Stock Picks Bob's Advice

Wednesday, 23 September 2009

McDonald's (MCD) and Walgreen (WAG) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

As one of my basic strategies for dealing with my investments and managing my cash and equity balances, I utilize predetermined sale points for all of my holdings both on the upside and downside after an initial purchase. Sales on appreciation are considered "good news" and generally result in a purchase of a new holding. This is contrasted with sales on the downside, which I refer to as "bad news" signals that result in a shift from equity into cash.

Earlier today my holding in Walgreen (WAG) reached a first appreciation target--a gain of 30% in stock price after an initial purchase and I sold 1/7th of my holding. I purchased 77 shares of Walgreen in my Trading Account on March 27, 2009, at a cost basis of $26.73/share. I sold 11 shares of Walgreen (WAG) today at $34.75 for a gain of $8.02 or 30% since purchase. Since I currently ownly hold 6 positions, well under my maximum of 20 holdings, this sale on "good news" generated a purchase signal for me, and I added a new position into my trading account.

Earlier today my holding in Walgreen (WAG) reached a first appreciation target--a gain of 30% in stock price after an initial purchase and I sold 1/7th of my holding. I purchased 77 shares of Walgreen in my Trading Account on March 27, 2009, at a cost basis of $26.73/share. I sold 11 shares of Walgreen (WAG) today at $34.75 for a gain of $8.02 or 30% since purchase. Since I currently ownly hold 6 positions, well under my maximum of 20 holdings, this sale on "good news" generated a purchase signal for me, and I added a new position into my trading account.

Recently I have been refining my purchases of positions trying to address the question of not only what and when to buy but to deal with the matter of 'how much'? This question became apparent when my portfolio, during the worst part of the correction, dipped to a minimum of 5 holdings. As these occasionally needed to be sold on losses, and yet reflecting my own desire to maintain a minimum of 5, I needed to address the problem of replacing losing holdings with similarly sized holdings in spite of their sale on 'bad news. Initially I chose to replace them with holdings 50% of the average of the other positions. Subsequently I have decided that 80% or 4/5 of the size of the remaining holdings made reasonable sense to me.

However, with a shrinking position size, conversely I needed some approach that would enable me to increase the size of these downsized holdings as the market improved so that new positions would be more 'normal' in value. Thus, I have chosen to add new holdings at a level of 125% of the value (5/4) of the other positions held in the portfolio. You can see that as a market firms, my new positions will continue to grow in size; when the market is very weak, my replacement holdings will diminish in value.

With my buy signal in hand, I chose to purchase 52 shares of McDonalds Corp (MCD) at a price of $56.18. I recently reviewed this company but would like to touch on some of the updated financial underpinnings to this decision. Unfortunately for me I purchased shares just before the Fed announced its decision to leave short-term interest rates unchanged at near zero, but commented that economic activity had "picked up" since the last Fed meeting in August. As should be expected, the skittish market understood good news to be bad news and sold off shares. Somehow, any comment that things had "picked up" was enough to convince an inflation bear that interest rates would be heading higher soon. Although there appears to be little in the announcement to justify that assessment.

With my buy signal in hand, I chose to purchase 52 shares of McDonalds Corp (MCD) at a price of $56.18. I recently reviewed this company but would like to touch on some of the updated financial underpinnings to this decision. Unfortunately for me I purchased shares just before the Fed announced its decision to leave short-term interest rates unchanged at near zero, but commented that economic activity had "picked up" since the last Fed meeting in August. As should be expected, the skittish market understood good news to be bad news and sold off shares. Somehow, any comment that things had "picked up" was enough to convince an inflation bear that interest rates would be heading higher soon. Although there appears to be little in the announcement to justify that assessment.

In any case, McDonald's (MCD) closed at $55.54, down $(.27) or (.48)% on the day, a bit under my own purchase price at $56.18.

Much has been written about McDonald's being "recession-resistant". We do know that the recession has hit upscale restaurants hard! Recently The Motley Fool labeled McDonald's as "recession-resistant". Intuitively, I view McDonald's as the high-quality, clean-store, good-value and consistent product offering that also represents comfort foods in this rather uncomfortable time of steep unemployment numbers and economic slowing.

But let's get back to McDonald's and why I like it as an investment.

The latest quarterly report came in July 23, 2009 as reported. The company's earnings actually dipped to $1.09 billion or $.98/share down from $1.19 billion or $1.04 billion in the year ago period. Revenue would have actually climbed 4% except for currency fluctuations. The company beat expectations of earnings of $.97/share (they reported $.98) but missed expectations on revenue of $5.7 billion (they reported $5.65 billion).

Interestingly, it was a strong dollar that led to adjustments in revenue. When local currency remains stable and the dollar soars, each unit of foreign currency means less dollars reported. If the converse is true, then global revenue should be increasing in the next report due to dollar weakness. Of course, I am not a currency expert, but it could make one wonder! In fact as this article noted:

"Stifel Nicolaus & Co. analyst Steve West told investors that the August results were worse than anticipated, but he expected further benefits in foreign exchange rates would help McDonald's overcome any weakness in the monthly metric."

However, the company continues to do well globally. These same-store sales results are reported in local currency, and represent consumer interest in the product. As reported:

"Same-store sales - or those at outlets open at least 13 months -- rose 4.8%, including a 3.5% rise in the U.S. Europe was up 6.9% and the Asia/Pacific, Middle East and Africa rose up 4.4%."

Longer-term, except for the recent dip in revenue, the "5-Yr Restated Financials" on Morningstar are impressive. Revenue has climbed from $19 billion in 2004 to $22.5 billion in the trailing twelve months (TTM). Earnings have increased from $1.79/share in 2004 to $3.77/share in the TTM. The company pays a nice dividend and has grown it from $.55/share in 2004 to $1.88/share in the TTM. The company appears to have a reasonable cushion on its dividends with a payout ratio of 50%.

Outstanding shares have been held steady with 1.27 billion in 2004, declining to 1.13 billion in the TTM. Free cash flow continues to be strongly positive with $2.6 billion in 2006 in creasing to $3.6 billion in the TTM.

The balance sheet appears reasonable with $3.6 billion in cash and other current assets compared with the $2.8 billion in current liabilities. The company does have significant long-term debt reported at $13.1 billion.

Checking the Yahoo "Key Statistics" we can see that this is a 'large cap' stock with a Market Capitalization of $60.61 billion. The trailing p/e is 14.72 and the p/e is moderate at 14.72. The PEG is a tad rich at 1.59.

There are 1.09 billion shares outstanding and only 10.28 million shares out short representing 1.3 trading days of volume (the short ratio). The company pays a forward dividend of $2.00/share yielding 3.6%. The last stock split was more than 10 years ago, a 2:1 split on March 8, 1999.

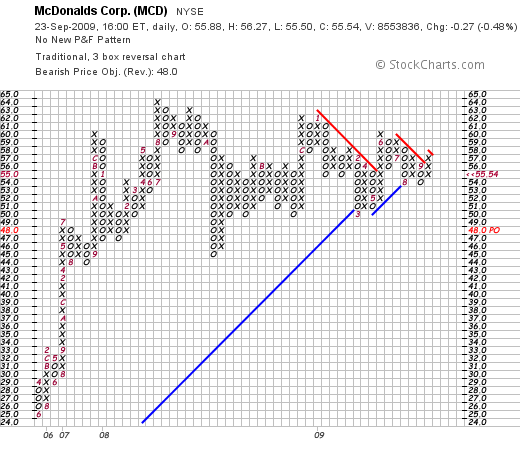

Taking a quick look at a 'point & figure' chart from StockCharts.com, we can see that the stock moved strongly higher from $25.00/share in June, 2005, to a high of $64 in August, 2008. Over the past year it has traded in a tight range between a low of $45 and $62. It appears to have found a new level of support and does not appear over-extended.

To summarize, my Walgreen shares hit a first partial sale point on the upside triggering a 'buy signal' in my own trading strategy. The small portion of Walgreen (WAG) was sold and a new position in McDonald's (MCD) was established at a slightly larger size than my other positions as was indicated.

I like McDonald's both from its well-established brand, its ability to innovate in a mature market, its reasonable valuation and its solid dividend. I believe we are still working ourselves out of a rather severe recession and that the value both in the stock and the product it sells will play out well for me. Now, if I can only avoid super-sizing any fries, I shall not have to worry about my ever-struggling diet :).

Thanks for stopping by! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Sunday, 20 September 2009

ResMed (RMD) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

One of my favorite stocks (that I do not currently own) is ResMed (RMD) a company that manufactures equipment that treats Obstructive Sleep Apnea. A very common disease that affects millions of people worldwide and that untreated can increase your risk of dying early by as much as 46%.

As this same report relates, sleep apnea

"...is closely linked with obesity, high blood pressure, heart failure and stroke"

Incredibly common, the same article found that

"Among men, 42.9 percent did not have sleep-disordered breathing, 33.2 percent had mild disease, 15.7 percent had moderate disease, and 8.2 percent had severe disease," they wrote.

They said about 25 percent of the women had mild sleep apnea, 8 percent had moderate disease and 3 percent had severely disordered breathing."

It is estimated that 20 to 30 million Americans have sleep apnea and it remains largely undiagnosed.

Now that I have you convinced that obstructive sleep apnea is a common and usually easily treatable disease with positive airway pressure masks, let's take a closer look at one of the dominant companies in this market, ResMed (RMD).

I say that ResMed (RMD) is an "old favorite" of mine, because I have written about this company several times, and my sentiment towards their business has remained positive. I first wrote about ResMed on December 5, 2003, when the stock was trading at a split-adjusted $20.88. (ResMed had a 2:1 stock split in October, 2005). I again revisited ResMed in February, 2005, when the stock was trading at a split adjusted $29.92. I also for a period became a holder in the stock myself.

In fact, on August 6, 2008 I purchased shares in ResMed (RMD) at $43.09 and wrote up a little more of my own rationale for doing so. I ended up selling those shares in October, 2008, as the stock market cratered. ResMed (RMD) closed at $45.52 on September 18, 2009, up $.25 or .55% on the day.

I am not yet convinced that the recession is over. But certainly there are early signs of recovery even as some states are seeing record levels of unemployment including California at 12.2% and Nevada at 13.2%. However, my own investment strategy is to monitor my own holdings, avoid making predictions about the economy or the stock market, and restrict my purchases to companies like ResMed with strong fundamentals.

On August 7, 2009, ResMed (RMD) reported 4th quarter 2009 results. Revenue for the quarter ended June 30, 2009, increased 7% to $252 million. (Growth would have been even stronger at 15% if adjustments for currency hadn't been made.)

Net income for the quarter increased 53% to $45.4 million or $.59/share. Analysts, as compiled by Thomson Reuters, had been expecting $.54 cents and only $243.2 million in revenue. Thus, as I like to see on an earnings report, the company reported rather robust growth in both revenue and earnings and beat expectations on both!

Using the Morningstar.com "5-Yr Restated" financials for a longer-term look, we can see that ResMed (RMD) has increased revenue steadily from $426 million in 2005 to $835 million in 2008 and $921 million in 2009. Earnings/share have grown from $.91/share in 2005 to $1.16 in 2006 before dipping to $.85/share in 2007, and then rebounding strongly and steadily to $1.90/share in 2009. The company does not pay a dividend. Outstanding shares have been steady at 75 million reported in 2005 and increasing only slightly to 77 million in 2009.

Free cash flow has been positive and growing recently with $14 million reported in 2007, increasing to $62 million in 2008 and $129 million in 2009.

Regarding the balance sheet, as reported by Morningstar, this company has a relatively 'pristine' set of numbers with $416 million in cash, which by itself could pay off both the current liabilities of $269.1 million and the long-term liabilities of $123.7 million combined!

Calculating the 'current ratio', adding the 'other current assets' to the 'cash' results in a total of $854 million in current assets which when compared to the $269.1 million in current liabilities yields a very strong ratio of 3.17 suggesting a very solvent company easily able to pay its current bills.

Examining Yahoo "Key Statistics" on ResMed, we can see thatwith a market capitalization of $3.44 billion, ResMed qualifies as a "mid cap" stock. The company currently trades at a trailing p/e of 23.97, which might by itself be considered 'rich', but taking into consideration the '5 yr expected' earnings, the company actually has a very reasonable PEG ratio of only 0.96.

Yahoo reports that the company has 75.54 million shares outstanding with 70.51 million that float. As of 8/26/09, there were 3.82 million shares out short. With an average trading volume recently placed at 371,244 shares, this works out to a short ratio (as of 8/26/09) of 8.4. Applying my own arbitrary '3 day rule' on short interest, this appears to be significant in terms of a potential short squeeze driving the stock higher in the face of any additional good news.

No dividends are paid and as I earlier noted, the company last split its stock in October, 2005, with a 2:1 stock split.

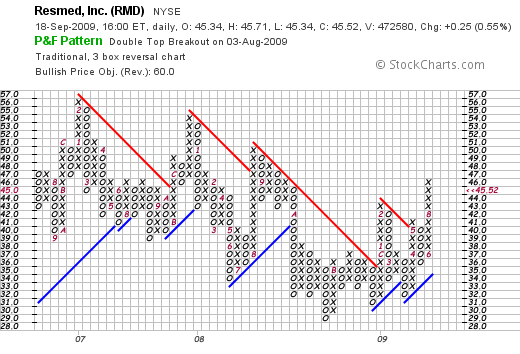

If we look at the 'point & figure' chart on ResMed (RMD) from StockCharts.com, we can see that the stock has been under pressure for the last several years, with sequential lower lows culminating in a low in July, 2008, at $29/share. Recently the stock has been generating a short series of higher highs and higher lows and appears to be positioned to move higher without appearing overextended.

To summarize, I have been a big fan of ResMed (RMD). I believe in the utility of their product---the health benefits of treating obstructive sleep apnea appear obvious. But beyond this, ResMed is a company that has been generating revenue and earnings growth, maintaining its outstanding shares, and reporting solid financial numbers in these somewhat less than solid financial times.

Valuation-wise, the p/e is a bit rich, but when taken into consideration the expected growth rate doesn't appear rich at all. There are quite a few shares out short (as of latest Yahoo numbers) which may also support further price appreciation. Their last quarter was strong and they beat expectations. Now, if only they paid a dividend too!

ResMed (RMD) is the kind of stock I would like to get back into my own trading portfolio if the opportunity should arise. Meanwhile, I shall wait for my own holdings to indicate whether it is time to be shifting from cash into another holding or in fact selling a holding and moving towards cash!

If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 8:22 PM CDT

|

Post Comment |

Permalink

Updated: Sunday, 20 September 2009 10:15 PM CDT

Sunday, 6 September 2009

Church & Dwight (CHD) "Revisiting a Stock Pick"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I apologize to my readers for my relative paucity of posts to my blog. I am committed to continuing to share my ideas with all of you and certainly to continue to offer you my actual experience in my own trading account.

I apologize to my readers for my relative paucity of posts to my blog. I am committed to continuing to share my ideas with all of you and certainly to continue to offer you my actual experience in my own trading account.

The economic deterioration appears to have slowed in intensity yet it has not yet reversed direction. As reported the other days, the national unemployment rate as of August, 2009, has reached 9.7%, the highest level since June, 1983. The economy shed 216,000 jobs in August, an awful figure yet a continuation of the gradual improvement from June, 2009 when the number was 463,000 jobs lost and July, 2009.when 276,000 jobs disappeared. Suddenly less bad news is becoming good news!

On another cautiously optimistic note we are also seeing improvement in the housing number figures. Sales of new homes rose 9.6% in July 2009, making it 3 months in a row of improved figures. Bank failures continue to be reported; we are up to 84 this year, from 25 in 2008 and 3 in all of 2007! And retail sales remain week with sales in August 2009 dipping an average of 2.9% with the only good news being that it wasn't as bad as was expected---analysts had been looking for a 3.8% decline according to a survey by Thomson Reuters.

Considering this bearish although seemingly improving environment, it is no wonder that an amateur investor like myself has grown increasingly conservative in my own approach. But my philosophy hasn't really changed in terms of the kind of stocks and the kind of financial underpinnings to those companies that make me personally find them attractive for consideration.

I would like to share with you another look at Church & Dwight (CHD), a stock that I first reviewed back in January 31, 2006 here on this blog, when it was trading at $36.80. I still do not own any shares of this company but it is one that is on my own investing horizon. Church & Dwight (CHD) closed at $56.50 on September 4, 2009, down $.31 or (.55)% on the day.

What do they do?

They are a household products company with products ranging from baking soda to toothpaste to laundry detergent. As the Yahoo "Profile" on CHD explains, Church & Dwight

"...together with its subsidiaries, develops, manufactures, and markets a range of household, personal care, and specialty products under various brand names in the United States and internationally. The company operates in three segments: Consumer Domestic, Consumer International, and Specialty Products. The Consumer Domestic segment offers household products for deodorizing, such as ARM & HAMMER baking soda and cat litter products; laundry and cleaning products, including XTRA and ARM & HAMMER laundry detergents, OXICLEAN pre-wash laundry additive, SCRUB FREE, KABOOM, ORANGE GLO, and BRILLO cleaning products; and personal care products, such as TROJAN condoms, ORAJEL oral analgesics, NAIR depilatories and waxes, FIRST RESPONSE and ANSWER home pregnancy and ovulation test kits, ARRID and ARM & HAMMER antiperspirant, and SPINBRUSH battery-operated toothbrushes. The Consumer International segment primarily sells various personal care products in international markets, including France, the United Kingdom, Canada, Mexico, Australia, Brazil, and China. The Specialty Products segment produces sodium bicarbonate, which it sells together with other specialty inorganic chemicals for a range of industrial, institutional, medical, and food applications."

In other words, they are a rather diversified consumer business providing for basic needs in many markets worldwide.

How are they doing?

Let's take a look at a few of the financial numbers that make me more convinced of the suitability of this 'stock pick' for my blog. First of all, as I like to do, let's review the latest quarterly financial result.

On August 4, 2009, CHD reported 2nd quarter results. For the quarter ended June 26, 2009, earnings came in at $58.2 million or $.81/share. This was up from $45.8 million or $.66/share the prior year same period. Sales for the quarter increased to $623.1 million from $594 million. Thus it wasn't a bad quarter at all for Church & Dwight!

More importantly perhaps to anticipate the stock price reaction to any piece of news, is what analysts were expecting. In this case, analysts polled by Thomson Reuters had been expecting net income of $.79/share on revenue of $611.5 million. Thus CHD beat expectations on both earnings and revenue results!

In addition, it is also a big plus in my book if we can hear something positive from management within these announcements regarding future results. In fact CHD went ahead and raised earnings expectations for the year to a range of $3.36 to $3.40/share from prior guidance of $3.30 to $3.35 per share. Analysts according to Thomson Reuters had previously been expecting profit of $3.35/share. Thus the guidance was above expectations!

As if this wasn't enough, the company went ahead and announced a significant increase in the dividend from $.09/share to $.14/share. So while we have many stocks with revenue dips, uncertain guidance, and dividend cuts, Church & Dwight comes out and knocks one 'right out of the park'!

What about longer-term?

There are many places to find this sort of information. For several years now I have been utilizing Morningstar.com which provides the individual investor what I believe to be a very useful amount of information. In particular, the "5-Yr Restated" financials on Church & Dwight (CHD) is a very useful place to start.

Here we can see clearly illustrated the steady increase in revenue from $1.4 billion in 2004 to $2.42 billion in 2008 and $2.48 billion in the trailing twelve months (TTM). Earnings have also steadily increased from $1.36/share in 2004 to $2.78/share in 2008 and $3.00/share in the TTM. Dividends are not only paid to shareholders but they also have been steadily increased from $.21/share in 2004 to $.34/share in 2008 and $.36/share in the TTM, with a new indicated payment of $.56/share going forward as I just noted above. Outstanding shares, where I might actually prefer to see a diminution of numbers, have only been modestly increased from 68 million in 2004 to 71 million in 2008 and the TTM.

Free cash flow is positive and steadily increasing. $139 million reported in 2006, up to $336 million in 2008 and $400 million in the TTM.

The balance sheet appears solid with $357.0 million in cash and $481.0 million in other current assets per Morningstar with $500.9 million in current liabilities yielding a current ratio of approximately 1.8. The company does have $1.03 billion in long-term liabilities on its books.

What about valuation?

Looking at Yahoo "Key Statistics" on CHD, we see that the company is a mid-cap stock with a market capitalization of $3.97 billion. The trailing p/e is a moderate 18.80, with a forward p/e estimated at 14.75. The PEG suggests a reasonable p/e valuation with a value of 1.32. There are 70.3 million shares outstanding with 64.78 million that float. As of 8/11/09, there were 2.92 million shares out short, yielding a mildly significant short interest ratio of 4.2. (I assign 'significance' on this ratio when there are over 3 days of short interest needed to be covered in case of a 'squeeze').

The company pays a forward dividend of $.56/share yielding 1.00%. With a payout ratio of only 12%, this dividend appears to be relatively secure. The stock was last split back in September, 2004, with a 3:2 stock split.

What about the chart?

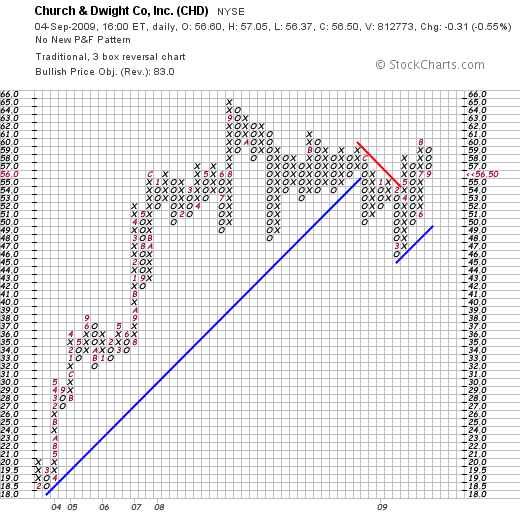

If we look at a "point & figure" chart on Church & Dwight (CHD) from StockCharts.com, we can see that the stock price made a strong move from February, 2003 when the stock was trading at around $18.50 to a high of $65 back in September, 2008. Since that time, along with the rest of the market, the stock has traded sideways, but recently, in April, 2009, broke through resistance at $54 and now is trading in an upward direction above support levels.

Summary:

To summarize, I don't really much like the economic environment that we find ourselves. Who does? We have all watched our 401k's and IRA's and personal accounts get clobbered as the economy slipped into recession and the market into a devastating bear market. Things do look a bit more hopeful recently.

To select stocks in this environment is treacherous. But if we can think about any particular type of company that might survive in this environment, a consumer staples company like Church & Dwight (CHD) might fit the bill.

As I have noted, in the latest quarter they reported increasing revenue, increasing earnings, beat expectations on both and raised guidance. They also raised their dividend! But these are not one-time events. This company has been performing like this for years!

Valuation is reasonable if not cheap. The stock chart appears reasonably optimistic in face of a difficult investing world.

I continue to employ my own investing strategy of waiting for my own holdings to advance to targeted appreciation levels before adding a new position and limiting my losses on the downside. But if I am given the opportunity to buy something new, this is the kind of stock that I shall be considering!

Thanks again for dropping by and visiting. I do not blog as often as I have and probably should, but I appreciate your visits, your comments, and your occasional encouragement! If you have any comments or questions, please feel free to reach me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 6:06 PM CDT

|

Post Comment |

Permalink

Updated: Sunday, 6 September 2009 6:15 PM CDT

Tuesday, 25 August 2009

On Picking Stocks and Market Corrections

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I set out tonight to write up an entry about a suitable stock to add to my blog. But nothing seemed right. I scanned through the list of the top % gainers, my usual starting place, but there were few stocks over $10. And when the few names I found seemed to have potential their latest earnings were in general a little less than exciting. Financial results are reported that are mediocre yet because they are ahead of the already more dismal expectations, the stock rises. Not enough in my book.

In fact if you are familiar with my own trading account, (you can see my current holdings on my Covestor page), you will see that even my own relatively aggressive momentum strategy has mutated into a more conservative large/mid-cap growth/value strategy that involves stocks with relatively secure franchises selling at reasonable valuation with reasonable dividend payments. (As I get older, I continue to start investing more and more like my original inspiration, my late father.)

Briefly, I am still looking for stocks making moves higher with solid recent earnings reports, a record of steadily improving financial results, reasonable valuation, and a decent charty. O.K. so I want everything :). But why not.

In my own portfolio I have caught myself chasing performance swapping out of Colgate (CL) for Coca-Cola (KO). Moving from Haemonetics (HAE) to Oshkosh (OSK), switching from PetSmart (PETM) to TJX (TJX).

Perhaps if I had been a bit wiser, I would have understood that my own frustration with my own account was merely a frustration with the overall market that was influencing my own holdings. With nothing wrong with the previously held stocks, their resistance to upward price appreciation, was merely a reflection of the difficult stock market. Chasing performance hasn't worked. Oshkosh (OSK) was sold after incurring a loss. The only possible improvement was the pick-up with TJX, which itself is in the process of consolidation after a large price appreciation this year.

I am back to my disciplined investment system. I shall hold onto stocks in my portfolio until they either incur losses, incur large gains, or actually report major financial problems. I cannot argue more about trusting your strategy, implementing your strategy, and keeping your cotton-pickin' hands off the stocks when you shouldn't be messing with your own plans.

Time and time again, I discover my own trading flaws that keeps me as an amateur, no matter how many blog entries I can accumulate on this website.

If you have any comments or questions, please feel free to email me at bobsadviceforstocks@lycos.com or leave them right here!

Yours in investing,

Bob

Wednesday, 12 August 2009

I Stand With Susan Hessel

My good friend Susan Hessel is recovering from surgery today for breast cancer. Last week, to explain to her friends, she wrote a piece about her own experience with this disease. Always smiling, always optimistic about what life was handing her, I asked her if she would kindly allow me to share with my own readers her words that are far more eloquent and informative than anything I could write here about this disease that strikes so many women today. She consented to me blogging her words; she herself is a wonderful writer and author of books---here is a list of books from Amazon that she has been involved in---and has a sense of humor that allows her to redefine even the notion of cheese-head as you can see from her Facebook page.

My good friend Susan Hessel is recovering from surgery today for breast cancer. Last week, to explain to her friends, she wrote a piece about her own experience with this disease. Always smiling, always optimistic about what life was handing her, I asked her if she would kindly allow me to share with my own readers her words that are far more eloquent and informative than anything I could write here about this disease that strikes so many women today. She consented to me blogging her words; she herself is a wonderful writer and author of books---here is a list of books from Amazon that she has been involved in---and has a sense of humor that allows her to redefine even the notion of cheese-head as you can see from her Facebook page.

Without any further words from me, this is what Susan had to say in her email to me and to many of her friends:

I Stand With Tevye

Susan T. Hessel

Do you remember that scene in the musical Fiddler on the Roof when Tevye looks up at the sky and says to G-d, “I know, I know. We are Your chosen people. But, once in a while, can't You choose someone else?”

Do you remember that scene in the musical Fiddler on the Roof when Tevye looks up at the sky and says to G-d, “I know, I know. We are Your chosen people. But, once in a while, can't You choose someone else?”

It’s a joke among Jews that we really didn’t need to be chosen in so many ways that we are. Now I get to add breast cancer to that list. Or do I?

It’s certainly how I felt when my doctor called me a few weeks back and told me that she and the breast radiologist had been talking and thought that because of my “ethnicity” they should go one step further and I should have a breast MRI.

“My ethnicity?” I asked.

“Yes, didn’t you know that Ashkenazic Jewish women are at greater risk for breast cancer?”

“I’ll convert,” I told my doctor, maybe only a quarter kidding at that moment. (And yes, I did tell my rabbi I said that. He laughed.)

“I don’t think that will work,” my doctor said to my suggestion of conversion. “It’s hereditary.”

“Ahh,” I said, “I’ll blame my parents.”

Of course, to blame my parents, who are no longer with me, would be tacky and inappropriate. It would open me to similar feelings from my kids. They chose lousy parents heredity wise, but that’s another story.

I am of Ashkenazic – Central/Eastern European Jewish descent. And yes, I do have breast cancer and am about to have a mastectomy. But who knows if it is genetic or something related to the environment or simply the flying fickle finger of fate (think Laugh-In television show in the 1960s).

I have talked with other Jewish women who didn’t know about this connection either. I decided to do some research. This summary is from the National Human Genome Research Institution:

In 1995 and 1996, studies of DNA samples revealed that Ashkenazi (Eastern European) Jews are 10 times more likely to have mutations in BRCA1 and BRCA 2 genes than the general population. Approximately 2.65 percent of the Ashkenazi Jewish population has a mutation in these genes, while only 0.2 percent of the general population carries these mutations.

Further research showed that three specific mutations in these genes accounted for 90 percent of the BRCA1 and BRCA2 variants within this ethnic group. This contrasts with hundreds of unique mutations of these two genes within the general population. However, despite the relatively high prevalence of these genetic mutations in Ashkenazi Jews, only seven percent of breast cancers in Ashkenazi women are caused by alterations in BRCA1 and BRCA2.

I really, really, didn’t know about that Ashkenazic Jews were at higher risk. And, I have done more than my fair share of medical writing. It was probably information that I needed to know but wished I didn’t know.

However, it’s not all that clear cut. Science Daily reported in 2006 on a study in the American Journal of Public Health that challenged “This population-based approach, warning that disparities in access to care and other unintended consequences for specific ethnic groups can result, and may have already occurred.”

“The science of breast cancer genetics has been marked by methodological inconsistency in how researchers defined ‘Ashkenazi Jew,’” said study coauthor Sherry Brandt-Rauf, J.D., associate research scholar at the Center. Most scientists relied on study participants’ self-identification. Ashkenazi Jews are descended from Jews who lived in central and Eastern Europe, but a complex history of migrations, and multiple cultural and religious meanings of Ashkenazi, makes self-identification problematic.”

At any rate, I was talking with a woman who had breast cancer several years ago and she only discovered after genetic testing that she was Jewish. (The geneticist wishes her a Happy Passover.” Her family had decided to become Christians after coming to this country at the turn of the 20th century. But it was funny, this woman remembered hearing Yiddish many years ago and understanding what the women were saying. At the time she thought she was clairvoyant.

The Chicago Center for Jewish Genetics Disorders also discusses the issue. Here is its Summary of BRCA1 and BRCA2 Facts:

• Certain ethnic groups are at increased risk for having BRCA1 and BRCA2 mutations; three particular mutations are more common among Ashkenazi Jews.

• Women with mutations in BRCA1 or BRCA2 are more likely to develop breast or ovarian cancer but are not guaranteed to do so.

• A BRCA1 or BRCA2 mutation is more likely to be found in an individual with a family history of particular cancers.

• Women with BRCA1 or BRCA2 mutations are more likely to get cancer at a younger age than the general population.

• Men can also have BRCA1 or BRCA2 mutations, which puts them at an increased risk for prostate, breast, and some other cancers.

• A BRCA1 or BRCA2 mutation can also be passed down through the father so it is important to consider both sides of the family history.

• The decision to get tested can be very complicated. Talk to your doctor or a genetic counselor if you are interested in testing.

What does this all mean? I guess to those of us who are Jewish women, we should be very vigilant. Get regular mammograms and don’t panic. Hey, that also applies to non-Jewish women. I didn’t think I had any family history of breast cancer, but my grandmother died of some kind of cancer when I was 3. My friend who had cancer and later discovered she was Jewish suggested there was no way of knowing if whatever cancer my grandmother had was lymphoma as we know it today. Then maybe the cancer was in the lymph and then spread. I’m going to ask for genetic testing.

By the way, there is one Jewish breast cancer link that is confirmed: My certificate of Bat Mitzvah (with four other women at CSOA) from 2001 arrived on the day of my biopsy last week. And that link did not require millions of dollars in research to identify. ☺

My mom and I used to joke about the expression, “Now is not the time to panic.” We wondered if they – whoever they are – would send out a memo or appear on TV and radio to announce, “Now is the time to panic.” At that point we would run in circles with our hands up in the air screaming.

The good news is with technology, they can send the panic message via email, text, by Twitter and Facebook.

I haven’t received it so far. And not that I would want to cause harm to anyone else, but like Tevye asked, “Once in a while, can't you choose someone else?”

Susan came out of surgery today. She wouldn't be awake enough to read her own words on the blog but I am glad to count myself as one of her friends. She is a courageous woman facing a terrible disease; a disease that threatens the lives and well-being of women across America and around the globe.

I stand with Susan T. Hessel. But once in awhile God, couldn't you have chosen someone else?

Thursday, 6 August 2009

Oshkosh (OSK) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

I really felt like an "amateur investor" today when I needed to sell my shares of Oshkosh (OSK) after they hit and passed my 8% loss tolerance. Like the rocket on the way up, the stock turned around and plunged with the market. I am still very impressed by the company, the $2 billion in new contracts for MRAP's and would consider this a very worthwhile stock to be acquiring shares in--as soon as the technicals show a little bit of support.

Like a car, I have my driving rules (and I was 'speeding' with my Oshkosh purchase!), my seatbelts and my airbags---in order that I can survive in the chaos of the investment world. Like airbags in vehicles designed to limit injury to inhabitants of colliding motor vehicles, my trading rules to limit losses are designed to get me out of a bad situation intact--or at least only slightly injured!

These loss limits, which I have described many times elsewhere on the blog, include limiting losses to (8)% after an initial purchase, break-even after a first partial sale, and then to 1/2 of the highest percentage gain after two or more partial sales at appreciation targets. For instance, I like to sell 1/7th of a holding after a 30% appreciation of a stock after an initial purchase. In that case, if I have only sold a portion once, I would sell if it should then decline to my purchase price--my break-even level.

My next 'targeted sale' is at a 60% appreciation from purchase level. After selling another 1/7th of my remaining shares, I would mentally (or actually) be moving up my sale point on the downside to a 30% appreciation point. Thus, I try to limit losses and preserve gains even if a stock, like Oshkosh (OSK), should dip in price.

I am aware that many stocks like Oshkosh with underlying great news will likely rebound. And I shall miss many of those rebounds with these rather rigid trading rules. But one of my main goals in this account is preservation of capital and enforcing a trading discipline to insure my own behavior. And thus the sale of my OSK shares.

The details? I sold 80 shares of Oshkosh (OSK) (my entire position) at a price of $28.16 today (8/6/09). These shares had been purchased at $30.73 on 8/3/09 (just 3 days ago!) resulting in a loss of $(2.57)/share or (8.4)% since purchase.

Finally, what to do with the proceeds of this sale. While I have been bending the rules (to little avail!) lately, with my swaps of positions as I have been truly trying to 'chase performance', a sale like this reminds me of my own 'amateur' status, and is a signal not to be reinvesting proceeds but rather to be 'sitting on my hands' with these funds.

I shall be adding a new position when one of my remaining holdings hits an appreciation target on the upside and when once again I can sell 1/7th of that holding on 'good news'!

Thanks again for visiting! I shall try to learn from this sale as well---as much as I like Oshkosh (OSK) and am impressed by the contracts obtained, that we are now dealing with volatile markets that have little follow-through momentum....so chasing performance, at least currently, may be a poor game to be playing!

If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Tuesday, 4 August 2009

Switching from Haemonetics (HAE) into Oshkosh Corp. (OSK) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

As is part of my blogging, I wanted to share with you a 'swap' I made out of my position in Haemonetics (HAE) and into Oshkosh (OSK). Both of these are mid cap stocks but that is where the similarity ends.

As is part of my blogging, I wanted to share with you a 'swap' I made out of my position in Haemonetics (HAE) and into Oshkosh (OSK). Both of these are mid cap stocks but that is where the similarity ends.

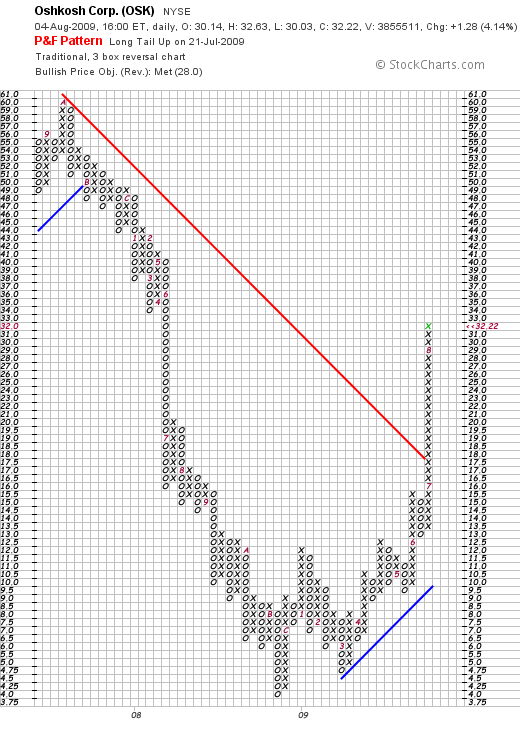

On Monday, August 3, 2009, I sold my 50 shares of Haemonetics (HAE) at $55.08 after what I viewed as both technical weakness on somewhat less than stellar earnings, and purchased 80 shares of Oshkosh Corp (OSK) at $30.73 on what I viewed as compelling news on this 'old favorite' of mine and a nearby Wisconsin-based firm. Oshkosh (OSK) closed at $32.22 today, up $1.28 or 4.14% on the day...so I am already a few percentage points ahead on this purchase!

Haemonetics (HAE) is a stock I have purchased two times, originally picking up 50 shares on October 27, 2008, at a cost basis of $51.54, so I had a gain of $3.54 or 6.9% since purchase. So it wasn't exactly a waste. And I do need to develop more patience with all of my holdings!

Basically Haemonetics (HAE) reported 1st quarter earnings results yesterday. They beat expectations of $.65/share in earnings coming in at $.69/share. However, 1st quarter revenue missed expectations at $154.1 million while analysts had been expecting slightly more at $156.6 million. And has been so common, the market over-reacts on earnings news that even slightly appear to be failing to meet expectations. And Haemonetics (HAE) was no exception dropping 4% plus that day. I pulled the plug on the stock which while still showing promise on a fundamental basis, was acting as a drag on my portfolio.

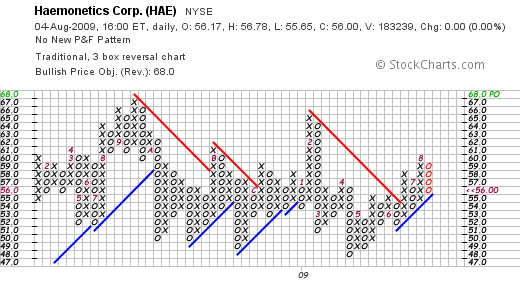

To illustrate this further, let's take a look at the point & figure chart for Haemonetics (HAE) from StockCharts.com spanning January, 2008 to the current price movement:

OK so it isn't the most exciting stock in the market. And I really should be more patient. But I exercised disgression once again (I promise to try to stay put a bit the rest of this month!)...and unloaded my shares. I had another stock in mind that was getting me very interested....

Shortly after starting my blog in 2003, I wrote up Oshkosh (OSK) on June 12, 2003. I "revisited" Oshkosh (OSK) on February 2, 2006, and even did a podcast on the stock. My stock club has been in and out of this stock and last month acquired a small position and added to it this evening with a few more shares.

Shortly after starting my blog in 2003, I wrote up Oshkosh (OSK) on June 12, 2003. I "revisited" Oshkosh (OSK) on February 2, 2006, and even did a podcast on the stock. My stock club has been in and out of this stock and last month acquired a small position and added to it this evening with a few more shares.

As background, it is important to know that Oshkosh (OSK) is an important supplier to the United States military, and also other allied military forces, for mine resistant ambush protected (MRAP) vehicles. IED's (improvised explosive devices or roadside bombs) contribute 75% of the casualties to coalition forces in Afghanistan as this article explains.

On July 1, 2009, Oshkosh (OSK) announced a $1.05 billion contract with the United States military for 2,244 M-ATV (mine-resistant all-terrain vehicles) beating out Force Dynamics, a partnership between Force Protection (FRPT) and General Dynamics (GD), as well as other competitors Navistar (NAV) and BEA Systems (BA) to land this contract.

That contract alone was enough to get my stock club last month interested in re-purchasing shares of OSK which had previously declined and were now rebounding with the news.

We can see the change in the chart of OSK with this announcement (chart from StockCharts.com):

What clinched the deal in my mind was the announcement on July 31, 2009, of Oshkosh (OSK) winning an additional $1.06 billion order for another 1,700 of these M-ATV's.

So when Haemonetics (HAE) hiccupped with the earnings report, I was more than ready to take the jump to Oshkosh (OSK) and purchased shares as noted above.

This stock certainly doesn't clearly fit into my usual 'steady growth in earnings and revenues' type company. In fact, on its latest earnings report on July 30, 2009, the company reported sales of $1.2 billion in the quarter (down 36% from the prior year) and a loss of (.36)/share exceeding the expected loss of $(.30)/year expected. So really a mediocre earnings report.

The Morningstar.com '5-Yr Restated' financials shows the previous record of revenue growth from $2.3 billion in 2004 to $7.1 billion in 2008 slipping to $6.5 billion in the trailing twelve months (TTM). Positive earnings growth turned into large losses from $3.58/share in 2007 to a large loss of $(16.67)/share in the TTM. Outstanding shares number only 75 million.

Free cash flow has remained positive and improved recently from $121 million in 2006 to $315 million in 2008 and $642 million in the TTM.

The balance sheet remains solid with $1.8 billion in cash and other current assets compared to current liabilities of $1.3 bilion.

In any case, the massive orders and the potential for more of these orders from the military combined with the small # of shares and the strong price momentum convinced me that I needed to climb abord Oshkosh (OSK) and see if we could ride this one over some difficult market environments!

Thanks again for stopping by and visiting! If you have any comments or questions, please feel free to leave them right on this website or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Posted by bobsadviceforstocks at 10:10 PM CDT

|

Post Comment |

Permalink

Updated: Tuesday, 4 August 2009 10:13 PM CDT

Sunday, 2 August 2009

Swapping PetSmart (PETM) for TJX Companies (TJX) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Before I write about the 'swap' I made with PetSmart (PETM) and TJX (TJX), I want to talk to you a little about "chasing performance". There is a good article on attempting to improve results by chasing after the best and latest hot stock or fund that you might want to read. In general, it is counterproductive to be switching investments or funds in pursuit of investments that have performed well in the past. Simply doesn't work.

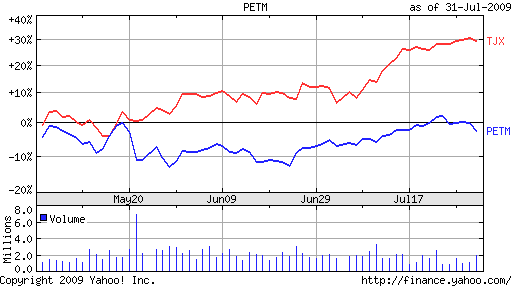

Perhaps as an amateur investor, I am guilty of the same amateur mistakes that others make. So with that in mind, after my latest review of TJX, I have been growing impatient with my PetSmart (PETM) stock which appeared to be underperforming my other holdings.

If we examine the last three months chart of the two stocks:

We can see how TJX has been outperforming PETM. But that doesn't mean that the divergence in performance shall continue. But it might!

In any case, I grew impatient and pulled the plug swapping out my shares of PETM for TJX. On July 31, 2009, I sold my 90 shares of PETM at $22.46/share, and purchased 60 shares of TJX at $36.50/share. The PetSmart shares were purchased 5/21/09 at a cost basis of $20.41/share. Thus I had a nice gain of $2.05 or 10% since purchase. TJX closed Friday at $36.23 so I was a little 'under water' on this purchase already.

Thanks so much for visiting my blog! If you have any comments or questions, please feel free to leave them right here or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Thursday, 30 July 2009

"Blinking" on Colgate Palmolive (CL)

Hello Again my friends! It is late and I am having a bit of seller's remorse. Earlier today I parted company with my shares of Colgate (CL) because of a slight miss on revenue while earnings exceeded expectations in the latest report.

I think I got a bit 'self conscious' of the public nature of my blogging and trading and probably rushed that trade. Over and over we have seen stocks pummeled on announcements that really aren't bad. The market wants to sell on good news and sell more on bad. It is probably best not to respond to these actions after earnings announcements and instead concentrate on breathing slowly, relaxing, and letting the chaos pass as it always do.

I certainly like Coca-Cola (KO), but Colgate-Palmolive is truly a phenomenal world company. I blinked when looking into the face of the irrational sell-off. Like a 'weak sister' as investors like myself are called I dumped my shares grabbing my small gain and moved into Coke. Not exactly the cool-headed investor I pride myself in being.

Perhaps that is what separates an amateur investor like myself from a professional. Perhaps knowing this is the first step on that road. We can certainly hope.

As I write over and over, it is important to have specified sale points for both good and bad price moves. It is also important to identify significant fundamental negative reports that might trigger a premature sale. However, this kind of volatility is not a game I should be playing or even get caught up in. I hope all of you can learn from my own actions as well!

In any case, it is late, tomorrow is certainly another day, and I still have a portfolio of mighty fine companies. I just miss my Colgate already and will be sure to keep it on my list of stocks to revisit in the future.

Yours in investing,

Bob

Colgate Palmolive (CL) and Coca-Cola (KO) "Trading Transparency"

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisers prior to making any investment decisions based on information on this website.

Colgate-Palmolive (CL) is definitely one of my favorite 'comfort stocks'. However, I wasn't very comfortable when they reported their 2nd quarter results that beat expectations on earnings but missed on revenue. As reported today before the open, profit came in at $1.07/share exceeding expectations of $.98/share, but revenue came in a little light at $3.75 billion, under the expected $3.83 billion. Not really a big deal imho, but enough to spook skittish investors (like myself) who really don't enjoy hanging on to a stock when the market roars ahead and the stock price drops on a small disappointment. Earlier today I sold my 43 shares of CL at $71.92/share. These shares had been purchased 4/24/09, just 3 months ago at a cost basis of $59.55/share. Thus, I had a gain of $12.37/share or 20.8% since purchase.

Colgate-Palmolive (CL) is definitely one of my favorite 'comfort stocks'. However, I wasn't very comfortable when they reported their 2nd quarter results that beat expectations on earnings but missed on revenue. As reported today before the open, profit came in at $1.07/share exceeding expectations of $.98/share, but revenue came in a little light at $3.75 billion, under the expected $3.83 billion. Not really a big deal imho, but enough to spook skittish investors (like myself) who really don't enjoy hanging on to a stock when the market roars ahead and the stock price drops on a small disappointment. Earlier today I sold my 43 shares of CL at $71.92/share. These shares had been purchased 4/24/09, just 3 months ago at a cost basis of $59.55/share. Thus, I had a gain of $12.37/share or 20.8% since purchase.

Preserving gains is about as important as avoiding losses in my strategy and I chose to swap out of Colgate (CL) and purchased some shares of Coca-Cola (KO) hoping that my portfolio would 'go better with Coke'!

I went ahead and purchased 50 shares of Coca-Cola (KO), a slightly smaller position than my Colgate, at $50.39/share this morning.

I went ahead and purchased 50 shares of Coca-Cola (KO), a slightly smaller position than my Colgate, at $50.39/share this morning.

Let's take a brief look at Coke and see if it makes sense and might offer almost as good an opportunity for this investor as my shares in Colgate!

On July 21, 2009, Coca-Cola (KO) reported 2nd quarter results. Earnings climbed 43% to $.88/share vs. $.61/share last year...but last year's results were dampened by $.40/share in one-time restructuring charges and asset 'write-downs'. Sales dipped 9% to $8.27 billion. So in fact, this was less than stellar.

Looking at the Morningstar.com "5-Yr Restated" financials on Coke, we can see the steady revenue growth from 2004 at $21.7 billion, increasing to $31.9 billion in 2008 only to dip slightly to $31.7 billion in the trailing twelve months.

Earnings have increased from $2.00/share in 2004 to a peak of $2.57/share in 2007, dipping to $2.49/share in 2008 and $2.43/share in the TTM. Again demonstrating a little weakness recently.

Free cash flow is not a problem with KO, with $4.5 billion in 2006 increasing to $5.3 billion in the TTM. This contributes to a balance sheet with $6.8 billion of cash, $7.9 billion of other current assets balanced against current liabilities of $13.2 billion. The company also has a moderate level of $9.2 billion in long-term liabilities.

Looking at some valuation numbers on Yahoo "Key Statistics", we can see that this is a large cap stock with a market cap of $116.5 billion. The trailing p/e is a moderate 18.63 with a forward p/e of 15.16. The PEG ratio, however, is a bit rich at 2.44 suggesting a bit of a premium price for this stock relative to its growth rate as estimated.

There are 2.32 billion shares outstanding with 2.30 billion that float. Currently there are 27.14 million shares out short representing 2.7 trading days of volume (the short interest ratio) below my own 3 day cut-off for significance. The company pays a $1.64 dividend yielding a forward dividend yield of 3.3%. The company last split its shares 2:1 in May, 1996.

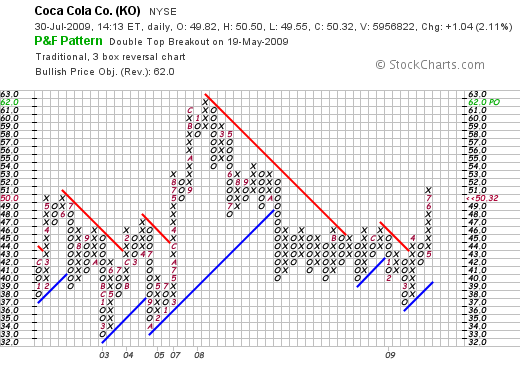

And the chart? Looking at the 'point & figure' chart on Coca-Cola (KO), we can see that the stock hit a high of $62 in January, 2008, before pulling back as low as $37 in March, 2009. The stock recently has broken out past resistance and is acting quite strong at its current level of $50.32.

Quite frankly, I like Coca-Cola (KO) stock as a long-term growth and recovery play on the global economy. It is a 'comfort stock' from my perspective, but the numbers are not quite as strong currently as I might like to see in a stock in my portfolio. Technically, the stock appears to be anticipating improved numbers as the stock price has appreciated nicely the past couple of months.

I am not sure if this stock is the 'Real Thing' or not. However, as I build my portfolio, while stepping aside from Colgate--at least temporarily--I shall try to see if this stock has enough 'fizz' to help move my portfolio in the right direction. If instead it turns out to be 'flat' instead, well I can always move on with another stock holding!

Thanks again for stopping by and visiting my blog! If you have any questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com.

Yours in investing,

Bob

Newer | Latest | Older