Stock Picks Bob's Advice

Tuesday, 8 August 2006

"Revisiting a Stock Pick" inVentiv Health (VTIV)

CLICK HERE FOR THE INVENTIV PODCAST

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I was looking through the list of top % gainers this evening and I came across an old favorite of mine inVentiv Health (VTIV) that had traded strongly higher today, in fact closing at $29.88, up $2.89 or 10.71% on the day in an otherwise weak stock market. I do not personally own any shares of this stock but my son does own 40 shares of VTIV in an account that I manage for him. This company, which used to be called Ventiv Health, formally changed its name to inVentiv Health (VTIV), a act approved by shareholders on June 16, 2006.

I was looking through the list of top % gainers this evening and I came across an old favorite of mine inVentiv Health (VTIV) that had traded strongly higher today, in fact closing at $29.88, up $2.89 or 10.71% on the day in an otherwise weak stock market. I do not personally own any shares of this stock but my son does own 40 shares of VTIV in an account that I manage for him. This company, which used to be called Ventiv Health, formally changed its name to inVentiv Health (VTIV), a act approved by shareholders on June 16, 2006.

I first posted Ventiv Health on Stock Picks Bob's Advice exactly one year ago on August 8, 2005, when the stock was trading at $24.19. With today's close at $29.88, this represents an appreciation of $5.69 or 23.5% since posting. Let's take another look at this stock and I will try to share with you my thoughts why this company deserves a spot on this blog.

First of all, what they do?

According to the Yahoo "Profile" on inVentiv, the company:

"...provides commercialization services to the pharmaceutical and life sciences industries in the United States and internationally. It operates through three segments: inVentiv Clinical, inVentiv Communications, and inVentiv Commercial."

And how about the latest quarterly report?

Actually, it was the earnings report announced just before the opening of trading that pushed the stock higher today. This morning, VTIV announced 2nd quarter 2006 results. For the three months ended June 30, 2006, total revenue increased 39% to $183.0 million in the second quarter of 2006 compared to $131.8 million for the same quarter in 2005. Net income increased 100% from $10.5 million to $21 million this year. Net income increased almost 100% to $.69/share, up sharply from $.38/diluted share the prior year. Also adding to the bullish sentiment on the stock was the announcement today of a multiyear contract with Novartis pharmaceuticals Corp. All-in-all a very nice day for this company!

How about longer-term results?

For this, the Morningstar.com "5-Yr Restated" financials report on VTIV is most helpful. On this page, we can see that revenue results, which first declined from $294.8 million in 2001 to $215.4 million in 2002, has since been increasing steadily to $556.3 million in 2005 and $609.1 million in the trailing twelve months (TTM).

Earnings, which were at a loss of $(2.58) in 2001, improved to $.35/share in 2002, then dipped to $.24/share in 2003. However, since 2003, earnings have climbed strongly to $1.56/share in 2005 and $1.57/share in the TTM. The latest quarter just commented on continues this strong growth record.

The company has increased its shares slightly from 23 million in 2001 to 27 million in 2005 and 29 million in the trailing twelve months.

Free cash flow has been improving steadily the past few years from $13 million in 2003 to $49 million in 2005 and $68 million in the TTM.

Looking at the balance sheet as reported on Morningstar.com, we find VTIV with $43.9 million in cash and $172.5 million in other current assets. This combined $216.4 million, when compared to the $127.4 million in current liabilities yields a current ratio of 1.7. In addition, the company $205.4 million in long-term liabilities. While the level of liabilities appears manageable imho, there are stronger balance sheets on the stocks we have reviewed elsewhere. However, with the growing free cash flow, this really doesn't seem to be a problem for this company.

What about some valuation numbers?

Reviewing the Yahoo "Key Statistics" on VTIV, we find that the company is a small mid-cap stock with a market capitalization of only $871.24 million. The trailing p/e is a very reasonable 19.06 imho, with a forward p/e (fye 31-Dec-07) of only 17.79. The PEG ratio (5 yr expected) is reported at 1.27.

According to the Fidelity.com eresearch website, VTIV is in the "Management Services" industrial group. Within this group, VTIV has a reasonable Price/Sales ratio of only 1.3. Topping this group is Ceridian (CEN) with a Price/Sales ratio of 2.3. This is followed by Heidrick & Struggle (HSII) at 1.5, Accenture (ACN) at 1.4 and then inVentiv at 1.3. Companies with lower Price/Sales ratio than Ventiv include Hewitt Associates (HEW) at 0.8, and Bearing Point (BE) at 0.5.

inVentiv is also one of the most profitable (as measured by the higher return on equity) stocks in this group with a ROE of 18%. Topping the group is Accenture at 62.2%. After inVentiv is Heidrick & Struggle at 16.9%, Ceridian at 10.9%, Hewit Associates at 10.3% and Bearing Point at a negative (53.7)%.

Returning to Yahoo, we see that there are 29.16 million shares outstanding with only 27.50 million that float. Currently there are 1.91 million shares out short (as of 7/11/06), representing 7% of the float or 8.9 trading days of volume. With today's excellent earnings report, the large number of shares out short (greater than my own 3 day short interest rule), this may well have been a bit of a squeeze on all those shorts scrambling to cover their pre-sold shares with new purchases of this stock! Just a thought :).

No cash dividend is paid and no stock split is reported on Yahoo.

What does the chart look like?

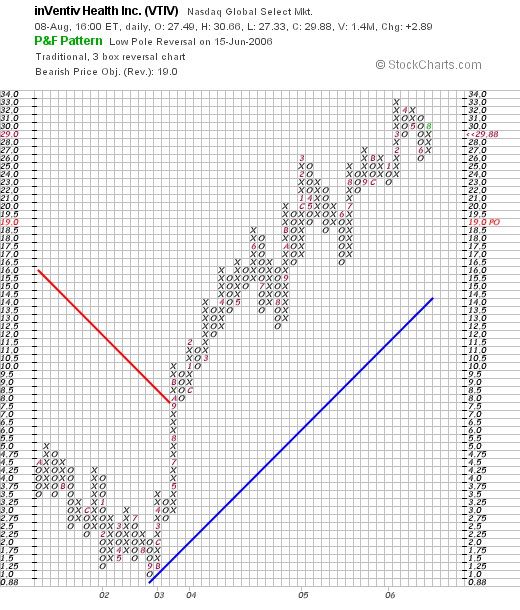

If we take a look at the "Point & Figure" chart on VTIV from StockCharts.com, we can see that the chart, which was declining though 2001 and 2002, turned around in 2003 and moved sharply higher. This coincides with the turn-around in earnings which once again emphasizes the close relationship between earnings performance and stock price imho. Since breaking through resistance in September, 2003, at $8.00/share, the stock has been trading very steadily higher to its current level around $29.88, a little below its recent high of $33 made in March, 2006.

Summary: 'So what do I think about this stock?'

Let's review some of the things I have discussed in this blog entry. First of all, the stock moved higher today in an otherwise anemic trading day. A plus. The company did this on a strong earnings report and the announcement of a multiyear contract with Novartis. Both pieces of good news.

Longer-term, the Morningstar.com "5-Yr Restated" financials look strong with steady five year revenue and earnings growth (except a dip 3 or 4 years ago). Earnings have been expanding strongly the past several years as well. The company is releasing a few shares the past few years, but certainly the financial reports have been staying ahead of the expanded float. Free cash flow is positive and growing strongly. The balance sheet is adequate if not fabulous.

Finally, valuation is reasonable with a p/e in the teens, a PEG just over 1.2, and a relatively reasonable Price/Sales ratio with a strong ROE.

In addition, the graph shows a strong upward movement to the stock price. Helping this along today appears to be a relatively large short interest of investors betting against this company.

In conclusion, I like this stock. I am not in the market to be purchasing any but I have bought just a few shares for my son this past year. Thanks so much for stopping by and visiting my blog! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, please remember to drop by and visit my Stock Picks Bob's Advice podcast site, where you can hear me drone on and on, if reading me wasn't enough. jk.

Bob

Posted by bobsadviceforstocks at 8:54 PM CDT

|

Post Comment |

Permalink

Updated: Tuesday, 8 August 2006 10:17 PM CDT

Saturday, 5 August 2006

Morningstar (MORN) "Weekend Trading Portfolio Analysis"

CLICK HERE FOR MY PODCAST ON MORNINGSTAR

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

Over the past year or so, I have been trying to review my actual holdings in my trading portfolio on weekends. These are the stocks that I actually own and that I try to be as transparent as possible letting you know what I own, when I buy it, and when I sell it. Sometimes my trades appear brilliant, and other times, like the latest trade in Kendle, I share with you my failures. Hopefully, together we shall continue to learn about investing!

On June 25, 2006, I reviewed my Kyphon stock here on the blog. Going alphabetically through my smaller list of 11 positions, I am up to Morningstar (MORN), a stock that I own which is also the website that I use regularly in evaluating my stock picks.

On June 25, 2006, I reviewed my Kyphon stock here on the blog. Going alphabetically through my smaller list of 11 positions, I am up to Morningstar (MORN), a stock that I own which is also the website that I use regularly in evaluating my stock picks.

Currently, I have 167 shares of Morningstar. These shares were purchased 11/22/05 with a cost basis of $32.57/share. With the stock closing 8/4/06 at $36.13, I have an unrealized gain of $3.56 or 10.9% on this purchase. The stock has been under pressure recently, and in fact, closed Friday at $36.13, down $(2.61) or (6.74)% on the day. Let's take a closer look at this stock, my history with this investment, and whether it still looks attractive to purchase.

My initial purchase of Morningstar was on 11/22/05, when I purchased 200 shares of the stock. I sold 33 shares of MORN on 2/16/06 with proceeds of $42.94/share, representing a gain of $10.37 or 31.8% since purchase. This was my first targeted gain at approximately a 30% appreciation, and thus, my next targeted sale on the upside would be at about a 60% gain or 1.60 x $32.57 = $52.11/share. On the downside, after one targeted sale at a gain, my sale point moves up from the (8)% loss level to break even or $32.57/share.

Let's take a closer look at this stock--first of all, what does this company do?

According to the Yahoo "Profile" on MORN, the company

"...provides independent investment research to investors worldwide. It offers Internet, software, and print-based products for individual investors, financial advisors, and institutional clients, as well as asset management services to advisors and institutions. It operates through three segments: Individual, Advisor, and Institutional."

I certainly can attest to the usefulness of the Morningstar material; I have been using "5-Yr Restated" statements from Morningstar since I have started this blog, long before I ever owned any shares!

How about the latest quarter?

On August 3, 2006 (just a couple of days ago), Morningstar reported 2nd quarter 2006 results. For the three months ended June 30, 2006, consolidated revenue came in at $76.3 million, a 36% increase from the same quarter the prior year. Net income for the quarter worked out to $11.2 million, or $.24/diluted share, up from $9.5 million, or $.22/diluted share in the same period the prior year.

How about longer-term results?

Reviewing the "5-Yr Restated" financials from Morningstar.com on MORN :), we can see the steady growth in revenue from $91.2 million in 2001 to $227.1 million in 2005 and $244.0 million in the trailing twelve months (TTM).

Earnings/share have improved from a loss of $(.32)/share in 2001 to a profit of $.21/share in 2004, $.70/share in 2005, and $.90/share in the TTM. During this time, the number of shares have fluctuated but are fairly stable with 39 million shares in 2001, 39 million shares in 2005, increasing slightly to 41 million shares in the TTM.

Free cash flow has been growing nicely with $21 million reported in 2003, increasing to $41 million in 2005 and $53 million in the TTM.

The balance sheet looks ok, especially with the low level of long-term debt, but the cash of $82.9 million and the other current assets of $68 million, when compared to the $123.1 million in current liabilities yields a rather anemic current ratio of 1.23. Generally a current ratio between 1.0 and 1.5 is considered acceptable. This is probably ok as I noted because the long-term debt for MORN is listed as only $4.8 million.

What about some valuation numbers?

Reviewing the Yahoo "Key Statistics" on Morningstar, we find that the company is a mid-cap stock with a market capitalization of $1.47 billion. The trailing p/e is a bit rich at 40.37, but the forward p/e is a bit better (fye 31-Dec-07) of 24.09. I cannot find a PEG on Morningstar either on the Yahoo or the Fidelity website.

Reviewing the Price/Sales ratio from the Fidelity.com eresearch website, we find that MORN is in the "Asset Management" industrial group. Morningstar is the most expensive in this group as measured by this ratio with a Price/Sales of 6.9. This is followed by T. Rowe Price (TROW) at 6.8, Franklin Resources (BEN) at 5.3, Federated Investors (FII) at 3.5, Janus (JNS) at 3.2, and Principal Financial Group (PFG) the most reasonably priced with a Price/Sales ratio of only 1.5.

Fortunately, Morningstar is also one of the most profitable of the group with a Return on Equity (ROE) of 24%. This is exceeded by Federated Investors (FII) at 39.6%, and followed by T. Rowe at 23.5%, Franklin Resources at 18.7%, Principal Financial at 13%, and Janus at 4.3%.

Finishing up with the Yahoo numbers, the company has 40.76 million shares outstanding but only 20.01 million that float. Of these, 1.06 million of these shares were out short as of 7/11/06, representing 10.5% of the float or 7.7 trading days of volume. Using my 3 day rule of significance, there is actually quite a few shares out short and the stock could rally with a 'squeeze' if good news was reported. Unfortunately, the recent earnings report was apparently not very impressive to those following this stock.

No cash dividends and no stock dividends are reported on Yahoo.

What about the chart? Does the recent correction in the stock price signify a break-down in the chart pattern?

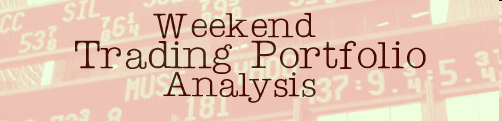

If we examine the "Point & Figure" chart on Morningstar from StockCharts.com, we can see a very steady improvement in the stock price from $19 in May, 2005, to a peak of $47 in May, 2006. However, the stock does appear to have rolled-over and is now testing a "triple-bottom" short-term. I would be rather concerned if the stock breaks down below the current level. On the other hand, if the stock can rally back above $41, I shall be breathing easier :).

So what do I think? Well, I own the stock :). I have sold the stock once on a gain but the company is just above 10% ahead of my purchase price. Thus, with no fundamental news, if the stock drops by about 9% from here I shall be selling my position. On the other hand, the latest quarter was good, the Morningstar.com 5-yr report looks good to me as well, the free cash flow is positive and growing and the balance sheet looks reasonable if not spectacular. Valuation is a bit rich with a p/e over 40 so possibly investors are thinking that the stock was priced for perfection and did not actually deliver perfection in the latest earnings report.

So that's the next stock in my trading portfolio! I hope that you enjoyed my review of my experience with this stock and some of the current numbers. If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, don't forget to visit my Stock Picks Bob's Advice podcast site.

Bob

Posted by bobsadviceforstocks at 3:58 PM CDT

|

Post Comment |

Permalink

Updated: Monday, 7 August 2006 7:14 AM CDT

"Looking Back One Year" A review of stock picks from the week of April 11, 2005

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I hope you all are having a nice Saturday and that the week ahead is profitable and productive for you! Regular readers of my blog will realize that most weekends (?) I have been trying to review past selections on the blog and see how they would have done if I had indeed purchased shares in the stocks I discuss. For the sake of ease of analysis, I have been assuming a "buy and hold" investment strategy instead of the actual disciplined investment and portfolio management approach.

Rather than just buying and holding equities, I sell stocks quickly and completely on losses, and slowly and partially on targeted gains. This certainly will affect the result of purchasing such investments! But for our basic purposes, this analysis works just fine.

I continue to review past selections; however, after missing another weekend, my 'year-earlier' period is increasing by the week! Two weeks ago I reviewed the selections on the blog from April 4, 2005. Today, I would like to take a look at the next week: the week of April 11, 2005. Fortunately for me :), I only "picked" one stock that week: LoJack (LOJN). I do not own any shares nor do I have any options on this stock.

On April 13, 2005, I picked LoJack (LOJN) for Stock Picks Bob's Advice when the stock was trading at $13.94. LOJN closed at $17.55 on 8/4/06, for a gain of $3.61 or 25.9% since posting.

On April 13, 2005, I picked LoJack (LOJN) for Stock Picks Bob's Advice when the stock was trading at $13.94. LOJN closed at $17.55 on 8/4/06, for a gain of $3.61 or 25.9% since posting.

On May 5, 2006, LoJack announced first quarter 2006 results. For the quarter ended March 31, 2006, revenue climbed 18% to $50.7 million from $43 million in the same quarter last year. Net income increased to $2.94 million from $2.64 million in the prior year. On a per share basis, this worked out to $.15/share, up from $.14/dilutedshare last year.

On May 5, 2006, LoJack announced first quarter 2006 results. For the quarter ended March 31, 2006, revenue climbed 18% to $50.7 million from $43 million in the same quarter last year. Net income increased to $2.94 million from $2.64 million in the prior year. On a per share basis, this worked out to $.15/share, up from $.14/dilutedshare last year.

Since that was the only stock I reviewed that week, I feel safe to say that the average performance of stock picks that week was a gain of 25.9% since posting! Thank you for visiting! If you have any comments or questions, please feel free to leave them on the blog or drop me a line at bobsadviceforstocks.tripod.com. Please also be sure and visit my Stock Picks Bob's Advice podcast site.

Bob

Friday, 4 August 2006

August 4, 2006 Anaren (ANEN)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

Looking through the list of top % gainers on the NASDAQ this afternoon, I came across Anaren Microwave (ANEN) which closed at $19.22, up $1.55 or 8.77% on the day. I do not own any shares nor do I have any options on this stock.

Looking through the list of top % gainers on the NASDAQ this afternoon, I came across Anaren Microwave (ANEN) which closed at $19.22, up $1.55 or 8.77% on the day. I do not own any shares nor do I have any options on this stock.

According to the Yahoo "Profile" on Anaren, the company

"... engages in the design, development, and manufacture of microwave and radio frequency components, assemblies, and subsystems for wireless communications, satellite communications, and defense electronics markets."

This certainly is pretty high-tech stuff, and I don't think I can use my Peter Lynch strategy to pick stocks. But the numbers were pretty compelling so let's take a closer look at this company!

Like so many stocks on the move this time of year, the company moved sharply higher on the back of an earnings report. Yesterday, after the close of trading, Anaren announced 4th quarter 2006 results. For the quarter ended June 30, 2006, net sales came in at a record $29.1 million, up 21% over the $24.1 million in the same quarter the prior year. Net income worked out to $3.7 million or $.20/diluted share, up from $2.6 million or $.14/diluted share in 2005.

How about longer-term results?

If we review the Morningstar.com "5-Yr Restated" financials on ANEN, we can see that revenue actually dipped from $85 million in 2001 to $71 million in 2002 before resuming its climb to $94 million in 2005 and $100 million in the trailing twelve months (TTM).

Earnings also dipped from $.52/share in 2001 to $.16/share in 2003, before climbing to $.37/share in 2005 and $.56/share in the TTM.

I find it interesting and provocative to see that the outstanding shares which were 22 million in 2001, increase to 23 million in 2002, but then started declining....dropping to 20 million shares in 2005 and 17 million in the TTM. It is fairly rare to see a company retiring shares instead of increasing its float, but for the investor, this means a lower number of shares to spread the same earnings over, and thus pressure to the upside on earnings growth.

Free cash flow has been a bit erratic, with $8 million in 2003 reported, increasing to $11 million in 2004, then to a negative $(1) million in 2005 but a positive $9 million in the TTM.

The balance sheet, as reported on Morningstar, looks solid. $75.5 million in cash is reported, enough to easily pay off both the $10 million in current liabilities and the $6.5 million in long-term liabilities combined more than 4 times over. In fact, if we add in the $40.6 million in other current assets to the $75.5 million in cash, we have a sum of $116.1 million, which when compared to the $10 million in current liabilities yields a current ratio of 11.6, the highest current ratio on any stock I have reviewed as far as I can remember. This company appears from this exam to be quite solvent.

What about some valuation numbers?

Looking at the Yahoo "Key Statistics" on Anaren, we can see that this is a small cap stock with a market capitalization of only $330.37 million. The trailing p/e is a moderate 30.95, but the forward p/e is only 21.60 (fye 30-Jun-07), and the PEG (5 yr expected) isn't too bad at 1.38.

Checking the Fidelity.com eresearch website on Anaren, Fidelity has assigned them to the "Scientific/Tech Instruments" industrial group. In regards to the Price/Sales ratio, Anaren is relatively cheap with a ratio of 3.1. Topping this group is Garmin (GRMN) at 8.4, SiRF Technology (SIRF) at 5.9, Flir Systems (FLIR) at 3.8, Applied Biosystems (ABI) at 3.3, then Anaren at 3.1, and Beckman Coulter (BEC) at the cheapest ratio of 1.4.

Unfortunately, looking at profitability with a review of the 'return on equity' (ROE), ANEN is also at the bottom of the list with a ROE of 6.5%. Topping the list is Garmin (GRMN) at 30.8%, Flir at 24.7%, Applied Biosystems at 19.5%, Beckman Coulter at 11.4% and SiRF at 7%.

Finishing up with Yahoo, ANEN has only 17.19 million shares outstanding with 16.33 million that float. As of 7/11/06, there were 758,560 shares out short representing 4.60% of the float or 5.9 trading days of average volume (the short ratio). No cash dividends and no stock splits are reported.

What about the chart?

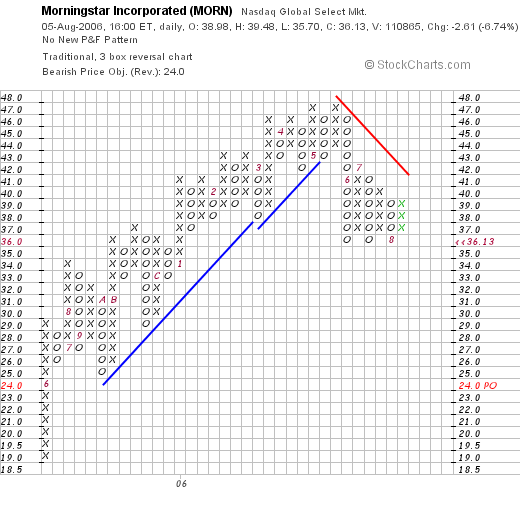

Reviewing the "Point & Figure" chart on ANEN from StockCharts.com, we can see that the company has been moving higher from its lows of around $7 from October, 2002. The company did sell-off in 2004 down to a low of $9.50, but since April, 2005, the stock has been moving steadily higher to the current level of around $19.22, a little under the highs of $24.00 in May, 2006. The chart looks relatively strong to me without appearing over-extended.

So what do I think? Well, the stock moved nicely higher today on the back of a terrific earnings report. Looking at Morningstar.com, this report is part of a longer trend of earnings and revenue growth. Free cash flow is positive recently, the company is reducing its outstanding shares, and the balance sheet is gorgeous. The p/e is reasonable imho with a PEG under 1.5. The Price/Sales isn't bad, but the profitability as measured by ROE is a bit low. Finally, the chart looks nice.

I don't really understand the business that this company is in from an intuitive perspective. However, if I were in the market to be buying a stock, this is the sort of company I would be purchasing!

Thanks so much for stopping by! Please remember to drop me a line at bobsadviceforstocks@lycos.com if you have any comments or questions. Certainly feel free to leave a comment right on the blog. Also, be sure and visit my Stock Picks Bob's Advice podcast site! You can listen to me rant as well as read my rants whenever you like!

Bob

Thursday, 3 August 2006

"Revisiting a Stock Pick" Christopher & Banks (CBK)

CLICK HERE FOR MY PODCAST ON CHRISTOPHER & BANKS

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

We have certainly had some tough days in the stock market recently! I haven't completely stayed with my investment strategy as you will see from my trading attempt with Kendle (KNDL). I always reserve the right to do something silly, and I managed to do just that. It isn't that I didn't like Kendle, it was just not part of my strategy to do a trade like that. And it didn't work out. So I am back to my plodding strategy that has been working a bit better than the old shoot from the hip approach!

We have certainly had some tough days in the stock market recently! I haven't completely stayed with my investment strategy as you will see from my trading attempt with Kendle (KNDL). I always reserve the right to do something silly, and I managed to do just that. It isn't that I didn't like Kendle, it was just not part of my strategy to do a trade like that. And it didn't work out. So I am back to my plodding strategy that has been working a bit better than the old shoot from the hip approach!

With the market trading a little better, I thought I would see if I couldn't find something to discuss this afternoon. Looking through the list of top % gainers on the NASDAQ today, I came across an old favorite of mine, Christopher & Banks (CBK), which, as I write, is trading at $29.44, up $1.30 or 4.62% on the day. I do not own any shares of this stock, nor do I own any options or other futures related to this company.

With the market trading a little better, I thought I would see if I couldn't find something to discuss this afternoon. Looking through the list of top % gainers on the NASDAQ today, I came across an old favorite of mine, Christopher & Banks (CBK), which, as I write, is trading at $29.44, up $1.30 or 4.62% on the day. I do not own any shares of this stock, nor do I own any options or other futures related to this company.

I say this is an "old favorite" because I have reviewed this stock previously on the blog. In fact, I first reviewed Christopher & Banks on Stock Picks Bob's Advice on June 5, 2003, when the stock was trading at $33.45. CBK had one stock split since that post on August 28, 2003, when the stock split 3:2. This results in an effective pick price for me of $22.30. Thus, with today's current stock price of $29.45, this means an effective appreciation of $7.15/share or 32.1% since posting.

And what does Christopher & Banks do? According to the Yahoo "Profile" on CBK, the company

"... operates retail specialty stores that sell women’s specialty apparel in the United States. It operates its retail stores under the Christopher & Banks, C.J. Banks, and Acorn names. Christopher & Banks stores offer fashions featuring co-ordinated assortments of sportswear and sweaters in sizes 4 to 16. C.J. Banks stores offer similar assortments of women’s specialty apparel in sizes 14W and up."

What drove the stock higher today, was the announcement of the 'all-important' same-store sales figures for July. When looking at retail companies like CBK, the same-store figure gives the investor a feeling for the 'organic' growth of the company; that is, by examining the performance of stores that have been open at least a year, we can take out the effect of opening new stores on the underlying growth results of the firm. This number can be considered a 'truer' criterion in examining sales results imho.

Basically, total sales for the five-week period ended July 29, 2006 "...increase 21% to $49.6 million from $41.1 million last year. July same-store sales rose 10%." In my expereience, anytime a retail firm can come in with high single-digit or low double-digit same-store sales increases, we have a great result. In addition, since same-store sales figures were a healthy 8% increase for the five month period ending July 29, 2006, this means that we are observing at least a short-term acceleration of sales growth. This report exceeded expectations according to the CEO Joe Pennington, and the company went ahead and raised guidance for the quarter ending August 26, 2006, to $.19 to $.20/diluted share, up from prior guidance of $.17 to $.19/share. This "trifecta" of sales reports----strong sales growth, exceeding expectations, and raising guidance, was enough to fire-up investors and get them to push the price of this stock higher.

And how about the latest quarterly result?

On June 20, 2006, CBK announced first quarter earnings results. As reported:

"Net sales in the first quarter increased 16% to $142.5 million, from $122.7 million in the prior year period, while same-store sales increased 7%. Net income for the first quarter increased 57% to $14.6 million, or $0.39 per diluted share, compared with $9.3 million, or $0.26 per diluted share, in the year ago period."

This was a very nice earnings report imho.

And longer-term results?

Looking at the Morningstar.com "5-Yr Restated" financials, we find that revenue, which was $276 million in 2002, has increased steadily to $490.5 million in 2006 and $510.4 million in the trailing twelve months (TTM).

Earnings have been a bit more erratic, climbing from $.83/share in 2002 to $1.01/share in 2004. However, they dropped to $.73/share in 2005, but have increased steadily since to $.97/share in the TTM. As an added plus, the company initiated dividends in 2004 with $.08/share paid. They have subsequently increased this to $.16/share in 2005 and since. the number of shares outstanding has been very stable with 37 million in 2002 and 37 million in the TTM.

Free cash flow appears quite healthy with $33 million in 2004, increasing to $39 million in the TTM.

CBK's balance sheet appears solid with $112.6 million in cash and $54.2 million in other current assets. The cash alone is enough to cover both the $41.5 million in current liabilities and the $33.8 million in long-term liabilities combined. Adding the cash and current assets together, gives us a sum of $166.8 million, which, when compared to the $41.5 million in current liabilities, yields a 'current ratio' of 4.02. Generally, anything 1.5 or higher is relatively 'healthy'.

How about some valuation numbers?

Reviewing the Yahoo "Key Statistics" on Christopher & Banks, we find that this is a mid-cap stock with a market capitalization of $1.10 billion. The trailing p/e is a moderate 30.02, with a forward (fye 25-Feb-08) p/e of 22.12. The PEG (5 yr expected) works out to a reasonable 1.14.

Looking at the Fidelity.com eresearch website, we can see that CBK is in the "Apparel Stores" industrial group and has a Price/Sales ratio of 2, near the top the retailers. Topping this group is Chicos Fas (CHS) with a ratio of 2.7, followed by Christopher & Banks (CBK) at 2 along with American Eagle (AEOS) at 2. Further down the list is Abercrombie & Fitch (ANF) at 1.7, Limited (LTD) at 1 and PacSun (PSUN) at 0.9.

Looking at profitability, we find Christopher & Banks at the bottom of the list of "return on equity" (ROE) with an 18.5% ROE. Topping the list is ANF at 37.6%, LTD at 31.9%, AEOS at 26.4%, CHS at 26% and PSUN at 23.1%. Thus, from these parameters, the company is relatively richly priced and is relatively less profitable than some of these other retailers.

Returning to Yahoo for some additional numbers, we see that there are 37.41 million shares outstanding and 36.41 million that float. Currently (as of 7/11/06) there are 2.54 million shares out short, representing 7% of the float or 4.4 trading days of average volume (the short ratio). This looks a little significant based on my own 3 day short interest 'rule'.

The company, as noted, pays a small $.16/share dividend yielding 0.60%. The last stock split, also as reported above, was August 28, 2003, when a 3:2 split was declared.

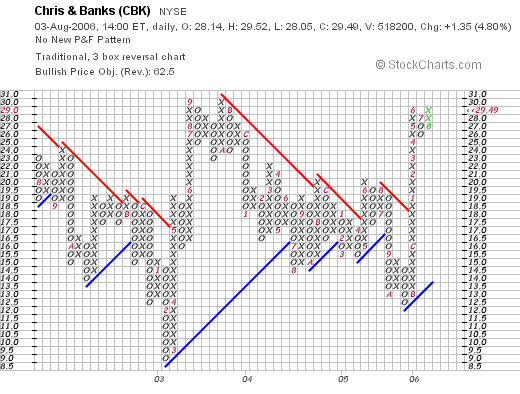

And what does the chart look like?

If we review a "Point & Figure" chart on CBK from StockCharts.com:

We can see that the stock has been trading sideways for the greater part of the past four years. Recently, the stock has moved back to historic highs and is poised to move into higher territory, as long as the underlying market allows. The graph is relatively neutral imho, and certainly doesn't look way over-priced.

So what do I think? Reviewing some of the above points on CBK, the company reported strong same store sales today in the low double-digit range and raised guidance for the current quarter. The latest quarterly results were solid with growing revenue and earnings. Morningstar.com looks strong as well except for a dip in earnings a few years ago, the company is free cash flow positive and has a nice balance sheet with lots of cash. Valuation wise, the p/e is a tad rich but the PEG is just over 1.1. The Price/Sales figures are a bit rich for the group and the profitability as measured by ROE is a tad low ...not my favorite combination of measurements. Finally, the graph is neutral and more recently appears to be moving higher.

In summary, I like the sales and earnings momentum on this company. Especially the same-store sales results. The other numbers are also supportive. While there is a premium being paid as indicated by the relatively rich price/sales ratio, the latest numbers certainly suggest the premium is well worth it!

Thanks so much for stopping by and visiting. If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Please also visit my Stock Picks Bob's Advice podcast site where I also talk about , in addition to writing about, my various stock market ideas!

Bob

Posted by bobsadviceforstocks at 1:10 PM CDT

|

Post Comment |

Permalink

Updated: Thursday, 3 August 2006 11:18 PM CDT

Tuesday, 1 August 2006

"Trading Transparency" KNDL

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

Today I learned another lesson :(. Stick with your strategy especially when it is working. As much as I like Kendle (KNDL), I will not let the loss I have grow. I do think the selling is overdone, but I cannot continue to fight this one. It is very important to recognize mistakes early and keep losses as small as possible.

A few moments ago, I sold my 800 shares of KNDL at $25.41. These shares had just been purchased (see the prior entry) on 7/27/06 at a price of $28.48. Thus, I had a loss of $(3.07) or (10.8)% on this investment. Even though I did not stick to my rules on making this purchase, I shall be sticking to my rules on limiting losses! And exceeding an 8% loss, I pulled the plug moments ago.

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to email me at bobsadviceforstocks@lycos.com and be sure to drop by and listen to my Stock Picks Bob's Advice podcast site.

Bob

Thursday, 27 July 2006

"Trading Transparency" KNDL---Breaking All of My Rules!

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice! As always, please remember that I am an amateur investor, so please rememeber to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

A few moments ago, I broke all of my trading rules---much the same way that I did with Dynamic Materials (BOOM) a few months ago. Kendle announced 2nd quarter earnings results this morning, and unfortunately missed expectations by a nickel. The market is in a "take no prisoners" mode and decimated the stock this morning. Kendle is trading at $28.22, down $(7.38) or (20.73%) as I write. I went ahead, believing that this was entirely overdone, and entered a purchase for 800 shares (!) of Kendle at $28.4799. Hopefully, I shall be correct on this move, as this is actually a larger than average purchase for me, totalling $22,783.92.

Let's review that earnings report and you will hopefully see why I would 'break' my trading rules and enter this stock purchase.

Net service revenue for second quarter 2006 came in at $62.1 million, an increase of 24% over net service revenue in the same quarter last year. Net income for the quarter came in at $4.29 million, up about 200% from last year's $1.44 million result. Again on a per share basis, this worked out to $.29/share, up sharply from $.10/share last year. Fully diluted "adjusted" net income, still worked out as $.39/share up over 100% from last year's "adjusted" fully diluted net income of $.19/share.

The Morningstar.com "5-Yr restated" is perfect. Almost perfectly steady revenue growth, earnings which dropped to a loss in 2002 at $(4.30)/share, have improved steadily, turning to a profit in 2004 at $.27/share, increasing to $.76/share in 2005, and $.93/share in the TTM.

Even the number of shares outstanding has been fairly steady at 12 million in 2001, increasing to 14 million in the TTM.

Free cash flow was $12 million in 2003, $18 million in 2005, and $17 million in the TTM.

The Morningstar balance sheet shows $51.6 million in cash and $80.6 million in other current assets, easily paying down the $60.3 million in current liabilities and the $1.5 million in long-term liabilities combined.

Anyhow, wish me luck. I am not following my intensely disciplined trading rules with this purchase. I am just trying to use my head and reserve the flexibility to make a purchase like this when things get entirely overdone imho.

Thanks again for stopping by! If you have any comments or questions on this or anything else on the blog, please feel free to leave your comments right on the blog or email me at bobsadviceforstocks@lycos.com. Also, be sure to visit my Stock Picks Bob's Advice Podcast website, where, if you are so inclined :), you can listen to me as well as read what I write!

Bob

Wednesday, 26 July 2006

July 26, 2006 BE Aerospace (BEAV)

CLICK HERE FOR MY PODCAST ON BE AEROSPACE

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

I was looking through the list of top % gainers on the NASDAQ today and came across BE Aerospace (BEAV) which, as I write, is trading at $23.05, up $2.83 or 14.0% on the day. I do not own any shares or options on this stock. The overall market is anemic with the middle-east conflict and climbing oil prices once again hanging over the market.

I was looking through the list of top % gainers on the NASDAQ today and came across BE Aerospace (BEAV) which, as I write, is trading at $23.05, up $2.83 or 14.0% on the day. I do not own any shares or options on this stock. The overall market is anemic with the middle-east conflict and climbing oil prices once again hanging over the market.

After reviewing some of what I consider relevant data, I thought that this stock deserved a spot on the blog! Let me share with you some of my observations.

First of all, on what the company does, according to the Yahoo Profile on BEAV, the company

"... engages in the manufacture and marketing of cabin interior products for commercial aircraft and business jets. It also distributes aerospace fasteners. The company operates in three segments: Commercial Aircraft, Distribution, and Business Jet."

Insofar as news driving the stock higher, the company announced 2nd quarter 2006 results and also announced an acquisition of Draeger, a German oxygen delivery system manufacturer for the aerospace market.

For the three months ended June 30, 2006, net sales climbed 30.8% to $271.5 million, from $207.6 million in the same quarter in 2005. Net earnings for the quarter came in at $18.7 million or $.24/diluted share, up over 100% from the $8.4 million or $.14/diluted share last year. The company raised guidance for 2006 in the same announcement, guiding to $1.19/diluted share, up $.02 for the estimate. According to the MarketWatch report on the earnings, analysts had been looking for earnings of $.21/share on sales of $252 million. Thus, the company did a "trifecta-plus" as I like to irreverantly refer to the earnings report; that is, they increased their revenue, increased their net income, exceeded expectations and raised guidance all in the same announcement. The stock climbed with this report!

How about longer-term results? Reviewing the Morningstar.com "5-Yr Restated" financials on BE Aerospace, we can see the steady (except for a dip in 2003) increase in revenue from $666.4 million in 2001 to $844.1 million in 2005 and $894.8 million in the trailing twelve months (TTM). Earnings, however, have been far less steady, dropping from a profit of $.78/share in 2001 to a loss of $(3.18) in 2002. The loss/share has been steadily improving until 2005, when the company reported a profit of $1.39/share and increased financial results to $1.50/share in the TTM.

Free cash flow, which was negative in 2003 at $(37) million improved to a negative $(4) million in 2005 and turned positive at $24 million in the TTM.

Reviewing the balance sheet, as reported on Morningstar, we find that the company has $140.5 million in cash and $434.2 million in other current assets. This works out to a total of $574.7 million in current assets, which, when compared to the current liabilities of $205.3 million yields a current ratio of 2.80. (Generally over 1.5 is considered 'healthy').

The company also has a not-insignificant $436.1 million in long-term liabilities.

What about valuation? Looking at the Yahoo "Key Statistics" on BE Aerospace, we find that the company is a mid-cap stock with a market capitalization of $1.8 billion. The trailing p/e is a very moderate 16.05, and we find the current forward p/e (?) at 17.60. However, with the growth in earnings expected, the 5 Yr expected PEG is only 0.81.

Using the Fidelity.com eresearch website for some more data, I found that BEAV is in the "Aerospace/Defence-Products/Services" industrial group. Within this group, BEAV has a very 'average' Price/Sales ratio of 1.7. Leading this group is Rockwell Collins (COL) with a ratio of 2.6, followed by BEAV at 1.7, then Orbital Sciences (ORB) at 1.5, Alliant Techsystems (ATK) at 0.9, DRS Technologies (DRS0 at 0.8, and EDO Corp (EDO) at 0.6.

Profitability, however, puts BEAV near the top of the group with a return on equity of 24%. Leading the group is Rockwell Collins with a 39.6% ROE, followed by BEAV at 24%, Alliant Techsystems at 21.7%, EDO at 9.5%, DRS at 9.3% and Orbital Sciences at 7.8%.

Finishing up the Yahoo review, there are 77.44 million shares outstanding with 76.42 million of them that float. Currently there are 3.70 million shares out short representing 3.6 trading days of average volume (the short ratio). No cash dividends are paid and no stock splits are reported on Yahoo.

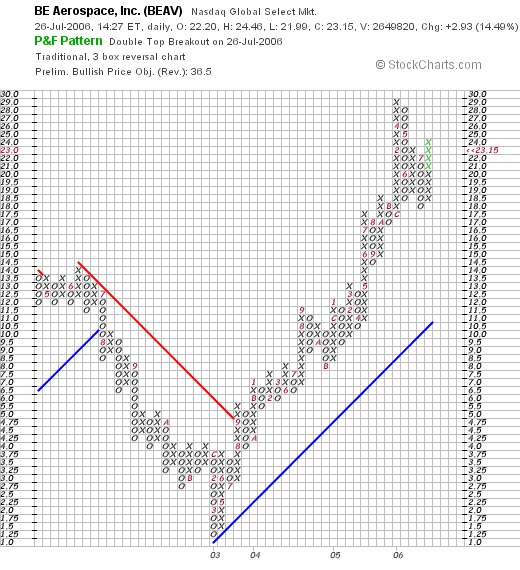

What about the chart? If we check the "Point & Figure" chart on BEAV from StockCharts.com, we can see that the stock was declining between July, 2002, when it was at $12.5, down to a low of $1.25 in March, 2003. Since then, the stock has moved strongly higher to the current level around $23.15. The stock chart looks strong to me!

So what do I think about this stock? Well, let's review a few of the findings.

First of all the company moved ahead strongly today on a great earnings report (they increased revenue, increased earnings, beat expectations, and raised guidance). The past five years have shown fairly steady improvement in the financial picture with growing earnings, revenue, and now positive free cash flow. The balance sheet is solid.

Valuation-wise, the p/e is in the teens and the PEG is under 1.0. The Price/Sales ratio is fairly average within its industrial group, and the profitability of the company is above average in its group. Finally, the chart appears solid. I do not know about the variability of the aerospace market, especially with the climbing fuel prices, but it appears most of the financial results are already "in the bag".

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Please be sure to stop by and visit my Stock Picks Bob's Advice Podcast Site.

Bob

Posted by bobsadviceforstocks at 1:50 PM CDT

|

Post Comment |

Permalink

Updated: Wednesday, 26 July 2006 11:09 PM CDT

Tuesday, 25 July 2006

"Revisiting a Stock Pick" Hologic (HOLX)

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website. I apologize for not doing a lot of posting the last couple of weeks. I am still working at building a new blog website but with the market correction, I frankly have not been motivated to look for new stocks....but have been posting my sales as they arise.

With the market climbing once again today (two days in a row!) I figured I would be able to find a stock or two that I liked. In fact, Hologic (HOLX), an old favorite of mine, was on the list of top % gainers, and the last price I have for it is $48.34, up $3.47 or 7.73% on the day. It is near the close of trading and probably is the closing price. I don't have any shares of HOLX in my Trading Account but my son does own literally 20 shares and my stock club also has purchased shares in Hologic.

With the market climbing once again today (two days in a row!) I figured I would be able to find a stock or two that I liked. In fact, Hologic (HOLX), an old favorite of mine, was on the list of top % gainers, and the last price I have for it is $48.34, up $3.47 or 7.73% on the day. It is near the close of trading and probably is the closing price. I don't have any shares of HOLX in my Trading Account but my son does own literally 20 shares and my stock club also has purchased shares in Hologic.

I first posted Hologic on Stock Picks Bob's Advice on April 27, 2005, when the stock was trading at $35.85. HOLX had a 2:1 stock split on December 1, 2005, making my effective stock pick 'price' actually $17.93. With today's closing stock price of $48.34, this represents an appreciation of $30.41 or 170% since posting the stock just a little over a year ago. And to think I didn't buy any shares for myself! At least I talked my stock club into this stock and bought a few shares for my son's account!

Let's take a closer look at this company. First of all what they do. According to the Yahoo Profile on Hologic, this company

" ...engages in the development, manufacture, and supply of diagnostic and medical imaging systems for serving the healthcare needs of women. It focuses on mammography and bone densitometry."

Next, what about the latest quarterly report? Actually, it was the third quarter 2006 earnings report release that sparked today's rally in the stock. Revenue for the third quarter ended June 24, 2006, came in at $119.7 million, a 62% increase over the $74.1 million reported in the same quarter last year. Net income increased 46% to $12.0 million or $.25/diluted share up from $8.2 million or $.18/diluted share in the same quarter last year.

How about longer-term results? If we check the Morningstar.com "5-Yr Restated" financials on HOLX, we can see that revenue has been steadily increasing from $180.2 million in 2001 to $287.7 million in 2005 and $341.2 million in the trailing twelve months (TTM). Earnings during this period have increased from a loss of $(.67)/share in 2001 to a profit of $.01/share in 2002, $.63/share in 2005 and $.75/share in the TTM. The company has been increasing its number of shares outstanding from 31 million in 2001 to 43 million in 2005 and 46 million shares outstanding in the TTM. I would rather see a stable number of shares all things being considered, however, with the solid growth in revenue in earnings, the company has been growing its financial results faster than its outstanding shares!

Free cash flow has been a bit erratic but has increased from a negative $(4) million in 2003 to $37 million in 2005 and $17 million in the TTM.

The balance sheet looks solid with $108.3 million in cash, more than enough to cover the combined $65.4 million in current liabilities and the $5.3 million in long-term liabilities combined. Calculating the 'current ratio' gives us a total of $256.1 million, which when divided by the $65.4 million in current liabilities, yields a current ratio of 3.92. (1.5 or higher is the minimum for good financial health as a rule).

And how about some updated statistics/valuation numbers on this company? Looking at the Yahoo "Key Statistics" on Hologic, we find that the company is a mid-cap stock with a market capitalization of $2.20 billion. The trailing p/e is certainly rich at 65.01, and the forward p/e (fye 24-Sep-07) isn't much better at 40.48. The PEG, however, suggests a more reasonable valuation of the p/e, that since due to the rapid growth in earnings, the PEG is estimated at 1.32 (5 yr expected).

Reviewing the Fidelity.com eresearch website, we find the Hologic is in the "Medical Appliances/Equipment" industrial group, and is in fact the most richly valued of the group in terms of the Price/Sales ratio. HOLX leads this group with a Price/Sales ratio of 6.2. Following Hologic is Medtronic (MDT) at 5.1, St Jude (STJ) and Zimmer Holdings (ZMH) both at 4.2, Biomet (BMET) at 3.9 and Edwards Lifesciences (EW) with a Price/Sales ratio of 2.9.

Insofar as profitability, using the 'return on equity' (ROE) as a guide, we find that Hologic is only average in this measure. Leading the group is Biomet with a ROE of 25.9%, Medtronic at 23.8%, Zimmer at 16.6%, then Hologic at 15.1%, St Jude at 14.4% and Edwards Lifesciences at 13.8%.

Finishing up the statistics from Yahoo, we find that there are 45.59 million shares outstanding and 45.1 million that float. Currently there are 6.56 million shares out short representing 14.5% of the float or a significant 6.9 trading days of volume. (I use 3 days as my arbitrary cut-off for significance.)

No cash dividend is paid and as I noted above, the company last split its stock on 12/1/05 when it declared a 2:1 stock split.

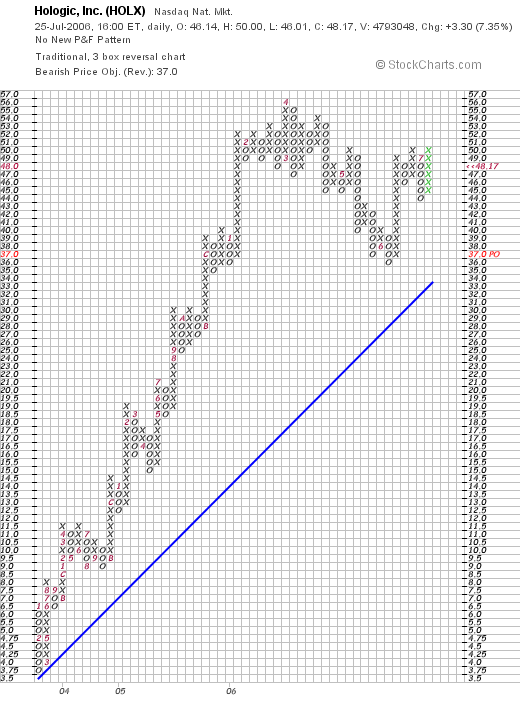

And what does the chart look like? Taking a look at the "Point & Figure" chart on Hologic from StockChart.com:

We can see a beautiful graph with an almost perfectly ascending price progression until May, 2006, when the stock sold off down to almost its support level. The stock appears to be appreciating once again.

So what do i think? I think the company reported a terrific quarter, has an outstanding Morningstar.com report (except for the very mild dilution of shares), and has a nice chart. Valuation, however, appears a bit rich and the stock thus appears to be "priced to perfection." Hopefull the company will continue to deliver perfect results. Certainly, the company's digital mammographer is selling well and this type of cancer detection may have some advantages over prior diagnostic procedures. with the p/e in the 60's and even the forward p/e in the 40's, fortunately we have a PEG just over 1.2. Even as measured by the Price/Sales ratio, the stock price appears rich. And profitability is not quite so phenomenal either. Only the rapid growth in earnings will continue to drive the stock higher.

Anyhow, that's the pick for this afternoon! A great performance from last year. Hopefull, for my son and my stock club, the stock will continue to perform well. Valuation, however, is a bit rich for what you are getting imho.

Thanks again for stopping by! If yhou have any comments or questions please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, please be sure to stop by and visit my Stock Picks Bob's Advice Podcast Website!

Bob

Posted by bobsadviceforstocks at 3:10 PM CDT

|

Post Comment |

Permalink

Updated: Tuesday, 25 July 2006 5:30 PM CDT

Saturday, 22 July 2006

"Looking Back One Year" A review of stock picks from the week of April 4, 2005

Hello Friends! Thanks so much for stopping by and visiting my blog, Stock Picks Bob's Advice. As always, please remember that I am an amateur investor, so please remember to consult with your professional investment advisors prior to making any investment decisions based on information on this website.

One of my weekend tasks that I try to address is the review of past stock picks on this blog. For ease of evaluation, I use a "buy and hold" assumption of past picks. In reality, I advocate and employ a disciplined buying and selling strategy with all of the stocks that I choose to own. This of course would affect the ultimate price performance of any investment.

Since I have again missed a couple of weeks in this review process, my trailing 52 weeks is getting closer to a trailing 65 weeks! In fact, I did review the week of March 28, 2005, but there weren't any stocks "picked" that week. My previous full review was on June 24, 2006 when I reviewed past picks from the week of March 21, 2005. Thus, I am now up to the week of April 4, 2005, which was a busy week for me on the blog! Let's take a look at those stock picks and see how they would have performed if we had purchased equal dollar amounts of the selections.

On April 4, 2005, I posted Jos A. Bank (JOSB) on Stock Picks Bob's advice when it was trading at $31.88. JOSB had a 5:4 stock split on 2/16/06, making my effective pick price actually only $23.88. JOSB closed on 7/21/06 at a price of $25.64 giving me a gain of $1.77 or 7.4% since "picking" the stock.

On June 8, 2006, JOSB announced first quarter 2007 results. For the quarter ended April 29, 2006, sales increased 17.7% to $113.7 million as compared with $96.6 million in the same quarter last year. Comparable store sales grew 4.7% during the period and combined catalog and internet sales climbed 25.0%. Net income, however, declined to $5.9 million or $.32/share, down from $6.7 million or $.38/share the prior year.

On June 8, 2006, JOSB announced first quarter 2007 results. For the quarter ended April 29, 2006, sales increased 17.7% to $113.7 million as compared with $96.6 million in the same quarter last year. Comparable store sales grew 4.7% during the period and combined catalog and internet sales climbed 25.0%. Net income, however, declined to $5.9 million or $.32/share, down from $6.7 million or $.38/share the prior year.

On April 5, 2005, I posted Greif Inc. (GEF) on Stock Picks Bob's Advice when it was trading at $74.06. GEF closed at $67.97 on 7/21/06, for a loss of $(6.09) or (8.2)% since posting.

On May 31, 2006, GEF announced 2nd quarter 2006 results. For the quarter ended April 30, 2006, net sales grew 1% to $620.1 million from $613.0 million in the same quarter last year. GAAP net income came inat $28.7 million or $.97/diluted Class A share and $1.49/diluted Class B share, compared to GAAP net income of $16.8 million or $.57/diluted Class A share and $.88/diluted Class B Share in the prior year.

On April 7, 2005, I posted Bed Bath and Beyond (BBBY) on Stock Picks Bob's Advice at a price of $40.80. BBBY closed at $32.62 on 7/21/06 for a loss of $(8.18) or (20.0)% since listing.

On April 7, 2005, I posted Bed Bath and Beyond (BBBY) on Stock Picks Bob's Advice at a price of $40.80. BBBY closed at $32.62 on 7/21/06 for a loss of $(8.18) or (20.0)% since listing.

On June 21, 2006, BBBY reported 1st quarter 2006 results. For the quarter ended May 27, 2006, net sales were $1.396 billion, a 12.2% increase from net sales of $1.244 billion in the same quarter in 2005. Net earnings for the quarter came in at $100.4 million, or $.35/diluted share, up from $98.9 million or $.33/diluted share the prior year. During the quarter, the company reported comparable store sales growth of 4.9%, better than the 4.4% same store growth in sales reported last year.

Finally, on on April 8, 2005, I posted Buckle (BKE) on Stock Picks Bob's Advice when the stock was trading at $35.60. Buckle closed at $37.90 on 7/21/06 for a gain of $2.30 or 6.5% since posting.

On May 18, 2006, Buckle reported 1st quarter results. For the quarter ended April 29, 2006, sales came in at $109.6 million, up from $105.5 million. Income increased to $9.4 million or $.47/share, up from $8.6 million or $.40/share in last year's same quarter. However, same store sales, a better indicator imho of the long-term potential of a retail firm, declined (1.3)%. Thus, even though sales overall grew, this result was influenced by new store openings and results were not quite as encouraging taking into consideration the shrinkage of same store sales results.

So how did I do for that week in April last year? Well, the average performance of the four stocks listed came in at a loss of (3.6)% with two stock losing and two stocks gaining....but the loss in BBBY biased the entire group into a losing result.

Thanks so much for stopping by and visiting! If you have any comments or questions, please feel free to leave them on the blog or email me at bobsadviceforstocks@lycos.com. Also, please be sure to stop by and visit my Stock Picks Bob's Advice podcast website!

Bob

Posted by bobsadviceforstocks at 3:45 PM CDT

|

Post Comment |

Permalink

Updated: Saturday, 22 July 2006 7:09 PM CDT

Newer | Latest | Older