8, 2013. Lumber Liquidators (LL) closed at $770.22, up $.75 or 1.08% on the day on March 28, 2013.

Lumber Liquidators represents the strongest holding in my Covestor "Growth and Momentum" model. (This model was formerly called "Buy and Hold Value" but was renamed to reflect the underlying strategy more accurately.) I first purchased shares of Lumber Liquidators (LL on June 26, 2012 at a cost of $32.46 and subsequently took some profits by selling a few shares on September 11, 2012 at $48.13 and again sold a few shares at $65.25 on March 8, 2013. Lumber Liquidators (LL) closed at $770.22, up $.75 or 1.08% on the day on March 28, 2013.

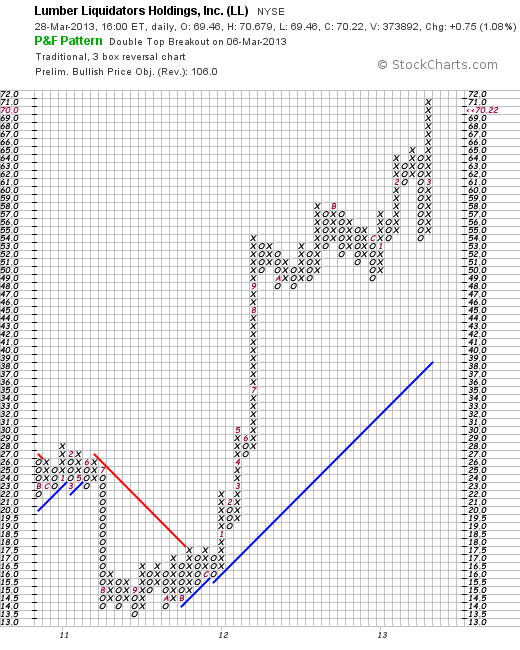

Examining the 'point & figure' chart on LL from StockCharts.com, we can see the initial sell-off in shares from $24 in July, 2011, to a low of $13.50 in October, 2011. The stock took off in December, 2012, spiking to $53/share in September, 2012 and has steadily built on that climb since that time.

According to the Yahoo "Profile" on Lumber Liquidators (LL), the company

"...operates as a specialty retailer of hardwood flooring, and hardwood flooring enhancements and accessories. The company provides various wood flooring products, including prefinished domestic and exotic hardwoods,  engineered hardwoods, unfinished hardwoods, bamboo, cork, and laminates, as well as resilient flooring products. It also offers flooring enhancements and installation accessories comprising moldings, and noise-reducing underlays and tools. The company markets its products to homeowners or to contractors under the brand name of Bellawood through its integrated sales channels, such as stores, a call center, and a catalog, as well as through its Website, lumberliquidators.com. As of December 31, 2012, it operated 279 retail stores in the United States; and 9 retail stores in Ontario, Canada."

engineered hardwoods, unfinished hardwoods, bamboo, cork, and laminates, as well as resilient flooring products. It also offers flooring enhancements and installation accessories comprising moldings, and noise-reducing underlays and tools. The company markets its products to homeowners or to contractors under the brand name of Bellawood through its integrated sales channels, such as stores, a call center, and a catalog, as well as through its Website, lumberliquidators.com. As of December 31, 2012, it operated 279 retail stores in the United States; and 9 retail stores in Ontario, Canada."

After a long period of weakness, the real estate market in America is starting to rebound and recent housing starts reports are encouraging. Companies that are involved in housing construction and renovation appear to be 'on a roll' and these include stocks like Home Depot (HD) and Beacon Roofing (BECN) among others that have shown tremendous price strength. I do not currently own shares of HD or BECN.

On February 20, 2013, Lumber Liquidators announced earnings for the quarter ended December 31, 2012. As the Motley Fool site reported, the company reported revenue of $210.7 million, beating expectations of $197.4 million. These sales were up by 21% over the prior-year same quarter result of $174.5 million.

Earnings came in at $.50/share and were also easily ahead of expectations of $.43/share. The GAAP earnings of $.50 were also ahead of the prior year's results of $.30/share by 67%. Certainly strong growth in financial results that are also ahead of what analysts are expecting are a good sign from my perspective for a stock that might be appreciating in price going forward to 'adjust' for the new financial results. And the stock did exactly that!

Reviewing the Morningstar.com '5-Yr Financials' on Lumber Liquidators (LL), we can see that the company has been steadily growing revenue results from $482 million in 2008 to $813 million in 2012. Earnings during this period have grown nicely from $.82/share in 2008 to $1.68/share in 2012, although growth in earnings was relatively stagnant between 2009 and 2011. Outstanding shares have been very stable with 27 million fully diluted shares according to Morningstar in 2008 and and increase to 28 million by 2012.

Looking briefly at the Morningstar-provided balance sheet reveals the company with $288 million in total current assets balanced against $101 of total current liabilities yielding a current ratio of 2.85. From my perspective a current ratio of over 1.0 is adequate and over 2.0 quite 'healthy' in terms of the ability to meet current cash needs to pay liabilities.

Morningstar reports that free cash flow has also been improving recently with $2 million reported in 2008, dipping to $(4) million in 2010 and then improving to $27 million in 2011 and $34 million in 2012.

Financially, the latest 'good results' reported in the latest quarter do not appear to be an unusual or exceptional development. The company has been doing a good job growing revenue and earnings, free cash flow, and maintaining a healthy balance sheet.

In terms of valuation, we can see from the Yahoo "Key Statitstics" on Lumber Liquidators (LL) that with a market capitalization of $1.91 billion, this is a small cap stock. (For comparison, we can see that Home Depot (HD) has a market cap of $103.2 billion, more than 50x the size of Lumber Liquidators).

Lumber Liquidators (LL) has a trailing p/e that is certainly 'rich' at 41.80 and even with the rapid growth expected, the forward P/E (fye Dec 31, 2014) still comes in at 27.01. Thus the PEG works out to a fairly rich 2.18. (I generally prefer to pay up to a PEG of 1.5 for a stock.)

Yahoo reports that there are 27.16 million shares outstanding with 25.84 million that float. As of February 28, 2013, there were 4.17 million shares out short representing a short interest ratio of 5.4 days of average trading volume, ahead of my own '3 day rule' for significance. A large short interest ratio may be a bullish indicator if the company actually reports an unexpected piece of good news forcing the short sellers to buy shares in a 'squeeze'.

The company does not pay a dividend and no stock splits are reported on Yahoo.

To summarize, the American economy has been in a 'funk' for several years since the financial crisis of 2008. With Congress in a stalemate unable toact to provide a fiscal stimulus, Ben Bernanke and the Federal Reserve have been utilizing quantitative easing and associated monetary policy to keep interest rates low and encourage economic activity. With economic weakness and an accomodative Federal Reserve, rates have stayed low and one of the key beneficiaries of this policy has been the housing market which indeed is starting to come alive.

Lumber Liquidators (LL) is sitting in the middle of this rebound and is a company and a stock that has been helped by the real estate mini-boom developing.

Thank you for visiting my blog! If you have any comments or questions, please feel free to leave them right here!

Yours in investing,

Bob

Posted by bobsadviceforstocks at 2:43 PM CDT

|

Post Comment |

Permalink

Updated: Saturday, 30 March 2013 2:45 PM CDT

Sunday, 24 March 2013

Valeant Pharmaceuticals International, Inc. (VRX)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Valeant Pharmaceuticals (VRX) is a holding of mine in the Covestor "Sustained Momentum" model. In fact, it is the strongest performing stock withing that eleven stock model. On December 27, 2011, I purchased shares of Valeant (VRX) at a cost of $46.93/share in this account. VRX closed at $73.97/share, up $1.11 or 1.52% on the day on March 22, 2013.

Valeant Pharmaceuticals (VRX) is a holding of mine in the Covestor "Sustained Momentum" model. In fact, it is the strongest performing stock withing that eleven stock model. On December 27, 2011, I purchased shares of Valeant (VRX) at a cost of $46.93/share in this account. VRX closed at $73.97/share, up $1.11 or 1.52% on the day on March 22, 2013.

My "Sustained Momentum" Model is based on my Marketocracy "RMF Fund" that is a simulated fund that I have been 'managing' since 2004. Valeant is the number one holding in that simulation having appreciated 135.16% since being included in that stock market game model. I have literally used my stock market simulation portfolio to build a real portfolio on Covestor. I currently am populating my "Sustained Momentum" model on Covestor with the top eleven of my Marketocracy holdings.

Let's take a closer look at Valeant (VRX) which has led the Sustained Momentum Model to a strong performance since inception.

According to the Yahoo "Profile" on Valeant (VRX), the company

"...develops, manufactures, and markets pharmaceutical products and medical devices in the areas of neurology, dermatology, and branded generics. It offers dermatology products, such as Zovirax Ointment, Xerese, Retin-A Micro, Elidel, Carac, Acanya gel, Sculptra and Sculptra Aesthetic, Atralin, Solodyn, Zyclara, Ziana, Vanos, Restylane family of products, and Dysport; over-the-counter (OTC) products, including CeraVe and  AcneFree; dentistry products, such as Arestin and Teeth Whitening System; ophthalmology products, including Timoptic, Timoptic, Macugen, and Visudyne; and neurology and other products, such as Wellbutrin XL and Xenazine in the United States. The company also provides pharmaceutical products, including Tiazac XC, Wellbutrin XL, Zovirax, Benzaclin, and Penlac; and Cold-FX, an OTC product in Canada, as well as Duromine/Metermine, Difflam, Duro-Tuss, and Rikodeine in Australia. In addition, it offers a range of treatments, including antibiotics, treatments for cardiovascular and neurological diseases, dermatological products, and diabetic therapies, as well as a range of various OTC products in Europe; and products for a range of therapeutic classes, including vitamin deficiency, antibacterials, and dermatology in Mexico and Brazil. Further, the company provides Duromine, Andolex, and Pholtex products in South Africa; and Difflam, Duro-Tuss, Tambocor, and Norgesic in Asia."

AcneFree; dentistry products, such as Arestin and Teeth Whitening System; ophthalmology products, including Timoptic, Timoptic, Macugen, and Visudyne; and neurology and other products, such as Wellbutrin XL and Xenazine in the United States. The company also provides pharmaceutical products, including Tiazac XC, Wellbutrin XL, Zovirax, Benzaclin, and Penlac; and Cold-FX, an OTC product in Canada, as well as Duromine/Metermine, Difflam, Duro-Tuss, and Rikodeine in Australia. In addition, it offers a range of treatments, including antibiotics, treatments for cardiovascular and neurological diseases, dermatological products, and diabetic therapies, as well as a range of various OTC products in Europe; and products for a range of therapeutic classes, including vitamin deficiency, antibacterials, and dermatology in Mexico and Brazil. Further, the company provides Duromine, Andolex, and Pholtex products in South Africa; and Difflam, Duro-Tuss, Tambocor, and Norgesic in Asia."

The history of Valeant (VRX) dates back to the 1990's when its forerunner company ICN Pharmaceuticals was in business, founded by Milan Panic. In 2002 ICN changed its name to Valeant Pharmaceuticas (VRX). Since that time Valeant has acquired other pharmaceutical companies including Tecnofarma in 2009, Aton Pharma in 2010, Vital Science Corp. in 2010, and Instituto Branded Generics in Brazil in 2010. Other acquisitions included iNova, Dermik, Sanitas Group, Dermik, and PharmaSwiss S.A. in 2011, Medicis Pharma, OraPharma, Pedinol, Natur Produkt in Russia, and Probiotica in Brazil in 2012. More recently, on March 21, 2013, Zacks reported on Valeant's acquisition of Obagi Medical Products, Inc. (OMPI) for $19.75/share. The Obagi acquisition should be accretive to earnings according to Valeant, and adds to the company's dermatologic products.

Valeant reported fourth quarter 2012 results on March 1, 2013. According to Zacks, the $1.21/share reported came in shy of estimates of $1.25/share but still represented a very strong growth from the $.90/share reported the prior year same period. Revenue for the quarter came in at $986 million, up 43% from the prior year. This was due to 'higher product sales' and beat the Zacks estimate of $959 million. For the full year of 2012, revenues came in at $3.55 billion, up 44% from the prior year and beat consensus estimates of $3.51 million. Earnings for the year of $4.42/share were shy of the Zacks Consensus Estimate of $4.47 but still were 61.9% (!) higher than the prior year.

Valeant reaffirmed strong sales guidance of $4.4 to $4.8 billion in revenue for 2013 representing a 30% increase and earnings per share are projected to come in between $5.45 to $5.75/share.

Reviewing the Morningstar.com "5 Years Financials" on Valeant (VRX), we can see that revenue has grown strongly with $757 million reported in 2008, increasing to $3.55 billion by 2012. Diluted earnings per share have actually dipped from $1.25/share reported in 2008 to a loss of $(.38)/share in 2012. Diluted shares have grown from 160 million in 2008 to a peak of 326 million in 2011 before dipping slightly to 305 million in 2012.

The Morningstar site reports that VRX has $2.78 billion in current assets as of the close of 2012, with $1.8 billion of current liabilities generating a current ratio statistic of 1.5 still quite healthy from my perspective. The company has improved its free cash flow from $182 million in 2008 to $475 million in 2012.

In terms of valuation, looking at the Yahoo "Key Statistics" on Valeant, we can see that this company is a large cap stock with a market capitalization of $22.6 billion. With losses reported there is no P/E or PEG to analyze. There are currently 305.76 million shares outstanding and 268.51 million that float. There are 6.52 shares out short as of 2/28/13, representing a short interest ratio of 5.9 days. (This is significant from my perspective as I arbitrarily use 3 days as a cut-off.) No dividends are paid and the last stock split was in October, 2000.

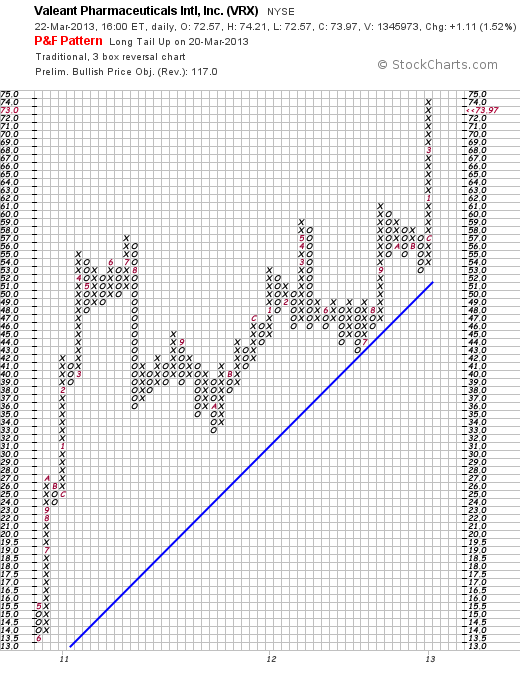

Probably one of the most impressive parts of this particular investment is the price chart of this stock! Looking at the 'point & figure' chart on Valeant (VRX) from StockCharts.com, we can see the price climbing sharply from a low of $13.50 in June, 2010, to a high of $56 in July, 2011, before3 slipping back to consolidate in the $35 range in October, 2011, before once again starting to climb to its current level of $73.97. If anything the price appears technically a bit over-extended but still a very strong chart from my amateur perspective.

To summarize, Valeant (VRX) has been assembled over the past 10-15 years from a variety of pharmaceutical companies including the former ICN Pharma and Biovail corporations. Management has done what appears to be a superb job of fitting these pieces together and they have grown revenue and earnings (at least adjusted earnings) at an impressive pace. They do not appear to be done adding the pieces to this puzzle but the picture they have been creating has been a good one, at least thus far, for this investor!

Thank you very much for stopping by and visiting my blog! If you have any questions or comments please feel free to leave them here on this website.

Yours in investing,

Bob

Saturday, 16 March 2013

CareFusion (CFN)

Hello Friends! Thanks so much for stopping by and visiting my blog Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

On February 1, 2013, I purchased shares of CareFusion (CFN) at a cost of $31.43 for my Healthcare Covestor Model. CareFusion closed at $34.31 on March 15, 2013, so thus far it has been a good move. Let's take a look 'under the hood' on this stock and see if it makes sense for this blog and for my own portfolio.

On February 1, 2013, I purchased shares of CareFusion (CFN) at a cost of $31.43 for my Healthcare Covestor Model. CareFusion closed at $34.31 on March 15, 2013, so thus far it has been a good move. Let's take a look 'under the hood' on this stock and see if it makes sense for this blog and for my own portfolio.

First of all, according to the Yahoo "Profile" on CFN, the company

"... operates in two segments, Medical Systems and Procedural Solutions. The Medical Systems segment develops, manufactures, and markets capital equipment and related supplies for medication management. It offers IV medication safety and infusion therapy  delivery systems, including dedicated disposables, software applications, and related patient monitoring equipment; automated dispensing machines and related applications for distributing and managing medication and medical supplies; and respiratory ventilation equipment and dedicated circuits for respiratory therapy, as well as develops data mining surveillance software that enables hospitals to identify adverse drug events and healthcare associated infections. This segment provides its products under the Alaris, Pyxis, Rowa, AVEA, Vela, and LTV Series brands. The Procedural Solutions segment develops, manufactures, and markets single-use skin antiseptic products and other patient-preparation products; hair-removal and skin-care products, and non-dedicated disposable IV infusion administration sets and accessories; surgical instruments; interventional specialty products, such as diagnostic trays and biopsy needles, drainage catheters, and vertebral augmentation products; and non-dedicated disposable ventilator circuits and oxygen masks used for providing respiratory therapy."

delivery systems, including dedicated disposables, software applications, and related patient monitoring equipment; automated dispensing machines and related applications for distributing and managing medication and medical supplies; and respiratory ventilation equipment and dedicated circuits for respiratory therapy, as well as develops data mining surveillance software that enables hospitals to identify adverse drug events and healthcare associated infections. This segment provides its products under the Alaris, Pyxis, Rowa, AVEA, Vela, and LTV Series brands. The Procedural Solutions segment develops, manufactures, and markets single-use skin antiseptic products and other patient-preparation products; hair-removal and skin-care products, and non-dedicated disposable IV infusion administration sets and accessories; surgical instruments; interventional specialty products, such as diagnostic trays and biopsy needles, drainage catheters, and vertebral augmentation products; and non-dedicated disposable ventilator circuits and oxygen masks used for providing respiratory therapy."

In other words, this company supplies hospital and medical clinics supplies for delivery of pharmaceuticals and patient care.

Let's take a look at their latest quarterly results. On February 7, 2013 CareFusion (CFN) reported their 2nd quarter results. Revenue for the second quarter came in $909 million, up 2% from the $890 million reported the prior year same period. Operating income grew 20% to $171 million from the $143 million reported the prior year. Income from continuing operatings came in at $108 million or $.48/share. The 'adjusted income' from continuing operatings increased 9% to $121 million or $.54/diluted share. These are reasonably good results but what about longer-term?

Reviewing the Morningstar.com "5-Yr Financials" on CFN, we can see that revenue has actually decreased from $4.5 billion in 2008 to $3.5 billion in 2011, and now has started increasing to $3.6 billion in 2012 and $3.62 billion in the trailing twelve months (TTM). Diluted earnings/share however, have shown strong growth with $.87/share reported in 2007 increasing strongly to $1.30/share in 2012 and $1.42/share in the TTM. Outstanding shares have been stable with 223 million shares outstanding in 2010 and 225 million shares in the TTM. Thus while revenue has decreased over the last 5 years, the company has been becoming more profitable with rapidly increasing earnings while revenue has been turning around as well.

In terms of their 'balance sheet', the Morningstar.com site shows that the company has $3.1 billion in total current assets as opposed to $933 million in total current liabilities yielding a current ratio of over 3.0. The company appears to be quite solvent.

Morningstar.com reports that the CareFusion's free cash flow has ranged from $563 million in 2010, dipped to $177 million in 2011, and increased back to $545 million in 2012.

In terms of valuation, this company is a mid cap stock with a market capitalization of $7.64 billion according to the Yahoo"Key Statistics" on CFN. The trailing p/e is a moderate 24.01, the forward p/e (fye June 30, 2014) is estimated at 14.18, yielding a reasonable PEG of 1.41. Yahoo reports 222.59 million shares outstanding with 222.04 million that float. As of February 28, 2013 there were 2.21 million shares out short yielding a relatively insignificant (from my perspective) short interest ratio of 1.10. The company does not pay a dividend and there is no record of a stock split on Yahoo.

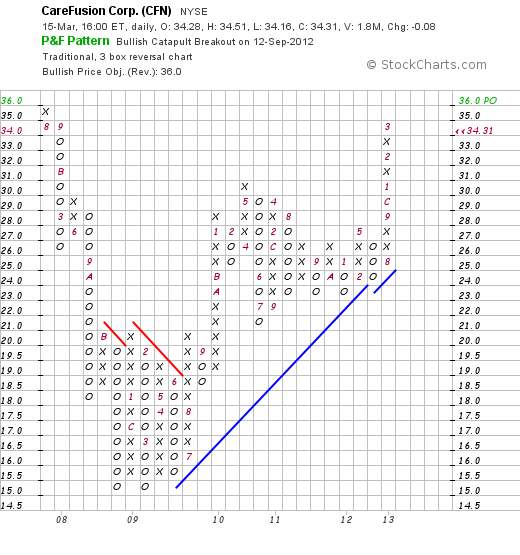

And how has the stock price been doing? Examining the 'Point and Figure' chart on CFN from StockCharts.com, we can see that the stock experienced a sharp decline from $35 in July, 2007 to a low of $15 in March, 2009. Since that low, the stock has moved higher, consolidating at around $25 between Novembe, 2009, until August, 2012. More recently the stock has been moving higher heading back towards the $35 range.

CareFusion (CFN) has been enjoying a strong stock performance as part of a very strong Healthcare Sector. Thus far the stock has been performing well within my own portfolio and hopefully the stock's momentum both technically and fundamentally will lead the stock price higher in the future.

Thanks so much for stopping by and visiting my blog! If you have any comments or questions, please leave them here.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 4:57 PM CDT

|

Post Comment |

Permalink

Updated: Saturday, 16 March 2013 5:33 PM CDT

Friday, 4 January 2013

FleetCor Technologies (FLT)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I would like to apologize to my friends and readers for my long hiatus here on this blog. I am definitely an amateur blogger and know that successful blogging requires a consistent post or two. If I can make this a New Year's resolution.... That being said, I wish all of you a happy and healthy 2013.

One of the strongest holdings in my Covestor 'Buy and Hold' Value model is my position in FleetCor (FLT). I purchased shares of FLT on September 12, 2012 at a price of $44/share. Today (1/4/13) FleetCor is trading at $55.05, up $.16 or .29% on the day. Let's take a closer look at this investment and try to understand what it does, how it's doing, and what kind of valuation this stock price represents.

One of the strongest holdings in my Covestor 'Buy and Hold' Value model is my position in FleetCor (FLT). I purchased shares of FLT on September 12, 2012 at a price of $44/share. Today (1/4/13) FleetCor is trading at $55.05, up $.16 or .29% on the day. Let's take a closer look at this investment and try to understand what it does, how it's doing, and what kind of valuation this stock price represents.

According to the Yahoo "Profile" on FleetCor, the company...

"...provides specialized payment products and services to businesses, commercial fleets, oil companies, petroleum marketers, and government entities in North America, Europe, South Africa, and Asia. It sells a range of customized fleet and lodging payment programs; and offers various card products to purchase fuel, lodging, and related products and services at participating locations. The company also offers prepaid fuel and food vouchers and cards, as well as a telematics solution that enables fleet operators to monitor the capacity utilization and movement of vehicles and drivers."

First of all let's take a look at the latest quarter. Zacks reported on their 3rd quarter results on November 9, 2012. Revenues for the quarter came in at $186.9 million, up 32% over the prior year same quarter. Revenue growth largely was due to international results which climbed 107.3% year over year, and moderate growth domestically, up 9.1% year over year.

Adjusted earnings came in at $.83/share, up 48% from $.56/share the prior year and exceeding the Zacks Consensus Estimate by 20.1%. The company also raised revenue guidance for 2012 to $678-$682 million from prior guidance fo $665-$675 million.

In terms of longer-term results, reviewing the Morningstar.com '5 Years Financials', we can see that revenue has grown steadily from $341 million in 2008 to $520 million in 2011 and to $645 million in the trailing twelve months (TTM). Net income has improved from, $97 million in 2008 to $147 million in 2011 and $194 million in the TTM. On a diluted earnings per share basis, Morningstar reports FLT reported $1.34/share in 2010, $1.76 in 2011, and $2.27/share in the TTM. Outstanding shares were 81 million in 2010 and have grown slightly to 85 million in the TTM.

Looking briefly at their balance sheet on Morningstar, we can see that the company as of December 2011, had $1,123 million in total current assets compared to $1,122 in total current liabilities giving it a current ratio of just over 1.0.

Free cash flow has improved from $52 million in 2008 to $266 million in 2011 and dipped to $224 million in the TTM.

Looking at Yahoo "Key Statistics" for some valuation numbers, we can see that this is a Mid Cap Stock with a market capitalization of $4.65 billion. The company sports a moderate trailing P/E of 24.22 and a forward P/E of 16.62. With rapid growth estimated the PEG Ratio (5 yr expected) comes in very reasonably at 1.15. Yahoo reports the company with 84.53 million shares outstanding with only 56.62 million that float. There are 1.84 million shares out short as of 12/14/12, resulting in a 'Short Ratio' of 2.20, under my own arbitrary 3 day level for significance. The company does not pay a dividend.

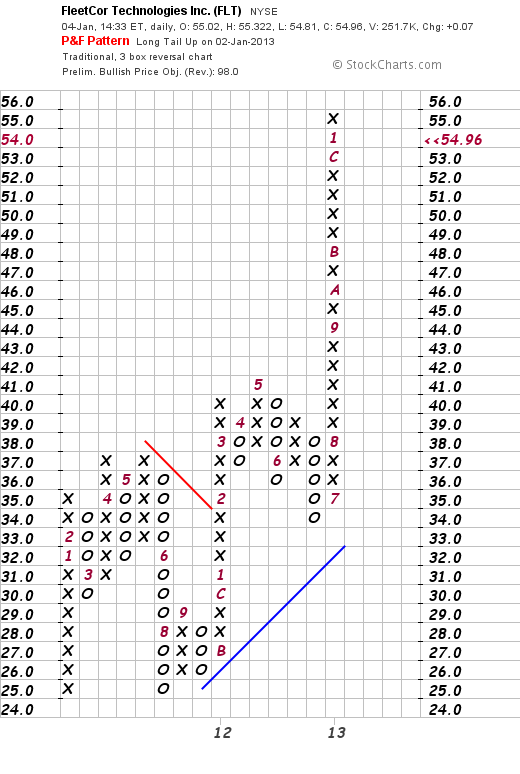

In terms of technical strength, looking at the StockCharts 'Point & Figure' chart on FLT, we can see that FleetCor (FLT) which has a trading record since 2011, has fairly steadily increased its price from $25 to its current level of $55 where if anything it appears a bit over-extended short-term.

As the economy rebounds from the recession, the trucking industry is also rebounding. Recently, one of my favorite sources for new ideas for stocks has been the Monday Edition of the IBD which lists the Investor's Business Daily top 50 stocks. Not every stock on that list meets my own requirements for inclusion. However, FleetCor (FLT) has been an IBD 50 favorite for some time and the underlying strong earnings growth and revenue record, reasonable valuation, and strong technicals along with sitting in a rebounding industry make it very attractive.

Thank you for your continued interest and loyal readership. If you have any questions or comments, please feel free to leave them right here.

Yours in investing,

Bob

Wednesday, 19 September 2012

Barrett Business Services Inc. (BBSI)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Earlier today I purchased shares of Barrett Business Services (BBSI) at an average cost of $27.96/share for my Covestor Buy and Hold Value model. BBSI closed today at $27.88, up $.35 or 1.27% on the day. Let's take a closer look at this stock.

Earlier today I purchased shares of Barrett Business Services (BBSI) at an average cost of $27.96/share for my Covestor Buy and Hold Value model. BBSI closed today at $27.88, up $.35 or 1.27% on the day. Let's take a closer look at this stock.

According to the Yahoo "Profile" on Barrett, the company

"...offers human resource management services in areas comprising payroll processing, employee benefits and administration, human resource management, risk management, and workers’ compensation coverage areas. It also provides professional employer organization services, which include employee benefits, health insurance, workers’ compensation coverage, workplace safety programs, federal and state employment laws compliance, labor and workplace regulatory requirements, and related administrative services; and payroll administrative services, such as payroll processing, payroll taxes, and human resource consulting services. In addition, the company provides staffing services, including on-demand or short-term staffing assignments, contract staffing, long-term or indefinite-term on-site management, direct placement, and human resource administration services."

On July 24, 2012, Barrett Business Services announced results for the second quarter ended June 30, 2012. Revenue for the quarter grew 26% to $95.5 million compared to $76.0 million the prior quarter. Net income was $3.7 million or $.53/diluted share compared to $3.4 million or $.34/diluted share the prior year.

A couple of articles on Barrett caught my eye. Certainly growing dividends is an attractive feature in this low-interest-rate environment. Here is a chart on the steadily increasing, although still somewhat small, dividend that Barrett has been paying:

In addition, Zacks gave Barrett a nice plug this week ranking it a "Buy". Zacks pointed out that the second quarter report that I reported above represented

"...an impressive record of outperforming quarterly earnings expectations, which it continued in its second quarter report with a surprise of more than 20%."

Zacks goes on to point out that Barrett is expected to grow its earnings at a 22% rate going forward for the next 5 years ahead of the 11.6% growth rate of similar companies in the same industry. In addition the company and analysts have been raising guidance.

Looking at some longer-term results from Morningstar.com, we can see that revenue for this company actually dipped from $289 million in 2007 to a low of $236 milion before resuming stronger growth with $273 million in 2010, $315 million in 2011 and $348 million in revenue for the trailing twelve months (TTM).

Diluted earnings/share have followed the revenue pattern dipping from $1.44/share in 2007 to a loss of $(.46)/share in 2009 before turning higher to $.71/share in 2010 and $1.41 in 2011. Morningstar does report that earnings did come in a bit lower at $.74/share in the TTM. The company has been buying back shares and reported 12 million shares in 2007 dipping to 10 million in 2009 and 9 million in the TTM.

In terms of free cash flow, the company reported $13 million in 2007, dipped to $2 million in 2009, then since then reported $16 million in 2010 and $30 million in 2011 and the TTM.

Briefly looking at the Morningstar.com balance sheet we can see that Barrett has $129 million in total current assets vs. $79 million in total current liabilities yielding a current ratio of 1.63.

Looking at Yahoo "Key Statistics" on BBSI, we can see that this is actually a 'micro cap' stock with a market capitalization of only $195.24 milion. The trailing p/e is rich at 37.93, but the forward p/e is 15.40 due to the rapid growth in earnings anticipated. Thus with the quick growth, the PEG ratio comes in at a very reasonable 0.84.

Yahoo reports shares outstanding of only 7 million with 6.79 million that float. Currently there are 182,440 shares out short resulting in a short interest ratio of 6.40, ahead of my own arbitrary '3 day rule' for significance.

Currently the company pays a forward dividend rate of $.44/share with an indicated yield of 1.60%. The payout ratio is 49% suggesting adequate earnings coverage for continuing and increasing the dividend if the estimated earnings growth continues.

The company last split its shares with a 3:2 split back in May, 2005.

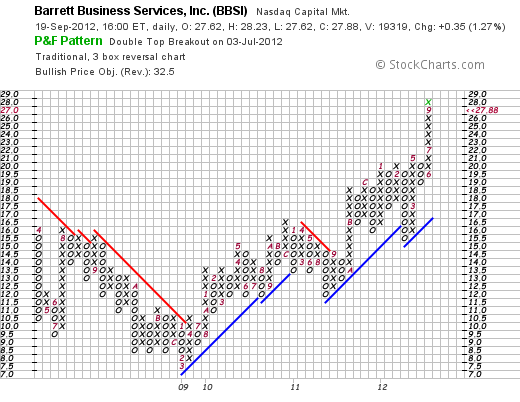

Let's take a look at the 'point & figure' chart on BBSI from StockCharts.com:

We can see that the chart demonstrates the same weakness in the stock price that followed the downturn of business into 2009 and the rebound in earnings and revenue growth resulted in the strong rebound in the stock price. Certainly the chart looks very strong if not a big over-extended at the moment.

To summarize, BBSI is a recent purchase of mine. The earnings, the revenue growth, the free cash flow, the valuation, the technicals all look encouraging. And the company is reducing outstanding shares as well. Unfortunately, the company is very small and is likely to experience additional volatility that a reduced float may result and investors both pile in and pile out of a company on varying news. The earnings report is likely very soon for the third quarter and hopefully will see this stock continue to move higher.

Thank you again for stopping by! I have been away a little longer than usual from this blog, but I hope this entry will not be an isolated event but continued posting from me on this site. As always, please feel free to leave your comments right here on the blog. I shall try to remove those comments that are just links to individuals promoting their own websites. I know how that works.

Yours in investing,

Bob

Saturday, 28 April 2012

Writing Articles on Seeking Alpha

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

For several years now I have had a close relationship with the Seeking Alpha website. David Jackson started this brilliant website back in 2004, shortly after this own website was started. Many of the entries here have been picked up by Seeking Alpha and have been reposted on their page where further distribution occurs including on Yahoo Finance and elsewhere.

This past week I have written a few articles directly on Seeking Alpha that I wished to make sure you were aware of as they may be of interest you if you enjoy my own approach to looking at investing. I wrote about Warren Buffet's Cancer and what that meant for him and for his Berkshire Hathaway as well as for stocks like Varian (VAR), Theragenics (TGX) and Intuitive Surgical (ISRG). It is an interesting read and hopefully may give you some insight on the disease as well as investments that are related to the treatment. Full disclosure, I own some shares of ISRG in my Covestor Healthcare Model.

Prior to the earnings announcement, I took a look at Merck (MRK). I do not have any stock in Merck at this time, but wrote up my thoughts of the company and actually while the company did end up exceeding expectations on earnings, still had some issues with underlying revenue growth. Sometimes growth stocks evolve into dividend and income stocks and there is nothing wrong with that. But it isn't my own particular 'cup of tea'. Or should I say medicine.

Finally I wrote a small review of Nordstrom (JWN). I own shares in my new Covestor model called 'Sustained Momentum'. (I need to do a separate blog entry all about that model in the near future.) My own personal purchase of this stock was about as Peter Lynch as I have ever gotten :). It's a great stock and it has been on a tear recently.

In my own mind, I would like this blog to be a bit looser and more casual. Sort of Jeans and a Tee-shirt I guess. Like my own article on my stock club, which wasn't particularly an analysis as it was a sharing of my own life with you the reader, that's where I would like this blog to go. I don't want to worry about spelling, grammar, even being politically correct. I do want to be able to even share political ideas that are important to me as well. I might even lose some of my readers here.

I shall do analyses here also, but shall be writing more over at Seeking Alpha. I seem to have a larger audience in that location. As you can see, even at 57 my life and my blog is still a work in process.

Thank you so much for visiting and supporting my own interest in investing and sharing ideas and perspectives.

Yours in investing,

Bob

Sunday, 15 April 2012

McKesson (MCK)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

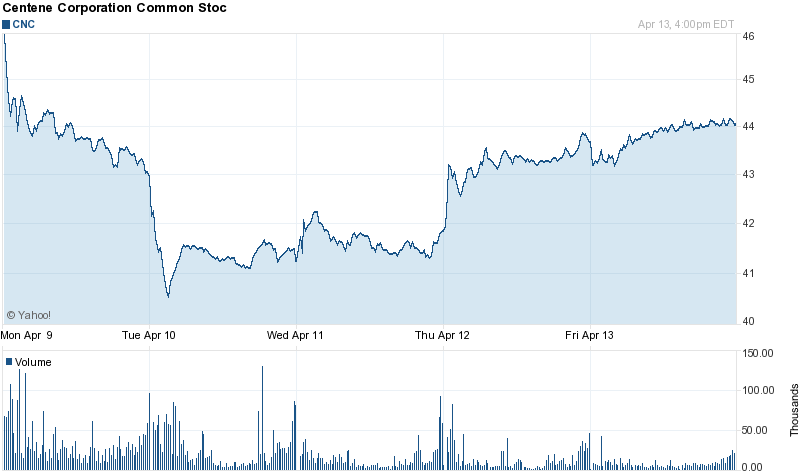

I wanted to share with you what I call a 'swap' in my Covestor Healthcare Model last week. Centene (CNC) shares swooned last week after they lost a contract for the Ohio Department of Job and Family Services. I sold my shares at $43.49 and the stock already has bounced back to a slightly higher level!

I cannot deny that I have a little seller's remorse, but I have also noticed that stocks after a sharp decline often have a bounce higher, but way once again move lower into the future.

Anyhow, I picked up some shares of McKesson (MCK) with the proceeds. One of the first times I reviewed McKesson was back on January 1, 2004, literally over 8 years ago right here on this blog! (The years have really flown by here!)

Anyhow, I picked up some shares of McKesson (MCK) with the proceeds. One of the first times I reviewed McKesson was back on January 1, 2004, literally over 8 years ago right here on this blog! (The years have really flown by here!)

At that time the stock was trading at $32.16. MCK closed at $90.48 on 4/13/12, so the stock really has done very well since that post.

Let's take a closer look at MCK and let's see if it is still was wise to pick up shares now that the stock has nearly tripled in price since I first visited it!

According to the Yahoo "Profile" on McKesson, the company

"...delivers medicines, pharmaceutical supplies, information, and care management products and services for the healthcare industry."

"...delivers medicines, pharmaceutical supplies, information, and care management products and services for the healthcare industry."

Unlike Centene (CNC) which suffered from a loss of a contract, McKesson (MCK) has been strong recently due to a continuance of a contract with the Department of Veteran affairs (VA).

In terms of its latest quarter, McKesson reported their 3rd fiscal quarter (ended December 31, 2011) on January 30, 2012. As Motley Fool pointed out on January 31, 2012, they had strong results with revenue growth of 9.2% coming in at $30.84 billion ahead of last year's $28.20 billion and exceeding analysts' expectations of $30.19 billion.

The company reported earnings of $1.40 ahead of estimates of $1.38 on same basis. GAAP earnings of $1.20 were 100% higher than the prior year's $.60/share result.

In terms of longer-term results, reviewing the Morningstar.com "Financials" on McKesson, we can see that revenue has steadily grown from $93.0 billion in 2007 to $112.1 billion in 2011 and $119.9 billion in the trailing twelve months (TTM). Earnings have grown but somewhat less consistently from $2.99/share in 2007 to $4.57 in 2011 and $5.13/share in the TTM.

The company has been retiring shares through buybacks with 305 million shares outstanding in 2007, 263 million shares in 2011 and 254 million in the TTM. The company announced another $650 million in stock repurchases on January 31, 2012.

Morningstar reports McKesson with $22.4 billion in current assets and $18.7 billion in current liabilities for a current ratio of 1.20. The company has also grown its free cash flow which has increased from $1.2 billion in 2007 to $2.0 billion in 2011 and $2.3 billion in the trailing twelve months.

Examining the valuation of the stock, we can see from the Yahoo "Key Statistics" page, that McKesson is a large cap stock with a market capitalization of $22.27 billion.

The trailing P/E is reported at 17.64 with a forward P/E of 12.57. With solid growth expected the PEG Ratio (5 yr expected ) works out to a very reasonable 0.95 indicating reasonable valuation.

Yahoo reports 246.10 million shares outstanding with 245.30 million that float. As of March 30, 2012, there were 1.88 million shares out short with a very modest short interest ratio of 1.00 (well below my own arbitrary 3 day rule for significance).

McKesson pays a modest dividend with a forward dividend yield of 0.90%. The company last split its stock in January, 1998, when it declared a 2:1 stock split.

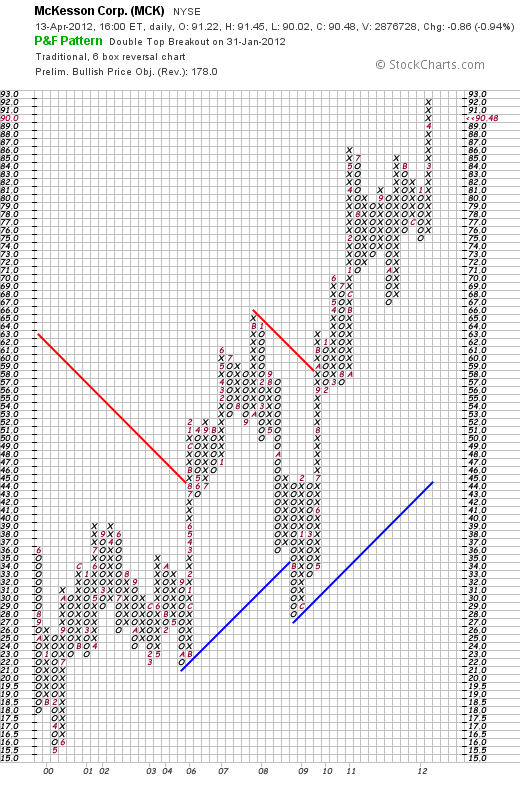

McKesson is a solid stock for my portfolio and belongs in this blog. Summarizing a few findings here, the stock recently reported a renewal of a very significant pharmaceutical contract with the Veterans Administration, the latest quarterly report was strong with growth in revenue and earnings that both exceeded expectations. Technically the stock has a strong chart going back for at least eight years. They have steadily grown their revenue, earnings (not quite as steady), and grown their free cash flow the past five years. Meanwhile they have bought back shares reducing the float and increasing shareholder value while maintaining a dividend and a strong balance sheet. The stock is modestly priced and considering estimated growth, the PEG is under 1.0 which is not a common finding in the stocks that I review on this blog.

My hand isn't as steady when bad news derails one or more of my holdings. I am relatively quick to sell on this news and even though Centene (CNC) may turn out to be a terrific stock long term, it appears that McKesson (MCK) is also a good choice. I shall be keeping Centene on my 'watch list' and may well revisit this holding in the future!

Thanks again for visiting here. If you have any comments or questions, please feel free to leave them right here.

Yours in investing,

Bob

Newer | Latest | Older